Got a Section 148 notice in your inbox? Don’t panic. Here’s everything you need to know from what triggers it, to the exact steps you must take, with a ready-to-use reply format.

By Dr. Haresh Adwani, PhD (Commerce), Law Graduate, Adwani and Company

Imagine opening your email or logging into the Income Tax e-Filing Portal only to find a formal notice sitting there one that says “Section 148 Reassessment of Income.” For many taxpayers, that moment triggers instant anxiety. Is this a tax raid? Have I done something wrong? Do I need a lawyer?The truth is, a Section 148 notice is one of the most common yet misunderstood notices issued by the Income Tax Department of India. It doesn’t automatically mean you’ve committed fraud. In many cases, it simply reflects a data mismatch a transaction flagged in the Annual Information Statement (AIS), a Form 26AS inconsistency, or unreported income.

In this comprehensive 2026 guide, we break down everything you need to know about the Section 148 notice what it means, why you received it, exactly how to reply, critical deadlines, legal rights, and how Adwani and Company can help you resolve it with minimal risk.

IMPORTANT

Ignoring a Section 148 notice can lead to penalties, ex-parte reassessment orders, and in extreme cases, prosecution. Always respond within the specified deadline.

What Is a Section 148 Notice?

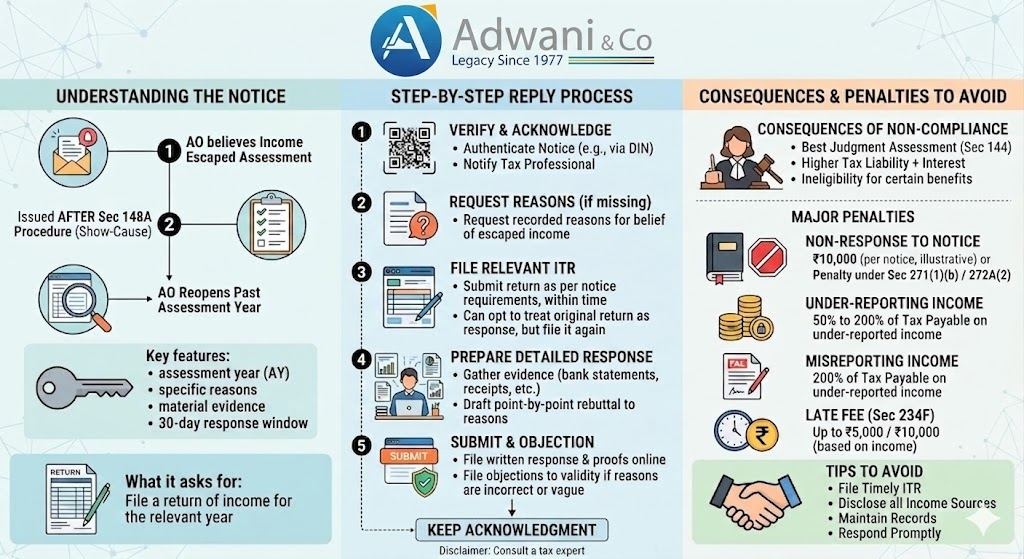

Under Section 148 of the Income Tax Act, 1961, the Assessing Officer (AO) is empowered to issue a notice to a taxpayer when there is “reason to believe” that income has escaped assessment meaning it was either not disclosed, was under-disclosed, or was incorrectly reported in a prior year’s Income Tax Return (ITR).

This notice initiates what is technically called reassessment proceedings. Upon receiving a Section 148 notice, the taxpayer is required to file or revise their ITR for the Assessment Year (AY) specified in the notice and provide an explanation for any discrepancies the department has identified.

According to the Income Tax Department’s guidelines, an AO must obtain prior approval from a superior officer typically a Commissioner or Principal Commissioner before issuing a Section 148 notice. This is a critical procedural safeguard that taxpayers can invoke if the notice appears to be improperly issued.

| Aspect | Detail |

|---|---|

| Governed by | Section 148, Income Tax Act, 1961 |

| Issued by | Assessing Officer (AO) |

| Purpose | Reassessment of escaped income |

| Requires approval of | Commissioner / Principal Commissioner |

| Time limit (normal) | Up to 3 years from end of relevant AY |

| Time limit (escaped income > ₹50 lakh) | Up to 10 years from end of relevant AY |

| Response required | File/revise ITR + submit explanation |

Why Did You Receive a Section 148 Notice?

The Income Tax Department relies on extensive data mining sourced from banks, registrars, stockbrokers, GST filings, and even foreign asset reports to identify potential underreporting. Here are the most common reasons a Section 148 notice is triggered

High-Value Financial Transactions

If you purchased a property, made significant investments in mutual funds or shares, or deposited large sums in cash without adequately disclosing the source in your ITR, the AIS (Annual Information Statement) will flag it. The department compares your declared income with these transactions automatically.

Mismatch Between AIS / Form 26AS and ITR

Your Annual Information Statement (AIS) and Form 26AS capture TDS deductions, interest income, dividend income, and other financial data. If your ITR doesn’t match these records, it can trigger a Section 148 notice.

Non-Filing or Incomplete Filing of ITR

If you failed to file an ITR for a particular year despite having taxable income, the department can reopen that year’s assessment for up to 3 years (or 10 years in serious cases) under Section 148.

Suspicious or Unexplained Entries

Accommodation entries, bogus purchases, inflated expenses, or donations made to questionable entities often draw scrutiny and may lead to a Section 148 notice for the concerned AY.

Information from Third Parties or Other Departments

Tip-offs from enforcement agencies, information shared by the GST department, or foreign asset disclosures can all prompt the AO to initiate reassessment under Section 148.

Practical Example

Mr. Ramesh Sharma sold a residential property for ₹80 lakh in FY 2022-23. The sale was registered with the Sub-Registrar and automatically reported to the Income Tax Department. However, Ramesh only declared capital gains on ₹35 lakh in his ITR, citing the indexed cost of acquisition. Without proper documentation a purchase agreement showing the original cost, improvement expenses, and indexed figures the AO had reason to believe ₹45 lakh escaped assessment. Ramesh received a Section 148 notice for AY 2023-24. With a well-drafted reply supported by documents, the case was resolved without any addition. This is exactly the kind of scenario Dr. Haresh Adwani and his team at Adwani and Company handle regularly.

Section 148 Notice: Step-by-Step Reply Process

1. Read the Notice Carefully: Note the Assessment Year, the deadline specified, and the reason recorded by the AO. Identify whether the reasons are explicitly stated or whether you need to request them separately through the portal.

2. Log In to the Income Tax e-Filing Portal: Visit incometax.gov.in, navigate to “Pending Actions,” and locate the notice. Download the official notice document for your records.

3. Request the “Reasons Recorded”: You have the legal right to request the reasons recorded by the AO before the notice was issued. This step is crucial it allows you or your CA to evaluate whether the notice itself is valid and challengeable.

4. Gather and Organise Documents: Collect bank statements, investment proofs, sale/purchase agreements, ITRs of previous years, Form 26AS, AIS, and any invoices or contracts relevant to the disputed transaction.

5. File the Return in Response to the Notice: In most cases, filing a revised or fresh ITR for the concerned AY is mandatory. Work with a qualified CA to ensure accuracy and completeness before submission.

6. Draft and Submit the Written Reply: Prepare a formal written reply acknowledging the notice, explaining the nature of each transaction, and attaching supporting documents. Submit this online via the portal’s response mechanism.

7. Attend Hearings and Respond to Follow-Up Queries: After your initial reply, the AO may schedule personal hearings or raise additional queries. Respond promptly with further clarifications and documentation.

Related Resources from Adwani and Company:

->Learn more about our Income Tax Notice handling services -_—> Read our detailed guide on responding to Section 143(2) Scrutiny Notice -> Understand how to appeal before the Income Tax Appellate Tribunal (ITAT)

Section 148 Notice Reply Format (Ready to Use)

Below is a simplified and legally sound reply format that you can use as a starting point. We strongly recommend consulting with a Chartered Accountant before submitting your actual reply.

Date: [DD/MM/YYYY]

To,

The Assessing Officer,

Income Tax Department,

Ward / Circle [___], [City]

Subject: Reply to Notice under Section 148 of the Income Tax Act, 1961 — AY [XXXX-XX] — PAN: [XXXXXXXXXX]

Respected Sir/Madam,

This is in response to the notice issued under Section 148 dated [Date of Notice] for Assessment Year [XXXX-XX].

1. Filing of Return in Response to Notice:

In compliance with the above notice, the return of income for AY [XXXX-XX] is being filed simultaneously through the Income Tax e-Filing Portal.

2. Nature of Alleged Discrepancy:

We understand that the notice pertains to [briefly describe the transaction — e.g., a property sale/cash deposit/investment] amounting to ₹[__] reported in AIS/Form 26AS for the said year.

3. Factual Explanation:

We respectfully submit that [provide a clear, factual explanation — e.g., “The said amount represents the sale of an ancestral property, the indexed cost of acquisition of which is ₹[__], resulting in taxable long-term capital gain of ₹[__], which has been duly reported in the ITR.”]

4. Documents Enclosed:

In support of our submission, the following documents are enclosed for your kind perusal:

a) Copy of Sale Deed / Agreement

b) Bank statements for the relevant period

c) Copy of ITR filed for AY [XXXX-XX]

d) [Any other relevant document]

We request your good office to kindly consider our submissions and close the matter. We remain available for any further clarification required.

Yours faithfully,

[Full Name]

[PAN Number]

[Date & Signature]

[If represented by a CA: For Adwani and Company, Chartered Accountants]

Time Limits for Section 148 Notice: Know Your Rights

One of the most important and frequently overlooked aspects of a Section 148 notice is the time limit within which it can be validly issued. If a notice is issued beyond the permissible period, it is legally invalid and can be challenged before the jurisdictional High Court or through a writ petition.

| Scenario | Maximum Time Limit | Approval Required |

|---|---|---|

| Normal cases | 3 years from end of relevant AY | Assessing Officer level |

| Escaped income exceeds ₹50 lakh | Up to 10 years from end of relevant AY | Principal Commissioner or Commissioner |

| Search / Survey cases | Special provisions apply (Section 153A/C) | Higher authorities |

Dr. Haresh Adwani — PhD in Commerce and a law graduate with extensive legal acumen — consistently advises clients to first verify the date of the notice against these statutory limits before preparing their response. An expired notice can be struck down entirely, saving the client from unnecessary litigation.

How Dr. Haresh Adwani Approaches Section 148 Cases

With decades of combined experience in income tax litigation and advisory, Dr. Haresh Adwani has developed a multi-layered approach to handling Section 148 notices. As the lead partner at Adwani and Company, he combines his academic depth (PhD in Commerce, law graduate) with practical courtroom and tribunal experience to build robust defence strategies for clients.

Under Dr. Haresh Adwani’s guidance, the firm systematically evaluates:

(a) whether the Section 148 notice is within the statutory time limit. (b) whether proper approvals were obtained, (c) whether the “reason to believe” is tangible and specific, and (d) whether the taxpayer’s disclosures are fully supported by documentation. This four-point framework has consistently produced favourable outcomes for clients across Gujarat and beyond.

Common Mistakes Taxpayers Make After a Section 148 Notice

Across hundreds of cases handled by Adwani and Company, certain mistakes appear repeatedly. Avoiding these can dramatically improve your outcome:

- Ignoring the notice : This is the most dangerous mistake. An ex-parte order (passed without hearing you) can result in a large addition to your income and a heavy tax demand.

- Filing an incomplete or inaccurate reply : Submitting a vague response without documentary support often worsens the situation and invites further scrutiny.

- Missing the deadline : The notice specifies a response window. Missing it eliminates your opportunity to present your case in the first round.

- Not engaging a qualified CA : Income tax reassessment is a technical, quasi-judicial proceeding. Attempting to navigate it without professional help risks costly errors.

- Not challenging an invalid notice : If the notice is time-barred or lacks proper approval, it can be quashed. Failing to raise this objection is a missed legal opportunity.

- Disclosing more information than required : Offering unsolicited information can open new lines of inquiry that the AO hadn’t considered.

Pro Tip from Adwani and Company

Always retain all financial documents for at least 7 years property agreements, bank statements, investment records, and ITR acknowledgements. This simple habit dramatically simplifies responding to any reassessment notice, including Section 148.

Can You Challenge a Section 148 Notice?

Yes and in many situations, you should. A Section 148 notice is challengeable on several legal grounds:

1. Notice Issued Beyond Statutory Time Limits

If the notice is issued after the permissible period (3 or 10 years, as applicable), it is void and can be challenged through a writ petition before the High Court.

2. Lack of “Tangible Material”

Courts across India, including the Supreme Court, have consistently held that an AO cannot issue a Section 148 notice based merely on suspicion or a change of opinion. There must be “new, tangible material” to justify reopening a closed assessment.

3. Procedural Defects

If proper approval from the required authority was not obtained, or if the notice was not served through proper channels as mandated by the Income Tax Act, it can be challenged.

Dr. Haresh Adwani routinely files objections against invalid Section 148 notices before the Assessing Officer itself and when rejected, escalates to the High Court often securing a stay on reassessment proceedings.

Conclusion: A Section 148 Notice Is Not the End It’s an Opportunity to Clarify

A Section 148 notice can feel overwhelming the moment it arrives. But as this guide demonstrates, it is a well-defined legal process with clear procedural safeguards, time limits, and your right to challenge it if improperly issued.

The most important steps are: read it carefully, do not ignore it, gather your documents, file your return in response, and submit a well-reasoned, documented reply ideally with the help of a qualified Chartered Accountant. Most reassessment cases, when handled proactively, close without any additional tax burden.

Dr. Haresh Adwani and the team at Adwani and Company have successfully guided hundreds of clients through Section 148 notices from straightforward data-mismatch cases to complex multi-crore reassessments. Their integrated approach combining tax expertise, legal knowledge, and documentation discipline consistently delivers results.

1. Is Section148 notice Serious?Should I be worried?

Yes, it is serious and should not be ignored but it is manageable. A Section 148 notice initiates reassessment proceedings and, if unanswered, can result in an ex-parte order with additional tax demands and penalties. However, with a proper reply and supporting documents, the vast majority of cases are resolved without any significant tax liability.

2. How do I reply to a Section 148 notice online?

Log in to the Income Tax e-Filing Portal (incometax.gov.in), navigate to “Pending Actions” → “Response to Outstanding Demand / Notices,” locate the Section 148 notice, and use the portal’s response mechanism to submit your reply and upload supporting documents. In parallel, file the return for the specified AY if not already done.

3. Do I have to file a return again in response to a Section 148 notice?

In most cases, yes. The notice specifically asks you to file a return for the Assessment Year under review. Even if you had originally filed a return for that year, you may need to file a fresh return (or a revised one, depending on the situation) in response to the Section 148 notice.

4. What happens if I ignore a SEction 148 notice?

Ignoring the notice is highly inadvisable. The Assessing Officer will proceed ex-parte meaning without your input and pass a best-judgment assessment order. This typically results in significant additions to your income, heavy tax demands, and penalties. In serious cases, prosecution under the Income Tax Act is also possible.

5. Can I chanllenge a Section 148 notice in Court?

Yes. If the notice is issued beyond the permissible time limit, without tangible material, or without proper approval from superior authorities, it can be challenged through a writ petition before the jurisdictional High Court. An experienced tax advocate or CA specialising in income tax litigation like Dr. Haresh Adwani can assess whether your notice is legally vulnerable.

6. How long does the Section 148 reassessment process take?

Yes. If the notice is issued beyond the permissible time limit, without tangible material, or without proper approval from superior authorities, it can be challenged through a writ petition before the jurisdictional High Court. An experienced tax advocate or CA specialising in income tax litigation — like Dr. Haresh Adwani — can assess whether your notice is legally vulnerable.

7. What penalty can be imposed after a Section 148 reassessment?

If the reassessment results in an addition to income (i.e., income found to have escaped assessment), a penalty under Section 270A may be levied ranging from 50% to 200% of the tax on the under-reported or misrepresented income, in addition to the actual tax and interest demands.

About the Author

Dr. Haresh Adwani

Ph.D. in Commerce | Law Graduate | Managing Partner, Adwani & Co LLP Dr. Haresh Adwani holds a Ph.D. in Commerce and is a qualified Law graduate with over two decades of hands-on experience in GST advisory, direct taxation, and statutory compliance for businesses across Pune and Maharashtra. As Managing Partner of Adwani & Co LLP a firm established in 1977 by Advocate N. T. Adwani Dr. Adwani has guided hundreds of

SMEs, startups, and corporates through India’s evolving tax landscape. He is a recognised advisor on GST compliance, company formation, and Virtual CFO services, and regularly

contributes to professional seminars and industry forums in Pune.