Dr. Haresh Adwani May 2026 12 min read

Everything looks completely fine your books are in order, you filed your income tax return (ITR) on time, and business is running smoothly. Then, one morning, an income tax notice India arrives in your inbox. That familiar dread kicks in. What went wrong? Am I in trouble? What do I do next?

You are not alone. Thousands of businesses and individuals receive income tax notices in India every year and a significant number of them are not the result of deliberate tax evasion. Many arise from minor data mismatches, incomplete documentation, or automated system flags triggered by the Income Tax Department’s AI driven scrutiny tools.

The good news: an income tax notice India 2026 is not a verdict. It is a question. And with the right guidance, you can answer it confidently, professionally, and without drama.

This guide walks you through everything you need to know about income tax notices India why they happen, what the different types mean, how to respond to an income tax notice, and how working with an experienced CA firm like Adwani and Company can protect your financial future.

Why Income Tax Notices India Are Increasing in 2026

The Income Tax Department of India has undergone a dramatic technological transformation over the past few years. The introduction of the new Income tax Act, 2025 (effective April 1, 2026) and the notified Income Tax Rules, 2026 have significantly strengthened the government’s compliance machinery.

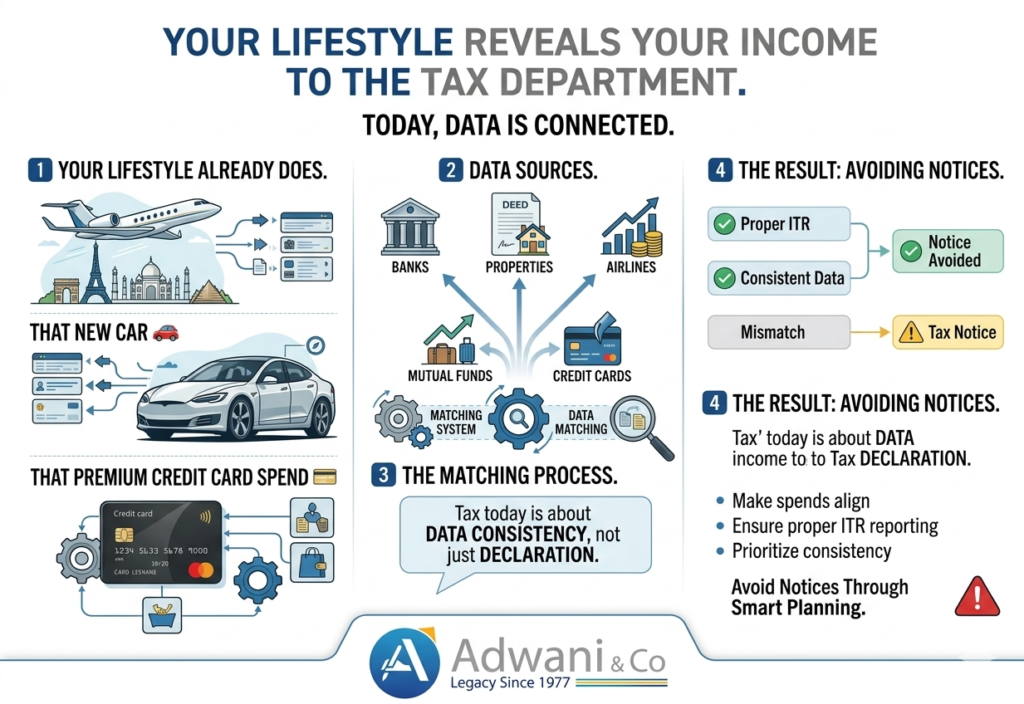

According to the Income Tax Department’s official portal (incometaxindia.gov.in) and public advisories, the department now cross-verifies taxpayer data from multiple sources simultaneously, including:

- Income Tax Returns (ITR) filed for FY 2025-26

- TDS and TCS data submitted by employers and businesses

- GST Portal records and GSTR filings

- MCA (Ministry of Corporate Affairs) company filings

- Bank transaction data and high-value financial statements

- Social media spending patterns flagged against declared income

- E-way bills and e-invoice records

When any of these data points contradict each other, an automated flag is raised and that flag can trigger an income tax scrutiny notice under Section 143(2), a reassessment notice under Section 148, or a demand notice under Section 156, among others.

As per updates from the Income Tax Department India and compliance advisories published under the Income tax Rules 2026, the department now uses sophisticated Computer Assisted Scrutiny Selection (CASS) systems to identify ITRs with statistical anomalies, making income tax compliance India more critical than ever before.

Common Types of Income Tax Notices in India You Must Know

Not all income tax notices India carry the same weight. Understanding which type of income tax notice you have received is the first and most important step.

1. Section 143(1) Intimation Notice

This is the most common notice and is largely automated. Issued after initial processing of your ITR filing 2026, it may flag arithmetic errors, TDS mismatches, or minor adjustments. In most cases, it requires a simple correction or no action at all.

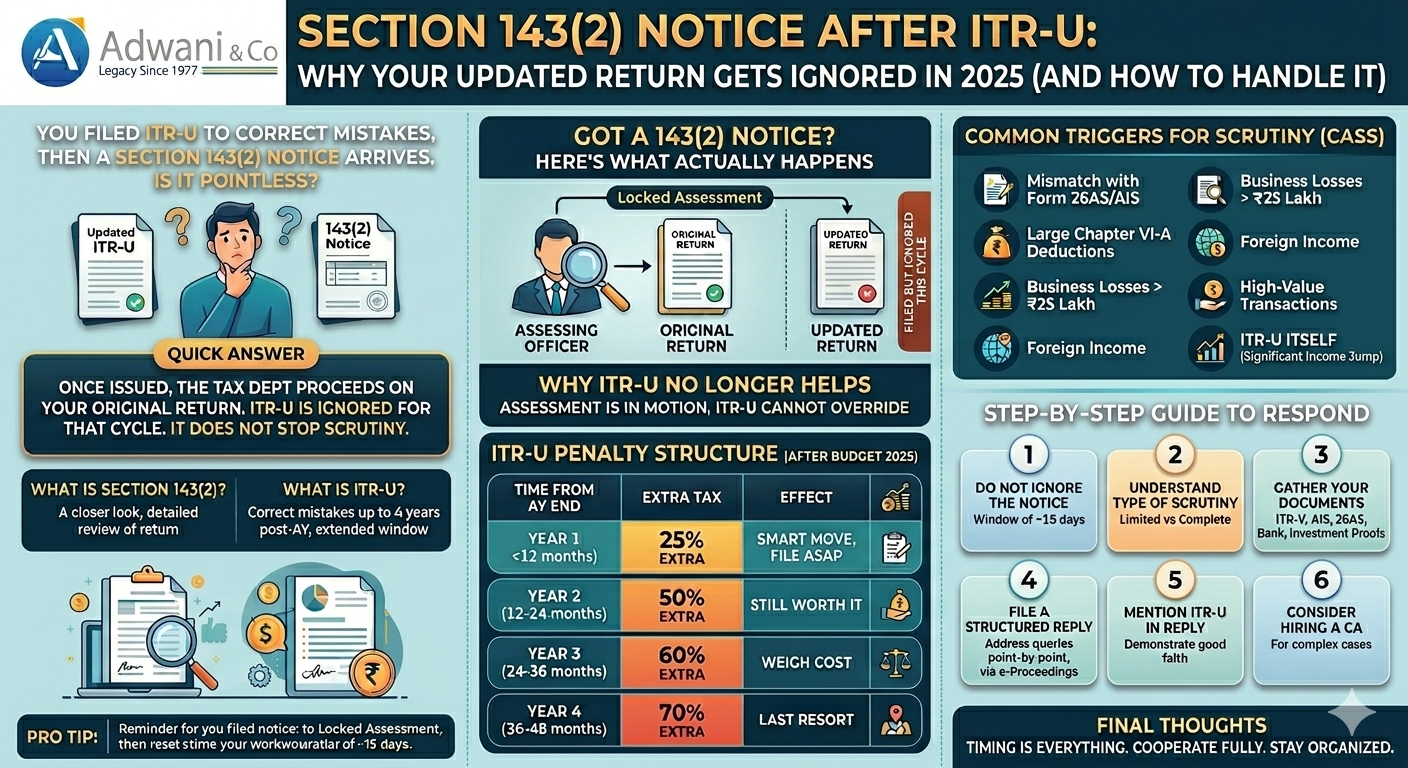

2. Section 143(2) Scrutiny Notice

This is a more serious income tax scrutiny notice. The assessing officer wants to examine specific aspects of your return in detail. As per Section 143(2), this notice can only be issued within three months from the end of the financial year in which the return was filed.

Example: If you filed your ITR on July 31, 2025, for FY 2024-25, an income tax scrutiny notice under Section 143(2) can be issued only until June 30, 2026. Beyond that, the notice is time-barred.

3. Section 148 Reassessment Notice

When the Income Tax Department believes income has escaped assessment, it may issue a notice under Section 148 to reopen completed assessments. This is often called an income tax reassessment notice, and the time limits are strictly governed under the Income-tax Act, 2025.

4. Section 156 Demand Notice

If the department determines a tax liability after assessment, it issues a demand notice under Section 156. A penalty of up to ₹10,000 under Section 272A can apply for failure to respond to certain notices within the stipulated timeframe.

5. Section 142(1) Inquiry Notice

Before completing an assessment, the assessing officer may ask for additional information or documents through this income tax inquiry notice. Prompt and accurate responses are essential to avoid escalation.

PRACTICAL EXAMPLE

A mid-sized trading business in Pune files its ITR for FY 2024-25 showing annual turnover of ₹1.80 crore. However, the GST Portal reflects GSTR-1 turnover of ₹2.05 crore for the same period. The e-way bill system shows goods movement worth ₹2.15 crore. The Income Tax Department’s automated system flags a discrepancy of ₹25 lakh between the ITR and GST data. An income tax scrutiny notice under Section 143(2) is issued not because the business evaded tax, but because the numbers don’t align across systems. A proper income tax notice reply, backed by reconciliation statements and supporting documents, is what resolves this situation.

This is exactly the kind of scenario Dr. Haresh Adwani PhD in Commerce, law graduate, and founder of Adwani and Company has been warning clients about for years. In his experience advising businesses across Maharashtra and beyond, the majority of income tax notices India arise not from fraud but from data inconsistencies that proper compliance systems could have prevented.

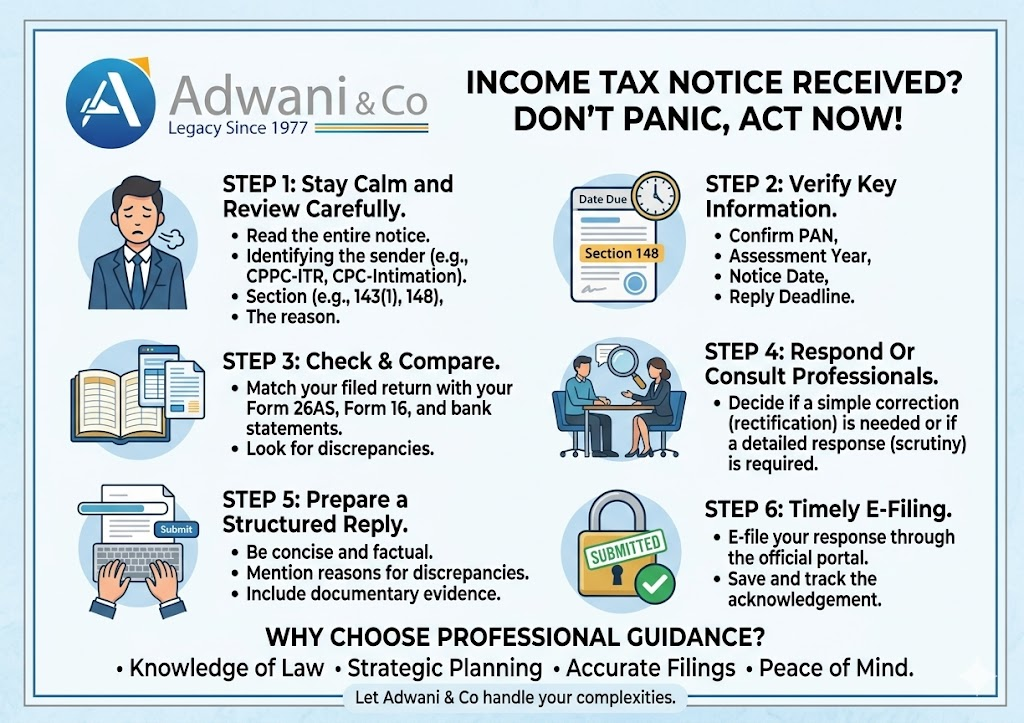

How to Respond to Income Tax Notice India: A Step by Step Guide

Receiving an income tax notice India can feel overwhelming. But a structured, professional response is what separates a resolved case from an escalated one. Here is the approach recommended by experienced tax professionals:

Step 1 : Read the Notice Completely and Carefully

Identify the section under which the income tax notice is issued, the assessment year in question, the deadline for response, and the specific issue or mismatch being raised. Do not assume what the notice is about read every word.

Step 2 : Do Not Ignore It

Ignoring an income tax notice India is never a safe strategy. Failure to respond within the prescribed time can result in ex-parte assessments, penalties under Section 272A, and additional scrutiny. Even if you believe the notice is incorrect, a formal income tax notice reply must be filed.

Step 3 : Gather All Relevant Documents

Collect ITR acknowledgements, Form 26AS, AIS (Annual Information Statement), bank statements, GST returns, invoices, TDS certificates, and any other documentation relevant to the period under scrutiny.

Step 4 :Reconcile the Data

Compare your ITR figures against Form 26AS, AIS, GST data, and bank records. Identify where the mismatch exists and build a factual explanation supported by documents.

Step 5 : Draft a Legally Sound Income Tax Notice Reply

Your income tax notice reply must be factual, legally precise, and supported by evidence. Emotional or vague responses rarely help. If the matter involves complex legal interpretation which many income tax assessment notices do professional assistance is not optional; it is essential. Learn more about our Income Tax Notice Reply Services at Adwani and Company.

Step 6 : Respond Through the Official E-Filing Portal

All responses to income tax notices India must be filed through the official Income Tax e filing portal at incometaxindia.gov.in. Maintain digital acknowledgements of every submission for future reference.

Income Tax Notice India 2026: Why Expert Guidance Matters

The new Income Tax Rules, 2026 have introduced stricter disclosure requirements, more granular scrutiny parameters, and enhanced cross-border tax provisions. For businesses and individuals navigating this landscape, professional expertise is not a luxury it is a necessity. Dr. Haresh Adwani brings a rare combination of academic rigour and practical expertise to income tax compliance and notice management. Holding a PhD in Commerce and a law degree, Dr. Haresh Adwani understands the financial, legal, and procedural dimensions of income tax proceedings with equal depth. This multidisciplinary perspective is exactly what taxpayers need when facing complex income tax scrutiny notices or reassessment proceedings.

At Adwani and Company, the team provides end-to-end support for clients receiving income tax notices India, covering everything from initial notice analysis and document reconciliation to drafting professional income tax notice replies and representing clients before assessing officers.

Whether you are a salaried professional, a business owner, or an NRI with Indian income, Adwani and Company offers the structured, strategic approach that income tax matters demand.

Read our detailed guide on Income Tax Return Filing and Compliance for businesses and individuals.

Key Income Tax Changes in 2026 That Could Trigger a Notice

The Income tax Act, 2025 and Income Tax Rules, 2026 have introduced several changes that increase the probability of income tax notices India for businesses and individuals who are not aware of the new compliance requirements:

- New Form 124 replaces Form 12BB for HRA and investment declarations incorrect transitional filings may trigger discrepancies.

- Enhanced perquisite valuation rules for employer-provided benefits such as accommodation, cars, and insurance.

- Stricter TDS compliance with updated section references under the Income-tax Act, 2025 using old section numbers (e.g., Section 194C) for new transactions may cause filing errors.

- Significant Economic Presence (SEP) threshold of 2 crore or 3 lakh users for digital businesses, with new scrutiny implications.

- Mandatory PAN disclosure for landlords when annual rent exceeds 1 lakh, with explicit relationship disclosure requirements.

- New audit trail requirements for stock exchanges relevant for investors and high net worth individuals.

Businesses that continue operating under pre2026 compliance assumptions are at higher risk of receiving income tax notices India in the coming months. A proactive compliance review is strongly recommended.

Income Tax Notice India 2026: What Small Businesses Must Do Now

Small business owners often operate under the misconception that income tax scrutiny is reserved for large corporations. That belief is outdated. With AI based CASS systems and integrated data verification across GST, MCA, and banking records, no taxpayer falls completely under the radar.

Here is what small businesses must prioritize to avoid income tax notices India:

- File ITR 2026 accurately and on time do not leave discrepancies between income declared and financial statements

- Reconcile turnover declared in income tax return with GST Portal data every quarter

- Ensure TDS deductions under the new Income-tax Act, 2025 framework are accurately filed

- Maintain proper invoicing records and banking documentation for all high-value transactions

- Verify that all financial data submitted to MCA aligns with income tax return data

- Conduct an Annual Information Statement (AIS) review before filing ITR to identify pre-existing discrepancies

As Dr. Haresh Adwani often advises clients: the best income tax notice reply is the one you never have to write because proactive compliance prevented the notice from being issued in the first place.

Learn more about our Business Tax Compliance Services for small and medium enterprises.

AIS, Form 26AS, and Income Tax Notice India: The Hidden Connection

Many taxpayers who receive income tax notices India are surprised to discover that the trigger was information already available on the Income Tax Department’s own portal — and that they never reviewed it before filing their return.

The Annual Information Statement (AIS) and Form 26AS are the Income Tax Department’s comprehensive databases of financial transactions linked to your PAN. They include:

- Salary income reported by employers

- Interest income from savings accounts and fixed deposits

- Dividend income from shares and mutual funds

- High-value purchase and sale transactions in real estate and securities

- Foreign remittances and international transactions

- GST turnover data

If the figures in your ITR do not match what appears in your AIS, the system is designed to flag it automatically. Reviewing and reconciling your AIS before filing your income tax return 2026 is one of the most effective ways to prevent an income tax scrutiny notice.

For official guidance, visit the Income Tax Department India portal or the Ministry of Corporate Affairs for business-related compliance updates.

Conclusion:

An income tax notice India is not the end of the road. In most cases, it is the beginning of a conversation between you and the Income Tax Department a conversation that, with the right preparation and professional support, can end cleanly and quickly.

The year 2026 marks a significant turning point in India’s tax compliance environment. With the Income tax Act, 2025 and Income Tax Rules, 2026 now in full effect, businesses and individuals face a more scrutinised tax landscape than ever before. Data cross-verification is automated, discrepancies are flagged in real time, and the margin for error has narrowed considerably.

The professionals and businesses that will thrive in this environment are those who treat income tax compliance as a continuous, proactive discipline not a once a year filing exercise. They review their AIS before filing. They reconcile GST and income tax data regularly. They maintain robust documentation. And when an income tax notice India does arrive, they respond swiftly and professionally.

Working with an experienced, multidisciplinary CA firm is the most reliable way to achieve this standard of compliance and notice preparedness.

Frequently Asked Questions

1. What is an income tax notice India and why did I receive one?

An income tax notice India is a formal communication from the Income Tax Department asking you to clarify, confirm, or provide documentation for specific aspects of your filed return. Common reasons include data mismatches between your ITR and AIS/Form 26AS, unusual financial transactions, TDS discrepancies, or failure to report certain income. Receiving a notice does not automatically mean you owe additional tax.

2. How do I respond to an income tax notice India 2026?

Log into the official Income Tax e-filing portal at incometaxindia.gov.in, navigate to ‘Pending Actions,’ and respond within the prescribed deadline. Your income tax notice reply should be factual, supported by documentation, and — for complex cases — drafted with professional assistance from a qualified CA firm.

3. What happens if I ignore an income tax scrutiny notice?

Ignoring an income tax scrutiny notice can lead to ex-parte assessment under Section 144, where the assessing officer decides the case based only on the department’s information. This frequently results in higher demand, additional penalties, and potential legal proceedings. Never ignore an income tax notice India, regardless of how minor it appears.

4. What is the time limit for responding to an income tax assessment notice?

Time limits vary by notice type. Section 143(1) intimations typically require response within 30 days. Section 143(2) scrutiny notices have timelines specified in the notice itself. Always check the deadline stated in the notice and respond before it — late responses may be treated as non-compliance.

5. Can income tax notices India be avoided with proper compliance?

While no compliance system provides 100% immunity from notices, maintaining accurate records, reconciling AIS and GST data before ITR filing, using correct TDS sections under the Income-tax Act 2025, and engaging a professional CA firm like Adwani and Company for periodic compliance reviews significantly reduces income tax notice risk.

6. How does the Income Tax Department India detect unreported income in 2026?

The Income Tax Department now uses AI-based CASS systems that cross-verify data from GST returns, bank transactions, MCA filings, e-way bills, TDS records, and even high-value lifestyle expenditures visible in financial data. Any significant inconsistency between these sources can automatically trigger an income tax scrutiny notice, even if your ITR appears complete.

About the Author

Dr. Haresh Adwani

Ph.D. in Commerce | Law Graduate | Managing Partner, Adwani & Co LLP Dr. Haresh Adwani holds a Ph.D. in Commerce and is a qualified Law graduate with over two decades of hands-on experience in GST advisory, direct taxation, and statutory compliance for businesses across Pune and Maharashtra. As Managing Partner of Adwani & Co LLP a firm established in 1977 by Advocate N. T. Adwani Dr. Adwani has guided hundreds of

SMEs, startups, and corporates through India’s evolving tax landscape. He is a recognised advisor on GST compliance, company formation, and Virtual CFO services, and regularly

contributes to professional seminars and industry forums in Pune.