A Doctor. A Foreign Account. A Notice That Changed Everything.

A Doctor. A Foreign Account. A Notice That Changed Everything.

A doctor maintained a foreign savings account for years. It was opened during his fellowship abroad, kept active for convenience — occasional deposits, minor interest income, nothing extravagant. He never declared it in his Income Tax Return because, frankly, he did not think it mattered.

Then a notice arrived from the Income Tax Department.

The department already knew about the account. The balance. The interest earned. The transactions. All of it.

How? Through the silent, relentless data-sharing machinery of FATCA CRS foreign assets disclosure frameworks that have fundamentally changed how foreign asset reporting works across 120+ countries.

This is not a hypothetical story. Dr. Haresh Adwani, Partner of Adwani and Company, has personally guided numerous doctors and professionals through exactly this situation. And the pattern is almost always the same: a well-meaning professional, an undisclosed foreign account, and a notice that triggers panic.

As Dr. Haresh Adwani puts it: “I personally know doctors who had no idea their foreign savings accounts were visible to the Indian tax department. They maintained them for years without declaration. And then the notices came.”

This blog is your comprehensive guide to understanding FATCA CRS foreign assets disclosure, why it matters especially for doctors, and how to ensure you are fully compliant before the department comes knocking.

What Is FATCA CRS Foreign Assets Disclosure?

FATCA CRS Foreign Assets Disclosure: The FATCA Framework Explained

FATCA was originally enacted by the United States in 2010 to combat tax evasion by US persons holding accounts abroad. However, its impact has been global. Under FATCA, foreign financial institutions (FFIs) worldwide are required to report information about accounts held by tax residents of partner countries including India.

India signed an Inter-Governmental Agreement (IGA) with the US on 9 July 2015, with the implementing Rules (114F to 114H) notified on 7 August 2015 and the agreement coming into force on 31 August 2015, making Indian financial institutions subject to FATCA reporting requirements from that date. But more importantly for Indian taxpayers, this agreement also works in reverse — foreign financial institutions report Indian residents’ account information to the Indian tax authorities.

CRS: The Common Reporting Standard

While FATCA is US-centric, the Common Reporting Standard (CRS) is a global framework developed by the Organisation for Economic Co-operation and Development (OECD). Under CRS:

- Over 120 jurisdictions have committed to automatically exchanging financial account information

- Financial institutions identify accounts held by foreign tax residents

- Account information is reported to the local tax authority, which then shares it with the account holder’s home country

India adopted CRS in 2017 under Rule 114F to 114H of the Income Tax Rules.

What Information Gets Exchanged Under FATCA CRS Foreign Assets Disclosure?

The scope of information sharing is comprehensive:

- Account holder identity: Name, address, tax identification number (PAN)

- Account balance: Year-end balance or value

- Interest income: Gross interest credited during the year

- Dividend income: Dividends received during the year

- Sales proceeds: Gross proceeds from sale of financial assets

- Other income: Any other income credited to the account

This means the Income Tax Department potentially has access to your foreign account details before you even file your return. This is the reality of modern FATCA CRS foreign assets disclosure — and ignoring it is no longer an option.

Also Read:

Why Doctors Are Particularly Vulnerable to FATCA CRS Foreign Assets Disclosure Issues

The Medical Professional’s Global Footprint

Doctors, more than almost any other professional group, have legitimate reasons for maintaining foreign financial connections:

- Medical fellowships abroad: Many Indian doctors spend 2–5 years training in the US, UK, Australia, or other countries, opening bank accounts during their stay. These accounts often remain open long after they return to India.

- Conference travel and honorariums: International medical conferences sometimes pay honorariums or reimbursements into foreign accounts.

- Investments made during overseas training: Some doctors invest in mutual funds, retirement accounts (like 401(k) in the US or pension funds in the UK), or even property during their time abroad.

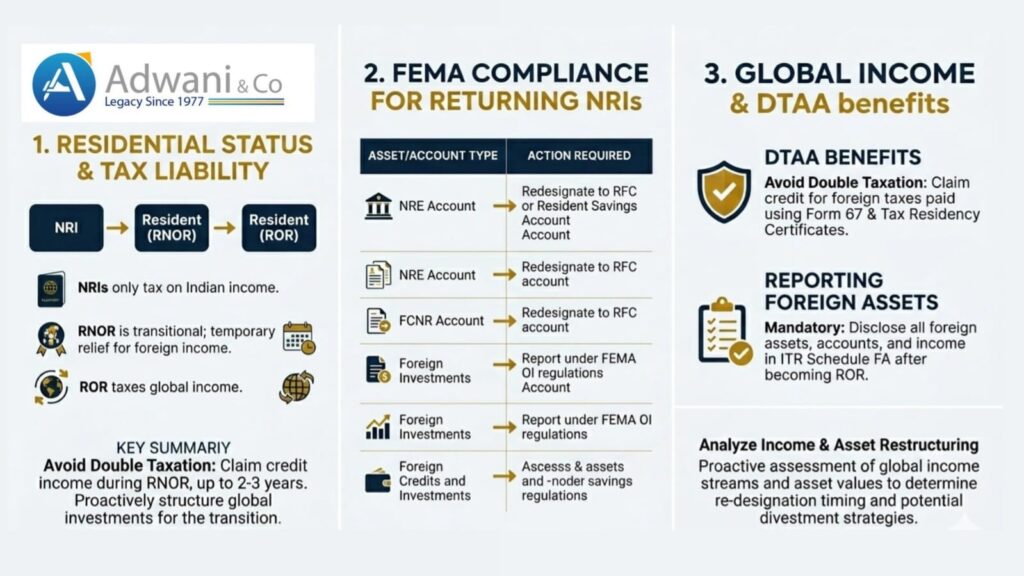

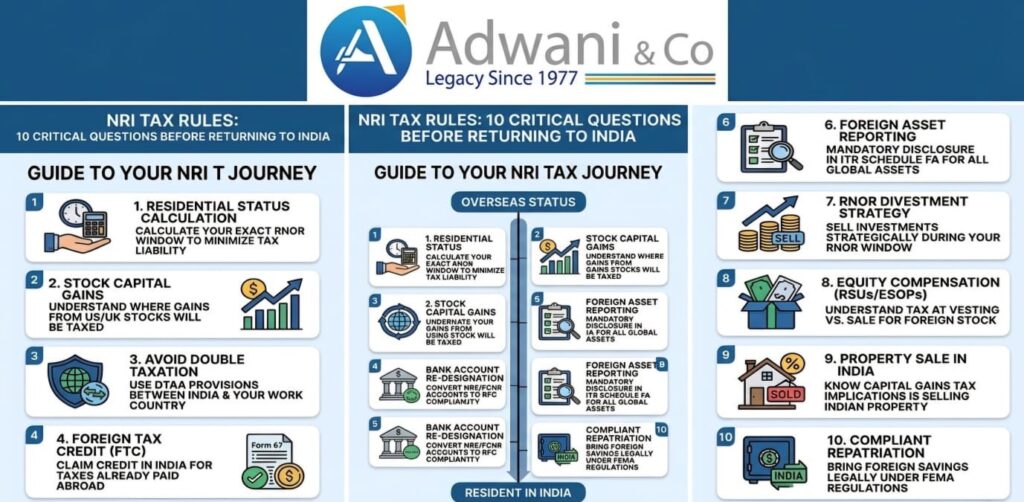

- NRI to Resident status transition: Doctors who return to India after extended overseas practice often retain NRE/NRO accounts or foreign accounts that need different tax treatment once residential status changes.

- Collaborative research funding: International research grants may be channeled through foreign institutional accounts where the doctor has beneficial ownership.

- Inheritance: Some doctors inherit foreign assets from family members settled abroad.

The problem is not having these accounts or assets. The problem is not disclosing them in the Indian ITR which triggers FATCA CRS foreign assets disclosure compliance failures.

The Common Misconception About FATCA CRS Foreign Assets Disclosure

Most doctors Dr. Haresh Adwani encounters share a common misconception: “The account is dormant / the balance is small / I do not use it anymore so it does not need to be declared.”

This is incorrect.

Under Indian tax law, every foreign asset must be disclosed in Schedule FA of your ITR, regardless of:

- Whether the account is active or dormant

- The balance amount (even zero-balance accounts with potential opening during the year)

- Whether any income was earned

- Whether the income was received in India or abroad

Schedule FA: The Mandatory Foreign Assets Declaration

What Is Schedule FA?

Schedule FA (Foreign Assets and Foreign Income) is a section in the Indian Income Tax Return where taxpayers must declare all foreign assets and income. It applies to individuals who are Resident and Ordinarily Resident (ROR) in India.

What Must Be Disclosed in Schedule FA?

The disclosure requirements are extensive:

- Foreign bank accounts: Every account, including dormant ones, with details of the bank name, country, account number, peak balance during the year, and closing balance

- Foreign financial accounts: Investment accounts, custodial accounts, insurance products with cash value

- Foreign immovable property: Property owned abroad, with purchase details, country, total investment, and income derived

- Foreign equity or debt interest: Shares, debentures, or any other interest in a foreign entity, with name of entity, country, nature of interest, and total investment

- Foreign trusts: Beneficial interest as trustee, beneficiary, or settler in any foreign trust

- Any other foreign asset: Any other capital asset held outside India

- Foreign income: All sources including salary, interest, dividends, rental income, and capital gains

5 Key Points Most Doctors Miss About FATCA CRS Foreign Assets Disclosure

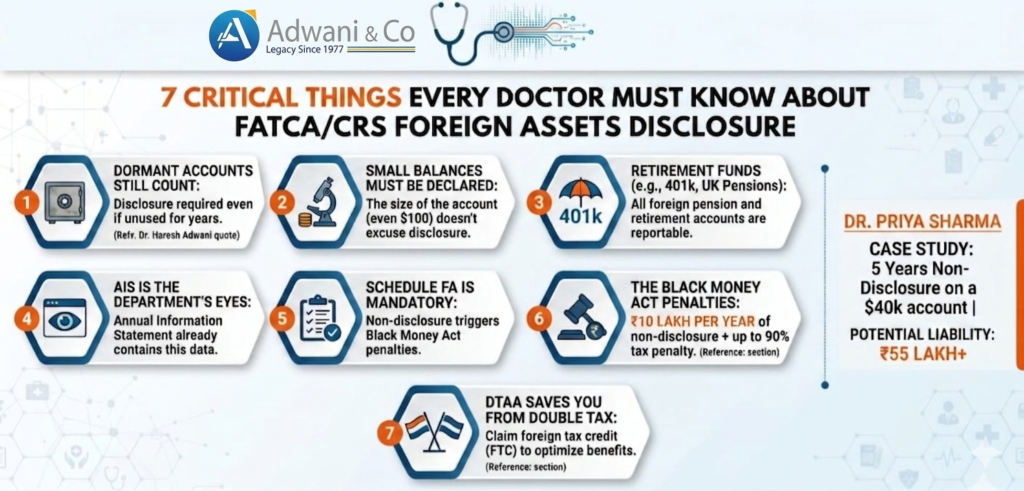

- Dormant accounts count. Even if you have not used the account in years, if it exists and has a balance (even $100), it must be declared.

- Retirement accounts abroad count. Your US 401(k) or UK pension fund needs to be disclosed in Schedule FA.

- Income received in India from foreign sources counts. If a foreign entity pays you a consulting fee and deposits it in your Indian bank account, it is still foreign income that needs proper classification.

- Jointly held accounts count. If you are a joint holder on a family member’s foreign account, your interest may need to be disclosed.

- Signing authority matters. Even if you do not own the account but have signing authority on it, disclosure obligations may apply.

The Black Money Act: Severe Consequences for Non-Compliance

What Is the Black Money Act?

The Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015 commonly called the Black Money Act was specifically enacted to deal with undisclosed foreign assets and income. It is one of the most stringent tax laws in India.

Penalties Under the Black Money Act

- Undisclosed foreign income: Tax at 30% flat rate (no slab benefit) + penalty of 90% of the tax amount (effective rate: approximately 120% of the undisclosed income)

- Failure to disclose foreign assets in Schedule FA: Penalty of ₹10 lakh per assessment year of non-disclosure

- Willful attempt to evade tax on foreign income: Rigorous imprisonment of 3–10 years + fine

These penalties are in addition to regular income tax liability. And unlike regular tax proceedings, the Black Money Act penalties are not easily negotiable or reducible.

A Real-World Example of FATCA CRS Foreign Assets Disclosure Penalties

Dr. Priya Sharma (name changed for privacy) maintained a bank account in the United States with an average balance of $40,000 (approximately ₹33 lakh). The account earned interest of $800 per year. She never disclosed the account or the interest income in her ITR for 5 years.g FATCA CRS foreign assets disclosure is not just important it is financially critical.

When the information reached the Indian tax department through FATCA:

| Liability Head | Amount |

|---|---|

| Penalty for non-disclosure of foreign asset | ₹10 lakh × 5 years = ₹50 lakh |

| Tax on undisclosed interest income | 30% of total interest over 5 years |

| Additional penalty | Up to 90% of the tax amount |

| Total potential liability | ₹55 lakh+ |

This is precisely why understanding FATCA CRS foreign assets disclosure is not just important it is financially critical.

How the Income Tax Department Uses FATCA CRS Data

The FATCA CRS Foreign Assets Disclosure Data Pipeline

Here is how the information flows:

- Foreign financial institution identifies an account held by an Indian tax resident

- Foreign tax authority collects this data from institutions in its jurisdiction

- Data is transmitted to the Indian Income Tax Department through automatic exchange

- The department matches this data against the taxpayer’s filed ITR

- If there is a mismatch an asset not declared, income not reported a notice is generated

According to the Income Tax Department, India has been actively receiving and processing FATCA/CRS data since 2017, and the matching algorithms have become increasingly sophisticated.

The AIS Connection

Your Annual Information Statement (AIS) now includes foreign asset and income information received through FATCA/CRS. Before filing your ITR, you can check your AIS to see what the department already knows about your foreign financial life.

Dr. Haresh Adwani strongly recommends this as a first step for all clients with any foreign connections: “Check your AIS before you file. If the department already has the information, there is no point in not disclosing it. Voluntary compliance is always the less painful path.

The FEMA Angle: Double Jeopardy for Non-Compliance

It is important to note that FATCA CRS foreign assets disclosure failures do not just create income tax problems. They can also trigger issues under the Foreign Exchange Management Act (FEMA), administered by the Reserve Bank of India.

If you are a resident Indian holding foreign assets without proper RBI authorization, you may face:

- Penalties under FEMA for unauthorized holding of foreign assets

- Compounding proceedings before the RBI

- Scrutiny of the original source of funds used to acquire the foreign asset

The Income Tax Department and RBI have information-sharing mechanisms, which means a tax notice can snowball into a FEMA investigation and vice versa.

This dual regulatory framework makes it even more critical for doctors to ensure full FATCA CRS foreign assets disclosure compliance across both regimes.n assets disclosure compliance across both regimes.

What Should You Do Right Now?

Step 1: Audit Your Foreign Financial Footprint

Make a comprehensive list of every foreign financial relationship you have or have ever had:

- Bank accounts (active and dormant)

- Investment accounts

- Retirement/pension accounts

- Property ownership

- Signing authority on any account

- Beneficial interest in foreign entities

Step 2: Check Your Past ITRs

Review your filed returns for the last 5–6 years. Did you fill out Schedule FA? Were all foreign assets disclosed? Was foreign income properly reported?

If you filed through a CA or tax preparer, ask them specifically whether Schedule FA was completed.

Step 3: Download Your AIS and TIS

Your Annual Information Statement (AIS) and Taxpayer Information Summary (TIS) on the Income Tax e-filing portal may already contain information received through FATCA/CRS. Check whether foreign account data appears there.

Step 4: Consider Voluntary FATCA CRS Foreign Assets Disclosure

If you discover that your foreign assets were not disclosed in past returns, the voluntary disclosure route is always the less painful path. While penalties may still apply, proactive disclosure demonstrates good faith and can significantly reduce the severity of consequences.

Dr. Haresh Adwani advises: “Voluntary disclosure, done correctly and timely, is always better than waiting for a notice. The department is far more lenient with taxpayers who come forward than with those who are caught.”

Step 5: Engage a Specialist

Foreign asset taxation sits at the intersection of Indian tax law, international treaties, FEMA regulations, and country-specific tax rules. This is not a DIY exercise. Engage a Chartered Accountant with specific experience in international taxation and FATCA/CRS compliance.

At Adwani and Company, we have a dedicated practice for NRI taxation and foreign asset compliance.

Key DTAA Benefits You Might Be Missing {#dtaa}

What Is DTAA?

India has signed Double Taxation Avoidance Agreements (DTAA) with over 90 countries. These agreements ensure that the same income is not taxed twice — once in the country where it is earned, and again in India.

How DTAA Applies to FATCA CRS Foreign Assets Disclosure

If you earn interest on a US bank account, for example:

- The US may withhold tax at 15% (under the India-US DTAA)

- You must declare this income in your Indian ITR

- You can claim tax credit for the US tax paid under Section 90/91

- Your effective Indian tax on this income is reduced by the foreign tax credit

Many taxpayers miss this benefit, ending up paying double tax — or worse, not declaring the income at all because they assume tax has already been paid abroad. Proper FATCA CRS foreign assets disclosure includes optimizing your DTAA benefits.

Real-World Resolution: How Adwani and Company Helps

The Situation: A surgeon who returned to India in 2018 after a 6-year practice in the UK. He retained a UK bank account with £25,000 and a small pension fund. He filed Indian ITRs since 2018 but never completed Schedule FA. In 2024, he received a notice from the Income Tax Department referencing CRS data.

Our Approach:

- Comprehensive review of all foreign accounts and their history

- Reconciliation of foreign income with Indian tax filings for each year

- Preparation of revised returns with complete Schedule FA disclosure

- Drafting a detailed response to the income tax notice explaining the oversight and demonstrating good faith

- Liaison with the Assessing Officer to settle the matter at the assessment stage

- FEMA compliance review to ensure RBI requirements were also met

The Outcome: The matter was resolved with minimal penalties. No prosecution. No extended investigation. The key factor? Proactive, professional, and transparent engagement with the department..

Conclusion: FATCA CRS Foreign Assets Disclosure Is a Legal Necessity

The world has changed. Financial borders have dissolved — not for money, but for information. With FATCA and CRS, your foreign accounts are no longer your private secret. They are data points in a global network that connects over 120 countries, and the Indian Income Tax Department is an active participant in this network.

For doctors and professionals with foreign assets, the message is clear: FATCA CRS foreign assets disclosure is not optional, not a formality, and not something to be deferred. It is a legal obligation with severe consequences for non-compliance.

But here is the silver lining voluntary compliance, done correctly, is the less painful path. It protects you from penalties, prosecution, and the stress of responding to a notice you were not prepared for.

As Dr. Haresh Adwani consistently advises: “The department often knows before you file. The question is not whether to disclose it is whether you disclose on your terms or on theirs.”

If you have foreign assets, accounts, or income that need to be properly disclosed, connect with Adwani and Company today. Our team has deep expertise in international tax compliance, FATCA/CRS reporting, and Black Money Act advisory. We will ensure your disclosures are accurate, complete, and strategically optimized.

Your expertise saves lives. Let ours protect your financial well-being.

Do not wait for the notice. Take control of your FATCA CRS foreign assets disclosure compliance today with Adwani and Company.

“This blog is for informational purposes only and does not constitute legal or tax advice. Please consult a qualified professional for advice specific to your situation.”

1. What is FATCA CRS foreign assets disclosure?

refers to the mandatory reporting and declaration of foreign financial accounts and assets under the Foreign Account Tax Compliance Act (FATCA) and Common Reporting Standard (CRS). Indian taxpayers must declare all foreign assets in Schedule FA of their ITR.

2. Do I need to disclose a dormant foreign bank account in my ITR?

tax law, every foreign bank account — whether active, dormant, or even zero-balance — must be disclosed in Schedule FA if you are a Resident and Ordinarily Resident (ROR) in India.

3. What is the penalty for not disclosing foreign assets in India?

Act, 2015, non-disclosure of foreign assets attracts a penalty of ₹10 lakh per assessment year. Additional penalties of up to 90% of the tax amount and imprisonment of 3–10 years may also apply.

4. How does the Income Tax Department know about my foreign accounts?

FATCA and CRS, over 120 countries automatically share financial account information with India. Your foreign bank reports your account details to its local tax authority, which then transmits it to the Indian Income Tax Department

5. Can I file a revised return to disclose previously undisclosed foreign assets?

can file a revised or updated return to correct past omissions within the prescribed time limits. Voluntary FATCA CRS foreign assets disclosure is always viewed more favorably than forced disclosure after a notice. Consult Adwani and Company for guidance.

6. Are foreign retirement accounts like 401(k) reportable in India?

Yes. Foreign retirement accounts, pension funds, and similar instruments are reportable under Schedule FA. The income treatment may vary based on the specific DTAA provisions between India and the relevant country.

7. How can Dr. Haresh Adwani help with FATCA CRS foreign assets disclosure?

Haresh Adwani and the team at Adwani and Company provide end-to-end support for FATCA CRS foreign assets disclosure — from asset mapping and AIS verification to Schedule FA preparation, DTAA benefit optimization, and notice response. Contact us today.

Author

| Dr. Haresh Adwani PhD (Commerce) • Adwani & Company, Pune Dr. Haresh Adwani holds a PhD in Commerce and brings over 20 years of expertise in GST compliance, income tax advisory, FEMA, and corporate law. He is one of Pune’s most trusted Chartered Accountants for GST litigation, demand notice resolution, appeal management, and tax planning for businesses and individuals. Services include GST audit, ITR filing, GST appeal representation, notice response, NRI taxation, and FEMA compliance. |