What Every Business Must Do Right Now

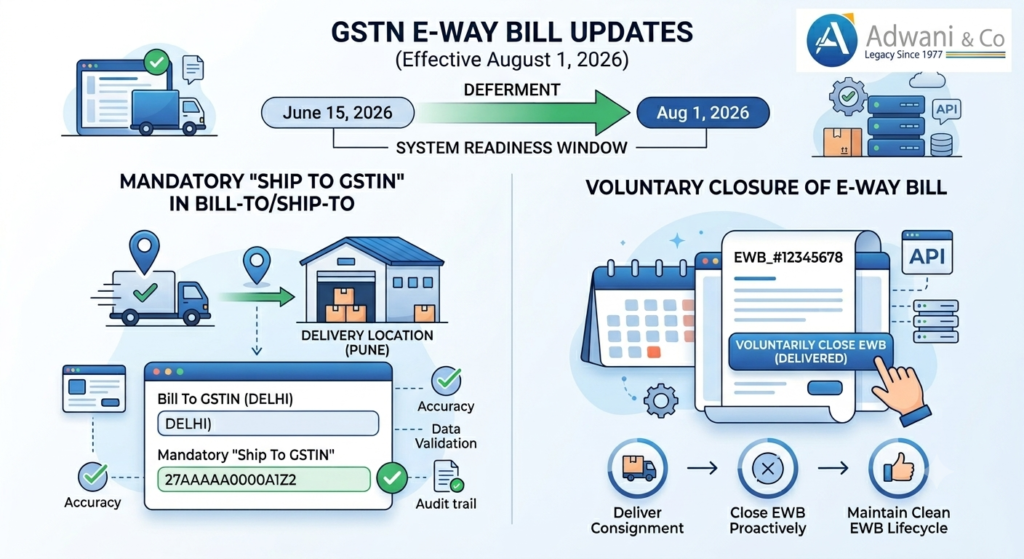

Two critical E-Way Bill Changes announced by GSTN are now deferred to 1 August 2026.If your business moves goods across India, you cannot afford to ignore what just happened on the GSTN E-Way Bill portal. In a move that has been welcomed across industry, the Goods and Services Tax Network (GSTN) has officially deferred two major E-Way Bill changes originally scheduled for 15 June 2026 to 1 August 2026. That gives you less than two months to get your systems, data, and teams ready.

But here is the critical question: will your organisation use this window strategically, or will August arrive before your ERP has even been updated?

In this detailed guide, CA Veena Adwani of Adwani & Co LLP a multi-disciplinary professional services firm serving businesses since 1977 breaks down exactly what these E-Way Bill updates mean, why they matter, and the concrete steps your compliance team should take before the new rules kick in.

Key Update at a Glance: GSTN has deferred two major E-Way Bill enhancements mandatory capture of “Ship To GSTIN” in Bill-To / Ship-To transactions, and the introduction of the Voluntary Closure of E-Way Bill facility from 15 June 2026 to 1 August 2026.

Understanding the E-Way Bill Framework in India

Before we dive into the specific E-Way Bill changes, it is important to understand the regulatory foundation on which this system rests. The E-Way Bill mechanism was introduced under Rule 138 of the CGST Rules, 2017. It mandates that a registered person causing the movement of goods of consignment value exceeding ₹50,000 must furnish the relevant information in Part A of Form GST EWB-01, either electronically on the GSTN E-Way Bill Portal (ewaybillgst.gov.in) or through a facilitation centre notified by the Commissioner.

Over the years, the GSTN has continuously enhanced the E-Way Bill system to bring greater transparency, auditability, and alignment between physical goods movement and GST records. The two E-Way Bill updates now deferred to August 2026 are part of this continuous improvement process.

The Two Key E-Way Bill Changes Deferred to August 2026

1. Mandatory Capture of “Ship To GSTIN” in Bill-To / Ship-To Transactions

In many commercial transactions, the party being billed is different from the party to whom the goods are physically delivered. This is the classic Bill-To / Ship-To scenario common in industries like FMCG, pharma, automobile, and manufacturing supply chains.

Currently, E-Way Bills in such transactions often capture only the billing party’s details. Under the new E-Way Bill change, the GSTIN of the actual recipient at the delivery address the “Ship To GSTIN” must be mandatorily captured. This change is designed to:

- Improve traceability of goods at the point of actual delivery

- Reduce mismatches between E-Way Bill data and GSTR-1 / GSTR-2B records

- Strengthen the input tax credit (ITC) matching framework

- Reduce instances of fake or fictitious transactions in the GST ecosystem

From a compliance perspective, as per the GST Council’s stated objectives of strengthening the anti-evasion mechanism, accurate “Ship To GSTIN” data creates a digital audit trail directly linking the E-Way Bill with the supplier’s GST return a step that tax officers can use to verify the genuineness of ITC claims.

2. Voluntary Closure of E-Way Bill Facility

The second significant E-Way Bill update is the introduction of a Voluntary Closure feature. Currently, an E-Way Bill automatically expires after its validity period elapses based on distance. If the goods have been delivered before that period ends, there is no mechanism for the generator to proactively close or mark the EWB as delivered.

The new Voluntary Closure facility will allow the EWB generator to:

- Proactively close an E-Way Bill once the consignment has been delivered

- Prevent misuse of an open EWB after actual delivery

- Maintain a cleaner, more accurate EWB lifecycle in the GSTN system

- Reduce the administrative burden of tracking open EWBs

This is a particularly meaningful change for businesses running high-volume logistics operations, where thousands of EWBs are generated monthly. The ability to voluntarily close delivered consignments will bring both operational clarity and better GST compliance hygiene.

Why GSTN Deferred These E-Way Bill Changes

The deferment from 15 June 2026 to 1 August 2026 was not a surprise to those who closely follow GST technology implementation cycles. Change management in the Indian GST ecosystem is complex it involves not just GSTN but also:

- Thousands of ERP and accounting software vendors across India

- GST Suvidha Providers (GSPs) and Application Service Providers (ASPs)

- Large enterprises running SAP, Oracle, or Microsoft Dynamics

- Small businesses using Tally, Zoho Books, or other SME-grade software

- Logistics and transporter companies generating EWBs in bulk

Each of these stakeholders needs time to update their API integrations, test new workflows, clean up master data, and train operational staff. The extension reflects GSTN’s practical, industry-focused approach aligning with the Central Board of Indirect Taxes & Customs (CBIC) ‘s broader goal of making GST compliance as seamless as possible for legitimate businesses.

📌 Important Perspective: The additional time should not be viewed as a delay. It is an opportunity and the businesses that treat it as such will be far better positioned on 1 August 2026.

A Practical Example: How the E-Way Bill Change Affects You

Real-World Scenario

Company ABC Pvt. Ltd. (Mumbai) sells 500 units of industrial equipment to XYZ Distributors Pvt. Ltd. (Delhi) but the goods are to be delivered directly to XYZ’s warehouse in Pune (billed to Delhi, shipped to Pune).

Before the E-Way Bill change: ABC’s team generates an EWB showing XYZ’s Delhi GSTIN as the recipient. The Pune delivery address appears in the transporter field, but no GSTIN for the Pune entity is captured.

After the E-Way Bill change (from 1 August 2026): ABC must now also capture the “Ship To GSTIN” of the Pune warehouse/entity in the EWB form. If XYZ’s Pune branch is separately registered under GST, its GSTIN must be entered. If not separately registered, the same Delhi GSTIN may apply but the field cannot be left blank.

Action required by ABC: Update its ERP master data for all consignee locations, verify Ship-To GSTINs, and configure the EWB generation workflow to capture this field before August 1.

This simple example illustrates why GSTIN master data validation is among the most urgent tasks businesses must complete before the E-Way Bill update goes live.

E-Way Bill Compliance Checklist: Prepare Before 1 August 2026

CA Veena Adwani recommends the following structured approach for businesses preparing for the upcoming E-Way Bill changes:

| Action Area | What To Do | Priority |

|---|---|---|

| Master Data | Validate and update “Ship To GSTIN” for all consignee and delivery locations | 🔴 High |

| ERP / Software | Coordinate with your ERP vendor to activate the new Ship To GSTIN field and Voluntary Closure API | 🔴 High |

| API Integration | Test updated GSTN API calls on the sandbox environment before production go-live | 🔴 High |

| Process Review | Update internal SOPs for logistics, invoicing, and EWB generation teams | 🟡 Medium |

| Team Training | Train accounts, logistics, and dispatch teams on the new requirements | 🟡 Medium |

| Vendor Alignment | Inform key suppliers and customers about the Ship To GSTIN requirement | 🟡 Medium |

| Internal Audit | Audit existing open E-Way Bills and plan for Voluntary Closure hygiene | 🟢 Ongoing |

Why E-Way Bill Compliance Matters More Than Ever in 2026

The Indian GST ecosystem is increasingly technology-driven. The GSTN’s data analytics capabilities have grown significantly and the tax department now uses AI-based risk profiling to detect mismatches between E-Way Bill data, GST returns (GSTR-1, GSTR-3B), and e-invoice records. In this environment, data accuracy in the E-Way Bill system is not just an operational nicety it is a compliance necessity.

As confirmed by the official GST Portal (gst.gov.in) , the government is systematically integrating E-Way Bill data with GST return data to cross-verify transactions. Businesses with inconsistent or incomplete EWB data face higher scrutiny during GST audits and assessments.

Section 129 of the CGST Act empowers tax officers to detain and seize goods in transit if E-Way Bill requirements are not met. Section 122 provides for penalties in case of non-compliance. The financial and operational cost of non-compliance including detention of goods, penalties, and audit exposure far outweighs the investment needed to prepare correctly.

How Adwani & Co LLP Can Help with E-Way Bill Compliance

At Adwani & Co LLP, we have been supporting businesses with GST compliance, advisory, and technology readiness since the introduction of GST in India. CA Veena Adwani and the firm’s indirect tax team regularly assist clients in:

- Conducting GSTIN master data audits and cleansing exercises

- Reviewing ERP configurations for GST and E-Way Bill compliance

- Liaising with ERP vendors and GSPs for API update readiness

- Preparing internal compliance SOPs and training material for teams

- Conducting pre-implementation reviews and mock drills

- Providing ongoing GST advisory to ensure seamless compliance

With over four decades of professional practice founded on the principles established by our firm’s founder, Advocate N.T. Adwani in 1977 Adwani & Co LLP brings a combination of technical expertise, regulatory depth, and practical business understanding to every engagement.

E-Way Bill Changes and the Broader GST Technology Shift

The E-Way Bill changes deferred to August 2026 are part of a larger wave of GST technology upgrades. Recent years have seen the rollout of e-invoicing (now mandatory for businesses above ₹5 crore turnover), the introduction of the Invoice Management System (IMS) for better ITC reconciliation, and increasing integration between the Income Tax Department and GST systems for cross-verification of financial data.

As the Income Tax Department of India and the GST Council continue to harmonise their data frameworks, the accuracy of your GST filings and E-Way Bill records will increasingly determine your risk profile across both direct and indirect tax assessments.

The message is clear: GST compliance preparedness is no longer optional. It is a core business function and organisations that invest in it proactively will enjoy smoother audits, cleaner credit flows, and lower regulatory risk.

Learn about our Virtual CFO & Strategic Finance services →

Conclusion: August 2026 Will Arrive Faster Than You Think

The GSTN’s decision to defer the E-Way Bill changes to 1 August 2026 is a practical and welcome relief but it must be treated as a deadline, not a safety net. Businesses that use the coming weeks to validate their GSTIN master data, update their ERP systems, and train their teams will navigate the transition smoothly. Those that wait will face avoidable disruption at precisely the moment their competitors are moving ahead.

The two changes mandatory “Ship To GSTIN” capture and Voluntary Closure of E-Way Bill are individually straightforward, but implementing them across a complex ERP and logistics landscape requires careful planning and execution. Start now.

As CA Veena Adwani often advises clients: “In compliance, the cost of being early is negligible. The cost of being late can be severe.”

1.What are the new E-Way Bill changes effective 1 August 2026?

From 1 August 2026, two key E-Way Bill changes come into effect: (1) the mandatory capture of the “Ship To GSTIN” in all Bill-To / Ship-To E-Way Bill transactions, and (2) the introduction of the Voluntary Closure of E-Way Bill facility. Both were originally scheduled for 15 June 2026 but were deferred by GSTN to allow businesses more time to prepare.

2. Why did GSTN defer the E-Way Bill update from june to August 2026?

GSTN deferred the implementation to allow businesses, ERP software vendors, GST Suvidha Providers (GSPs), and GST technology partners adequate time to update their systems, integrate new APIs, validate master data, and train their operational teams. The deferment reflects a practical, industry-sensitive approach to change management in the GST ecosystem.

3. What exactly is “Ship To GSTIN’ in the E-Way Bill context?

In Bill-To / Ship-To transactions, goods are billed to one registered entity but physically delivered to a different location or entity. The “Ship To GSTIN” is the GST Identification Number of the actual consignee at the delivery location. From August 2026, this field will be mandatory in E-Way Bills, ensuring a complete digital trail from the point of sale to the point of delivery.

4. How does the voluntary closure of E-Way Bill feature work?

The Voluntary Closure feature allows the generator of an E-Way Bill to proactively mark it as closed once the goods have been delivered before the EWB’s automatic validity period expires. This prevents misuse of open EWBs after actual delivery, improves EWB lifecycle management, and maintains data cleanliness in the GSTN system.

5.What happens if a business fails to comply with E-Way Bill rules?

Non-compliance with E-Way Bill requirements can attract serious consequences under the CGST Act, 2017. Section 129 empowers tax officers to detain and seize goods in transit. Section 122 provides for penalties for non-compliance. In addition, discrepancies in EWB data relative to GST returns can trigger scrutiny notices and audit proceedings from the GST department.

6.Does the E-Way Bill change apply to all businesses in India?

The mandatory “Ship To GSTIN” requirement applies specifically to Bill-To / Ship-To transactions i.e., where the billing party and the delivery party are different. Businesses that frequently undertake such transactions (e.g., manufacturers, distributors, FMCG companies) are most immediately affected. However, all businesses generating E-Way Bills should review their processes to determine applicability.

7.Where can I find official updates on E-Way Bill changes?

Official E-Way Bill notifications and technical advisories are published on the GSTN E-Way Bill Portal (ewaybillgst.gov.in) and the GST Portal (gst.gov.in). Always refer to these authoritative government sources for the latest regulatory notifications. For personalised advisory, you can reach out to Adwani & Co LLP.

Ready for E-Way Bill Changes? Let Adwani & Co LLP Guide You

Do not wait until August. Our expert GST and compliance team can review your E-Way Bill readiness, audit your GSTIN master data, and ensure your systems are configured correctly long before the 1 August 2026 deadline.

📞 Schedule a Consultation Explore GST Services

Author

CA Veena Adwani is a Chartered Accountant associated with Adwani & Co and is actively involved in statutory compliance and systems audit assignments.