By CA Dipesh Gurubakshani Updated: May 2026 9 min read

The bank advertised your loan at 6%. But when the first EMI hit your account, the numbers didn’t add up. You weren’t wrong — the bank was. Understanding hidden loan costs is not optional anymore. It can save you lakhs of rupees over the life of a loan.

Millions of Indian borrowers sign loan agreements every year without fully understanding what they are committing to. The advertised interest rate — whether it’s 6%, 8.5%, or 12% — is rarely the true cost of borrowing. Hidden loan costs, undisclosed fees, and misleading marketing practices leave borrowers paying significantly more than they ever anticipated. This guide, brought to you by Adwani and Company, breaks down every layer of the hidden loan costs that lenders conveniently leave out of their brochures.

Why Hidden Loan Costs Are the Biggest Financial Trap

When a lender advertises a “6% home loan” or a “10% personal loan,” they are typically quoting a nominal interest rate — not the Annual Percentage Rate (APR) or the effective cost of credit. This distinction is critical, and most borrowers don’t know it exists.

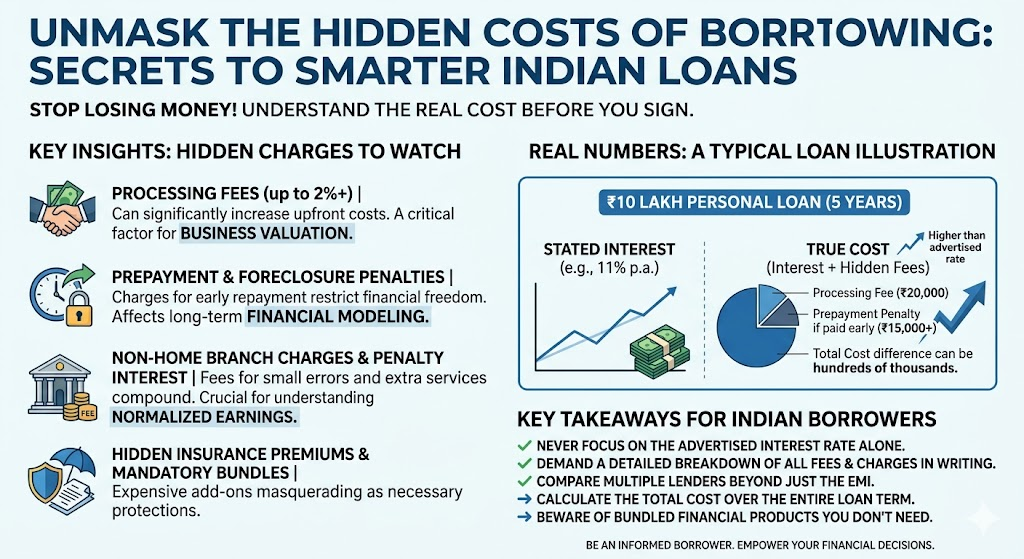

Hidden loan costs are charges added on top of the stated interest rate that inflate the true cost of your loan. These can include processing fees, administrative charges, insurance premiums bundled without consent, prepayment penalties, late payment fees, and documentation charges. When you add these up over a 15 or 20-year home loan, the difference between the advertised rate and what you actually pay can run into lakhs — sometimes even tens of lakhs.

According to the Reserve Bank of India (RBI), lenders are required to disclose the Annual Percentage Rate (APR) transparently. Yet, in practice, these disclosures are often buried in fine print, disclosed only at the time of disbursement, or communicated in ways that most borrowers cannot interpret without professional help.

“A loan is not just what you borrow — it is everything you will pay back, including what was never clearly disclosed.”

The Most Common Hidden Loan Costs in India

To fully grasp the hidden loan costs embedded in your borrowing agreement, you need to know exactly what to look for. Here are the most prevalent charges:

1. Processing Fees

Processing fees are typically charged as a percentage of the loan amount — usually between 0.5% and 2%. On a ₹50 lakh home loan, a 1% processing fee means you pay ₹50,000 before your loan even begins. This hidden loan cost is non-refundable, even if your loan application is rejected after payment.

2. Insurance Premiums — Bundled Without Full Transparency

Many lenders bundle life insurance or loan protection insurance with your loan and include the premium in the loan amount itself. This increases your principal — and therefore your interest outgo — for the entire loan tenure. The borrower often isn’t clearly told that this is optional. This is one of the most insidious hidden loan costs in the Indian banking system.

3. Prepayment and Foreclosure Penalties

If you come into money and want to repay your loan early, many lenders — especially those offering fixed-rate loans — charge a prepayment penalty of 2% to 4% on the outstanding amount. The RBI has banned foreclosure charges on floating-rate home loans for individual borrowers, but this protection does not apply to all loan types. Always verify this before signing.

4. Documentation and Legal Charges

Legal verification fees, stamp duty on loan agreements, CERSAI registration charges, and document handling fees are frequently not disclosed upfront. These can add ₹10,000 to ₹30,000 to the cost of a home loan — small percentages that silently inflate the true borrowing cost.

5. MCLR vs. Repo Rate — When the Benchmark Matters

Home loans linked to MCLR (Marginal Cost of Funds Based Lending Rate) reset less frequently than those linked to the RBI Repo Rate. If interest rates fall, borrowers on MCLR-linked loans benefit much later than those on repo-linked products. This is a structural hidden loan cost that many borrowers discover only years into their tenure.

6. Goods and Services Tax (GST) on Loan Services

Processing fees, prepayment charges, and many loan-related services attract 18% GST as per the GST Portal guidelines. This is rarely highlighted in loan advertisements and adds to the effective borrowing cost. Learn more about GST compliance for financial transactions on our resources page.

A Real Example: The ₹50 Lakh Home Loan That Wasn’t 8%

Illustrative Example — Home Loan Cost Breakdown

A borrower takes a ₹50 lakh home loan for 20 years at an advertised rate of 8%. Here’s what the actual cost looks like when hidden loan costs are included:

₹50L

Loan Amount

8%

Advertised Rate (Nominal)

₹1,00,000

Processing Fee (2%)

₹42,000

Insurance Premium (bundled)

₹22,000

Legal + Documentation Fees

~9.3%

Effective APR (Approx.)

The total upfront hidden loan costs alone amount to over ₹1.64 lakh — more than 3% of the loan amount — before the borrower receives a single rupee. Over 20 years of EMIs, the true cost diverges significantly from what was advertised.

This is precisely why consistently we advise clients to request a full APR disclosure and amortization schedule from lenders before signing any loan document. A difference of even 1% in effective interest rate on a ₹50 lakh loan over 20 years translates to over ₹8 lakh in additional outgo.

Also Read: https://www.adwaniandco.com/blog/gst-show-cause-notices

What Indian Law Says About Disclosing Hidden Loan Costs

The regulatory framework in India is clear, even if enforcement is imperfect. The RBI’s Fair Practices Code mandates that all lenders — banks, NBFCs, and housing finance companies — must:

- Provide a clear loan agreement with all charges stated before disbursement

- Disclose the APR (Annualised Percentage Rate) in the loan sanction letter

- Not alter loan terms unilaterally without the borrower’s written consent

- Not levy foreclosure charges on floating-rate home loans to individual borrowers

Additionally, the Ministry of Corporate Affairs (MCA) regulates the corporate governance of lending institutions, and violations of transparent disclosure norms can be reported to the RBI’s Banking Ombudsman Scheme. If you believe you have been misled about hidden loan costs, you have legal recourse.

Read our detailed guide on your rights as a borrower under RBI guidelines to understand how to protect yourself legally.

Did you know? Under Section 17 of the Consumer Protection Act, 2019, misleading advertisements — including those that obscure the true cost of a loan — can constitute an unfair trade practice and are actionable before Consumer Disputes Redressal Commissions.

How to Calculate the True Cost of Your Loan

There are two metrics every informed borrower should demand from their lender before signing:

1. Annual Percentage Rate (APR)

APR is the most accurate measure of the true cost of a loan. It includes the nominal interest rate plus all fees, charges, and costs associated with the loan, expressed as an annualized percentage. Always compare loans using APR — not the headline interest rate. A loan at 8% nominal with 2% processing fees can have an APR closer to 9.5% in the first year.

2. Total Interest Outgo Over Tenure

Ask your lender for the complete amortization schedule. This document shows you month-by-month how much of each EMI goes toward principal versus interest. For a ₹50 lakh loan at 8% over 20 years, the total interest alone amounts to approximately ₹50 lakh — you effectively pay back double the loan amount before counting any hidden loan costs.

At Adwani and Company, we regularly assists clients in interpreting amortization schedules, comparing loan offers across multiple lenders, and negotiating better terms particularly for home loans, business loans, and education loans. Learn more about our loan advisory and financial planning services.

5 Proven Strategies to Avoid Hidden Loan Costs

- Always demand the APR in writing — not just the nominal rate — before submitting any loan application

- Read every line of the sanction letter before accepting. The sanction letter is a legal document and binds you to its terms

- Opt out of bundled insurance unless you have independently verified its value and cost — it is almost always optional

- Check if your lender has a floating or fixed rate and understand what happens when the RBI changes the repo rate

- Consult a qualified CA before signing — professional review of loan documents can prevent expensive mistakes that last decades

The Digital Age of Lending and New Hidden Loan Costs

The rise of fintech lending, Buy Now Pay Later (BNPL) platforms, and instant digital loans has introduced an entirely new category of hidden loan costs. Many digital lenders advertise “0% interest” loans but recover their margins through flat processing fees, convenience charges, and mandatory subscription plans. A ₹10,000 BNPL loan with a ₹400 “convenience fee” and ₹200 monthly “account management fee” carries an effective annual cost well above 70%.

Digital borrowers are particularly vulnerable because the application process is fast, paperwork is minimal, and borrowers rarely pause to examine the effective cost. The rule is the same regardless of the channel: demand full cost disclosure before borrowing.

The Income Tax Department also takes note of loan-related costs processing fees on business loans are deductible under Section 37(1) of the Income Tax Act as a business expense. If you are a business borrower, understanding and properly documenting these hidden loan costs can reduce your tax liability. Read our detailed guide on business loan tax deductions in India.

Conclusion: Know What You Borrow : Not Just What You Sign

The gap between the loan that was advertised and the loan that was delivered is not an accident. Hidden loan costs are a systematic feature of how lending is marketed in India. Understanding them is not just financially prudent — it is an act of self-protection in a system that favors informed borrowers.

The advertised rate is the entry point of a conversation. The APR, the amortization schedule, the insurance disclosure, the prepayment clause, the GST on fees — these are the substance of the deal. Before you commit to a loan that will follow you for 10, 15, or 20 years, make sure you are reading the full document, not just the headline number.

a borrower who understands the hidden loan costs in their agreement is never truly trapped by them.

Frequently Asked Questions

01. What is the difference between the advertised loan interest rate and the actual cost of the loan?

The advertised rate is the nominal interest rate usually the base rate applied to your principal. The actual cost of a loan includes processing fees, insurance, documentation charges, GST on fees, and other charges, all of which inflate the effective rate. The Annual Percentage Rate (APR) captures all these hidden loan costs and is the most reliable figure for comparison.

02. Are banks in India required to disclose all loan charges upfront?

Yes. Under the RBI’s Fair Practices Code, banks and NBFCs are required to disclose all charges and the APR in the loan sanction letter before disbursement. However, compliance varies, and borrowers must proactively ask for full cost disclosures rather than relying on what is volunteered.

03. Can I negotiate processing fees and other hidden loan costs with my bank?

Absolutely. Processing fees, documentation charges, and even prepayment penalty clauses are often negotiable especially for high-value loans or existing relationship customers. A Chartered Accountant or financial advisor can help you negotiate better loan terms before signing.

04. What is a prepayment penalty and when does it apply?

A prepayment penalty is a charge levied when you repay your loan before the agreed tenure. For floating-rate home loans to individual borrowers, the RBI has prohibited foreclosure charges. However, fixed-rate loans, business loans, and many personal loans may still carry prepayment penalties of 2%–4% of the outstanding balance. Always verify this before signing.

05. How do hidden loan costs affect my EMI?

In most cases, hidden loan costs like insurance premiums are added to the loan principal, which directly increases your EMI. Processing fees and GST are typically deducted upfront from the disbursed amount, meaning you receive less money than the sanctioned loan amount but pay EMIs on the full amount.

06. Can I file a complaint if I was not informed about hidden loan costs?

Yes. You can file a complaint with the RBI Banking Ombudsman if a regulated lender fails to disclose charges as required. Under the Consumer Protection Act, 2019, non-disclosure of material facts in a financial product can also constitute an unfair trade practice, actionable before Consumer Commissions.

07. Are processing fees on a business loan tax deductible?

Yes. Under Section 37(1) of the Income Tax Act, 1961, processing fees and other loan-related charges for business loans are allowable as a deductible business expense, provided they are incurred wholly and exclusively for business purposes and are properly documented. Consult a CA for proper treatment in your books of accounts.

About the Author

CA Dipesh Gurubakshani is a Chartered Accountant with Adwani & Co LLP, Pune, specialising in income tax audit, direct taxation, and accounting advisory. He supports clients across statutory compliance, financial reporting, and income tax matters with a focus on accuracy, regulatory adherence, and disciplined execution.

Leave a Reply