CA Dipesh Gurubakshani June 2026 14 min read

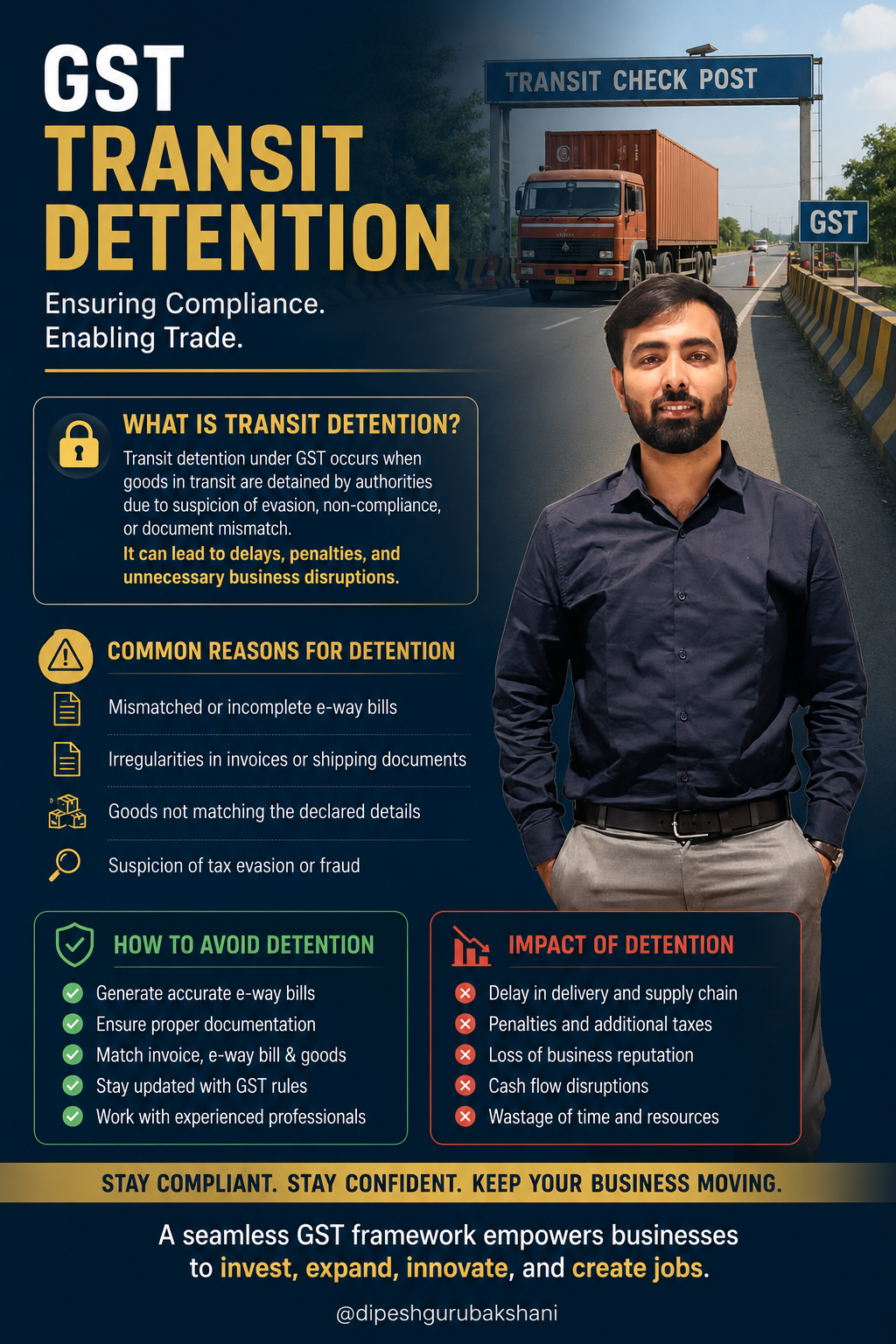

GST Transit Detention

Scenario: Valid Documents. Still Detained.

Your truck has been stopped. The GST inspector reviews every document. The tax invoice is valid. The e-way bill is current. The goods match the description exactly. No quantity discrepancy. No classification mismatch.

And then: “These goods are worth ₹10 lakh. You have invoiced them at ₹5 lakh. I am detaining the consignment.” Can a GST officer legally do this? The answer under Indian GST law is nuanced, consequential, and widely misunderstood.

GST transit detention has become one of the most contested areas of indirect tax enforcement in India. Businesses face enormous disruption when goods are detained mid-journey halted trucks, storage costs, delayed deliveries, unhappy buyers, and potential penalty demands. Yet not all detentions are legally equal. The law draws a sharp line between a genuine GST valuation dispute and deliberate tax evasion, and understanding that line is essential for every business that moves goods under the GST framework.

In this authoritative guide, Dr. Haresh Adwani, PhD in Commerce and law graduate, and senior partner at Adwani & Co LLP, Pune, unpacks the legal framework governing GST goods detained during transit, the officer’s powers, the taxpayer’s rights, and the correct remedy for each situation.

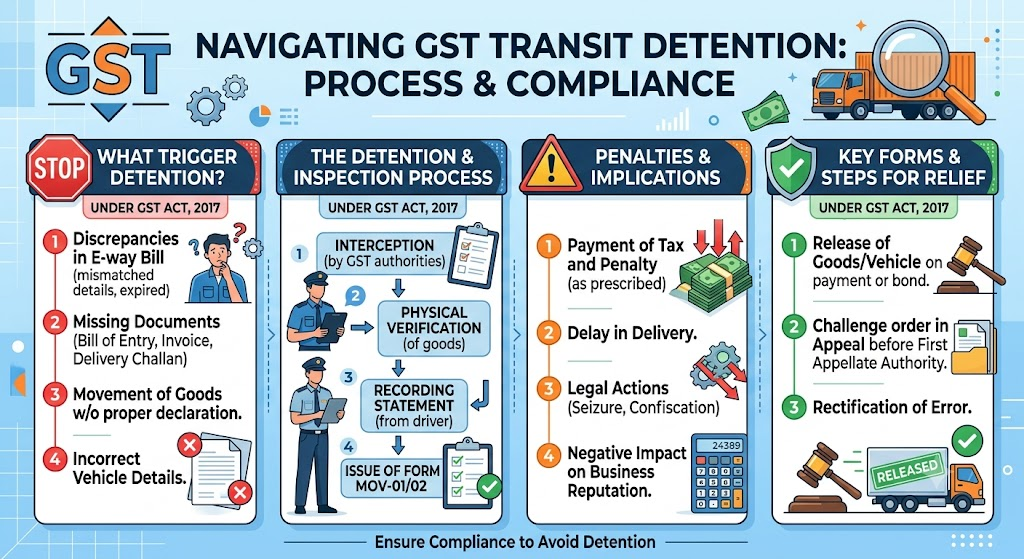

What Is GST Transit Detention? Understanding Section 68 and Rule 138B

Under the GST law, the movement of goods above a specified value must be accompanied by an e-way bill. The CGST Act and CGST Rules empower designated officers to intercept any conveyance carrying taxable goods to verify the correctness of the e-way bill and the accompanying invoice. This power is conferred by Section 68 of the CGST Act, 2017, and operationalised through Rule 138B of the CGST Rules.

When goods are intercepted, the officer is empowered to inspect the documents and the physical consignment. If the officer finds a discrepancy or believes there is one the goods may be detained under Section 129 of the CGST Act, pending payment of applicable tax and penalty, or pending adjudication.

The critical statutory boundary here is this: the officer’s mandate under Section 68 is to verify the legality of the movement of goods. The provision does not confer powers to determine the commercial or market valuation of the goods being transported. That is a separate function governed by a separate statutory framework entirely.

Learn more about our GST Advisory Services to understand how Adwani & Co LLP supports businesses during transit inspections and departmental proceedings.

GST Valuation Dispute vs Tax Evasion: The Critical Legal Distinction

This is the question at the heart of every contested GST transit detention involving invoice value: is a low invoice price automatically evidence of tax evasion?

The answer is no — and the law is clear on why.

GST Valuation Is Governed by Section 15 of the CGST Act

Section 15 of the CGST Act, 2017 establishes that the value of a taxable supply is ordinarily the transaction value the price actually paid or payable provided the supplier and recipient are not related parties and the price is the sole consideration for the supply. The CGST Valuation Rules (Rules 27 to 35 of the CGST Rules, 2017) provide additional methods for determining value when the transaction value is not acceptable.

Crucially, challenging the transaction value under Section 15 requires evidence, adjudication, and a structured legal process. It requires the department to examine pricing agreements, cost structures, market comparisons, commercial context, and the relationship between buyer and seller. None of these can be meaningfully evaluated at a transit checkpoint in real time.

As Dr. Haresh Adwani explains: “A valuation dispute is a matter of law and evidence. The roadside is not the courtroom. GST transit detention on the sole ground that an invoice price ‘appears low’ without corroborating evidence of fraud is ordinarily not legally sustainable.”

What Constitutes Tax Evasion During Transit?

The distinction sharpens when we look at what actually constitutes actionable tax evasion during the movement of goods. The following circumstances would support legal detention and further proceedings:

- Physical goods do not match the invoice description different product, grade, or quantity

- The e-way bill has expired, does not cover the goods, or contains materially incorrect particulars

- Intelligence reports or contemporaneous evidence suggest fake invoices or circular trading

- The consignment is accompanied by two sets of invoices one for the officer, one for the actual transaction

- Physical inspection reveals goods that are entirely different from what is declared

In these situations, the officer’s powers under Section 129 and, in more serious cases, Section 130 for confiscation are squarely applicable. GST transit detention is legally defensible where it is backed by specific, documented evidence of fraud or deliberate misdeclaration not by a subjective assessment of whether the price seems right.

Numerical Example: Valuation Dispute vs Tax Evasion in GST Transit

To make this concrete, consider the following side-by-side comparison the type of analysis the Adwani & Co LLP team regularly prepares when advising clients facing transit disputes

| Factor | Scenario A: Valuation Dispute | Scenario B: Tax Evasion |

| Invoice Value | ₹5 lakh (genuine price) | ₹5 lakh (actual value ₹10 lakh) |

| Documentation | Valid invoice, valid e-way bill, goods match | Fake invoices, goods mismatch, double billing |

| Officer’s Grounds | Suspects price is below market no evidence | Intelligence report, physical discrepancy |

| Correct Legal Path | Adjudication under Section 15 CGST + Valuation Rules | Detention under Section 129; proceedings under Section 130 |

| GST Transit Detention? | Not ordinarily sustainable on valuation alone | Legally sustainable with corroborating evidence |

In Scenario A, the business has a legitimate commercial reason for the price perhaps a long-term supply agreement, a bulk discount, or an intra-group pricing policy. In Scenario B, the price suppression is a cover for tax evasion and is supported by concrete evidence. Only Scenario B justifies GST transit detention. Scenario A requires a proper adjudication process and the taxpayer retains the right to contest the demand.

GST Transit Detention Under Section 129: Taxpayer Rights and Remedies

If your goods are detained under Section 129 of the CGST Act, understanding your rights is the first step to an effective response. Dr. Haresh Adwani, who has guided numerous businesses through GST transit disputes and departmental proceedings, identifies the following non-negotiable rights for detained taxpayers:

1. Right to a Written Detention Order

The officer must issue a written order specifying the grounds for GST transit detention. Verbal instructions are not sufficient. Do not allow goods to be detained without a written order in hand.

2. Right to Pay Under Protest to Secure Release

Under Section 129(1) of the CGST Act, the owner or transporter may pay the applicable tax and penalty to secure the release of detained goods. Critically, payment under protest does not amount to an admission of liability. The taxpayer retains the right to contest the demand through the appeals mechanism.

3. Right to Appeal

If the officer’s detention order is challenged, the matter proceeds to adjudication. Appeals lie before the Appellate Authority under Section 107 of the CGST Act. Decisions of the Appellate Authority may be further challenged before the GST Appellate Tribunal and, thereafter, before the High Court.

4. Right to Legal Representation

Taxpayers are entitled to be represented by a qualified professional a Chartered Accountant, Cost Accountant, or Advocate at all stages of detention proceedings. Engaging experienced GST counsel at the earliest stage significantly improves outcomes.

Read our detailed guide on GST Notice 2026: What Businesses Miss

How Adwani & Co LLP Handles GST Transit Detention Cases

At Adwani & Co LLP, a Pune-based firm founded in 1977 and led by Dr. Haresh Adwani, we have advised businesses ranging from manufacturing units and commodity traders to e-commerce sellers and pharmaceutical distributors on GST transit matters. Our approach is systematic:

- Immediate assessment of the detention order to identify whether grounds are legally tenable

- Preparation of a response brief within 24–48 hours citing applicable GST valuation provisions, CBIC circulars, and judicial precedents

- Decision analysis on whether to pay under protest for quick release or contest the detention order

- Filing of replies before the adjudicating authority with documentary evidence pricing policies, purchase agreements, prior transaction history

- Representation before the Appellate Authority and High Court where required

The GST Portal (gst.gov.in) and the Central Board of Indirect Taxes and Customs (cbic.gov.in) have issued multiple circulars clarifying the scope of officer powers during transit inspections. Staying current with this guidance is essential and it is part of what Adwani & Co LLP brings to every client engagement.Learn more about our GST Compliance Services for Businesses to see how we help companies build robust compliance frameworks that reduce the risk of transit disputes before they arise.

Proactive Steps to Protect Your Business from GST Transit Detention

The most effective strategy against GST transit detention is preparation. As Dr. Haresh Adwani consistently advises clients: the checkpoint is not the place to start building your defence. Build it before the truck leaves the warehouse.

- Maintain a written pricing policy document especially if you sell below MRP, offer bulk discounts, or supply to related parties

- For related-party transactions, comply with GST Valuation Rules 28 to 33 and maintain contemporaneous documentation of the pricing basis

- Generate e-way bills accurately covering full value, correct HSN code, and complete vehicle/transporter details

- Train warehouse and logistics staff on their rights if goods are intercepted: demand written orders, do not move goods without documentation

- Retain a GST advisor who can be reached immediately if goods are detained the first few hours of a detention often determine the outcome

Q: Can GST officers detain goods during transit solely because the invoice price appears low?

A: Not ordinarily. A mere difference between invoice value and perceived market value without corroborating evidence of fraud or misdeclaration is insufficient grounds for GST transit detention. Valuation disputes must be resolved through adjudication under Section 15 of the CGST Act, not at a transit checkpoint.

Q: What is Section 129 of the CGST Act and how does it apply to detained goods?

A: Section 129 of the CGST Act governs the detention, seizure, and release of goods and conveyances in transit. It allows the owner or transporter to secure release by paying applicable tax and penalty. The section also provides for adjudication if the taxpayer disputes the detention.

Q: What documents must a transporter carry to avoid GST transit detention?

A: A transporter must carry a valid tax invoice (or delivery challan, as applicable), a valid and current e-way bill covering the full value and correct description of goods, and vehicle details matching the e-way bill. Any discrepancy between documents and physical goods significantly increases detention risk.

Q: Is paying the GST demand at the transit checkpoint an admission of tax evasion?

A: No. Payment made under Section 129 to secure the release of detained goods does not constitute an admission of liability. The taxpayer retains the right to contest the underlying demand through the GST appeals process, starting with the Appellate Authority under Section 107 of the CGST Act.

Q: What is the difference between Section 129 and Section 130 of the CGST Act in transit cases?

A: Section 129 deals with detention and release of goods upon payment of tax and penalty. Section 130 deals with confiscation a more severe outcome applicable when goods are found to be liable for confiscation (e.g., used in deliberate tax evasion). Confiscation under Section 130 follows from non-payment or continued dispute after Section 129 proceedings.

Conclusion:

GST transit detention sits at the intersection of taxpayer rights and enforcement authority and it is an area where legal clarity matters enormously. The law has drawn a clear distinction: a valuation dispute requires evidence, adjudication, and due process. It is not a ground for roadside detention on the basis of a price that ‘looks suspicious’. Tax evasion, on the other hand supported by concrete evidence of fake invoices, misdeclaration, or circular trading is fully actionable under Sections 129 and 130 of the CGST Act.

For businesses, the message is equally clear. Proactive compliance accurate e-way bills, documented pricing policies, trained logistics staff, and immediate access to qualified legal and tax counsel is the strongest shield against unjustified GST transit detention.

Dr. Haresh Adwani summarises it well: “The law protects legitimate commerce and punishes deliberate fraud. Businesses that operate transparently and document their pricing decisions have little to fear from transit inspections. Those who use documentation as a cover for evasion should expect consequences.”

Author

CA Dipesh Gurubakshani is a Chartered Accountant with Adwani & Co LLP, Pune, specialising in income tax audit, direct taxation, and accounting advisory. He supports clients across statutory compliance, financial reporting, and income tax matters with a focus on accuracy, regulatory adherence, and disciplined execution.

Legal Disclaimer: This article is published for informational and educational purposes only. Nothing contained herein constitutes legal, financial, or tax advice, nor should it be treated as a substitute for professional consultation tailored to your specific circumstances. Tax laws, rates, and provisions are subject to change; readers are strongly advised to consult a qualified Chartered Accountant or tax advisor before acting on any information in this article.

All content is original. References to government portals and statutory provisions are paraphrased for educational purposes in compliance with fair use principles. No content has been reproduced from third-party sources

Facing a GST Transit Detention or Valuation Dispute?

Adwani & Co LLP has been advising businesses on GST compliance, transit disputes, and departmental proceedings since 1977. Our team combines deep technical expertise with practical litigation experience to protect your business and resolve disputes efficiently.Connect with Adwani & Co LLP today adwaniandco.com