AI in Tax

Everyone is asking whether AI can prepare tax returns. Almost nobody is asking the more important question: who will defend the tax position behind them?

That single question who defends the reasoning, not just the numbers is quietly reshaping the future of tax compliance across India and globally. And for businesses, founders, and professionals navigating the increasingly scrutinised landscape of income tax, GST compliance, and cross-border taxation in 2026, it is the question that matters most.

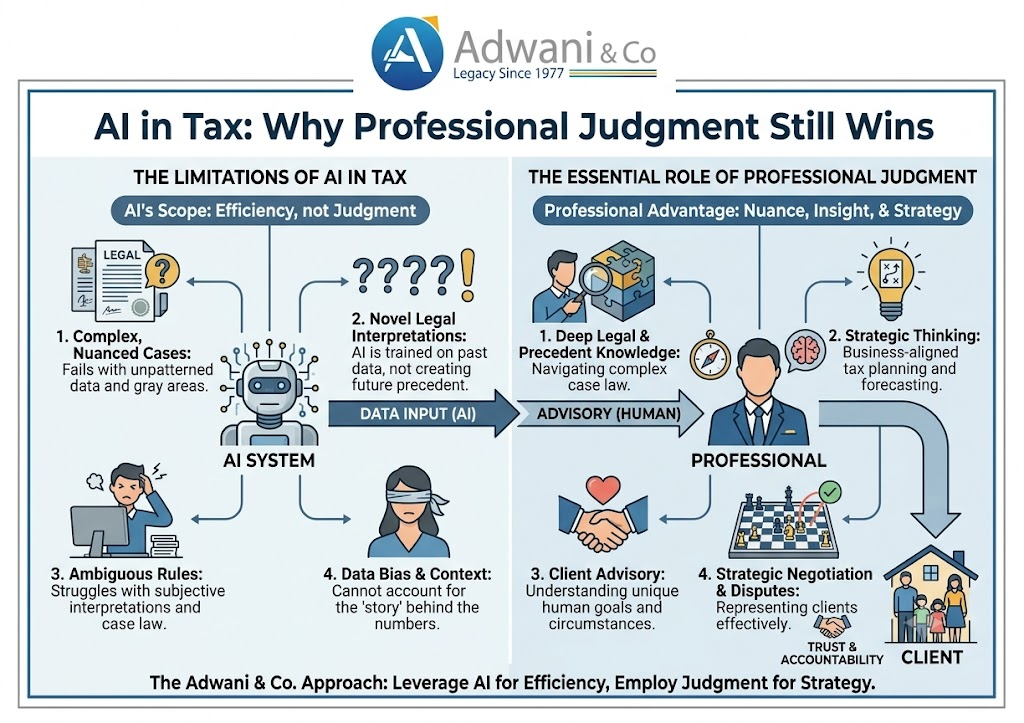

AI in tax return preparation is already impressive. It extracts data from documents, populates schedules, identifies missing information, and generates draft returns in minutes. The Income Tax Department’s own AIS (Annual Information Statement) system and the GST Portal now integrate AI-driven analytics to detect mismatches before a return even reaches a scrutiny desk. In that environment, a technically accurate return is just the starting point not the finish line.

The real risk in modern tax compliance is not a calculation error. It is a reasoning error. And reasoning errors are exactly where AI in tax professional judgment gaps show up most sharply.

AI in Tax Compliance: What It Does Well in 2026

To be fair to the technology, AI is genuinely transforming the mechanics of tax compliance. What previously took hours of manual data entry now happens in minutes. For routine income tax return filing, GST return preparation, and reconciliation tasks, AI-assisted tools have meaningfully improved speed and reduced data-entry errors.

The capabilities that AI brings to tax compliance include:

- Extracting structured data from invoices, bank statements, Form 16, and TDS certificates

- Pre-populating ITR forms based on AIS and Form 26AS data available on the Income Tax Department portal

- Identifying gaps between GSTR-1 and GSTR-3B or flagging GSTR-2B mismatches before filing

- Generating draft tax computations with standard deduction and exemption claims

- Flagging potential income tax notice triggers based on patterns in prior filings

These are genuine productivity gains. A CA firm that uses AI tools intelligently can serve more clients, reduce routine errors, and spend less time on administrative work.

But productivity is not the same as judgment. And in taxation especially for businesses managing GST compliance 2026, handling cross-border transactions, or responding to income tax notices judgment is where the real risk lives.

Why AI in Tax Return Preparation Is Not Enough on Its Own

Consider a straightforward scenario.

A business files its ITR. The numbers are correct. Every document is available. The return passes all system validation checks. Yet three critical questions remain unanswered:

The Questions AI Cannot Answer for You

→ Is the taxpayer actually eligible for the benefit claimed?

→ Does a restriction or limitation provision apply under the Income Tax Act?

→ Is there a more advantageous tax position available that has not been explored?

→ What assumptions underlie the computation, and can they withstand scrutiny?

→ If the Income Tax Department issues a notice, can the position be professionally defended?

These are not edge cases. They represent the core of professional tax advisory and they are precisely where AI in tax professional judgment gaps become expensive.

The Income Tax Department and CBDT have significantly increased their use of data analytics and AI-driven scrutiny. Cross-referencing of ITR data with AIS, TDS data, MCA filings, GST turnover, and banking transactions is now routine. As per guidance available through the Income Tax Department portal, cases are increasingly selected for scrutiny based on risk-scoring models that evaluate the consistency and commercial logic of reported positions not just the arithmetic.

In that environment, a return that is numerically correct but logically indefensible is not a safe return. It is a delayed problem.

A Real-World Tax Risk Example: Where AI Missed and Judgment Mattered

| Practical Example A proprietary trading firm with an annual turnover of ₹3.2 crore used an AI-assisted platform to prepare and file its ITR-3 for AY 2025-26. The AI correctly: • Computed speculative and non-speculative business income separately • Applied the correct tax rates • Populated all required schedules What the AI did not evaluate: • Whether certain derivatives transactions qualified as speculative or non-speculative under Section 43(5) of the Income Tax Act a distinction that affects set-off of losses • Whether the firm’s expenses claimed as business deductions met the ‘wholly and exclusively for business’ test • Whether turnover disclosed in the ITR was consistent with GST returns and bank statements, given the firm also had an NBFC registration Result: An income tax notice was issued under Section 143(2) querying the loss set-off and expense claims. A CA reviewing the return before filing would have identified these risk points and either restructured the position or documented the reasoning making the notice either avoidable or significantly easier to defend. |

This is not a rare situation. It is representative of exactly the kind of reasoning error that automated tax preparation cannot prevent because preventing it requires judgment about facts, law, and professional risk, not just calculation.

AI vs. Professional Judgment in Tax: A Practical Comparison

| What AI Handles Well in Tax Compliance | Where Professional Judgment in Tax Is Required |

| Extracting data from Form 16, TDS certificates, AIS | Evaluating whether all income sources are correctly characterised |

| Populating ITR schedules based on available data | Deciding which ITR form is appropriate given the taxpayer’s income profile |

| Identifying GSTR-1 vs GSTR-3B mismatches | Determining the legal significance of the mismatch and how to resolve it |

| Flagging excess ITC claims against GSTR-2B | Advising whether to reverse ITC, dispute the claim, or pursue vendor rectification |

| Generating draft tax computations | Reviewing whether deductions, exemptions, and set-offs are correctly applied |

| Detecting variance from prior-year filings | Explaining the variance and assessing whether it creates scrutiny risk |

| Preparing income tax notice response templates | Drafting a legally sound reply that addresses the actual notice ground |

Professional Judgment in Tax: What It Actually Means

The phrase is used frequently in professional circles, but it has a concrete meaning in the context of AI in tax compliance.

Interpreting Provisions:Not Just Applying Them

The Income Tax Act, 1961, and the GST law contain thousands of provisions. Many are straightforward. Some are ambiguous, subject to judicial interpretation, or apply differently depending on facts. An AI system applies the provision as trained. A professional interprets it in context.

Dr. Haresh Adwani, a PhD holder in Commerce and a law graduate, regularly applies this dual lens at Adwani and Company evaluating tax positions not only through a finance lens but through the legal framework that governs their validity.

Evaluating Whether Assumptions Are Commercially Defensible

Every tax return carries assumptions about the nature of transactions, the classification of income, the eligibility for benefits. AI generates those assumptions from patterns. A professional evaluates whether they hold up to scrutiny in a specific business context.

Managing Risk Across the Compliance Lifecycle

Tax risk does not end at filing. It extends to assessments, scrutiny, notices, and appeals. Professional judgment in tax includes structuring positions that can be defended through the full lifecycle of compliance not just at the point of return preparation.

As AI-driven scrutiny by the Income Tax Department and GST authorities becomes more sophisticated, the cost of an indefensible position rises. This is the core dynamic reshaping what tax professionals are paid to do.

AI in Tax and the Income Tax Notice Risk

One of the most practical implications of AI in tax compliance for businesses and individuals is the income tax notice risk.

Under Section 143(2), Section 148, and other scrutiny provisions, the Income Tax Department can issue notices based on risk-scoring that increasingly relies on cross-database analytics. The parameters include:

- Significant variation between ITR-reported income and AIS data

- Mismatch between GST turnover and income tax turnover

- High-value transactions without corresponding income disclosure

- Unusual deduction or exemption claims relative to prior years

- Discrepancies between MCA-reported financials and tax filings

An AI-prepared return can tick all the validation checkboxes and still contain the exact kind of inconsistency that triggers one of these notices—because the inconsistency is in the reasoning, not the arithmetic.

This is where Adwani and Company‘s approach to tax advisory adds measurable value. The firm’s review process, guided by Dr. Haresh Adwani‘s academic grounding in Commerce and legal knowledge, evaluates both the technical accuracy and the commercial defensibility of every significant tax position before filing.

Learn more about our ITR Filing 2026: Deadlines, Penalties & Smart Tax Saving Guide.

GST Compliance 2026 and the Same Judgment Problem

Everything said about income tax applies equally and in some ways more acutely to GST compliance in 2026.

AI tools can prepare GSTR-3B, match GSTR-2B for input tax credit reconciliation, and flag vendor-level discrepancies. But the judgment questions in GST compliance are substantial:

- Is a particular supply correctly classified, and has the right GST rate been applied?

- Does a transaction qualify for input tax credit eligibility, or does a restriction under Section 17(5) apply?

- Is an export zero-rated correctly, or does a condition remain unsatisfied?

- When a GST notice arrives questioning ITC claims, is the response legally adequate?

According to compliance advisories and updates available on the GST Portal (gst.gov.in) and cross-referenced with MCA (mca.gov.in) data, authorities are increasingly scrutinising the commercial rationale of transactions—not just their documentation.

A business with ₹80 lakh in ITC claims but a vendor base that shows irregular GSTR-1 filing is not just a documentation risk. It is a legal risk that requires professional assessment and, where necessary, a structured response strategy.

Read our detailed guide on GST Compliance and Notice Response for businesses.

The Most Valuable Tax Skills in an AI-Enabled World

The LinkedIn post that inspired this article asked a pointed question: what will be the most valuable skill in an AI-enabled tax world?

Based on work across diverse client engagements at Adwani and Company, here is a grounded answer:

| High-Value Tax Skills for the AI Era 1. Analytical Review of AI Outputs ability to critically evaluate AI-generated computations, identify reasoning gaps, and flag positions that look correct but carry hidden risk 2. Regulatory Interpretation applying the Income Tax Act, GST law, FEMA, and related frameworks to specific facts in a way that produces a defensible position 3. Risk Communication translating technical tax risk into commercially actionable language for founders, CFOs, and business owners 4. Notice and Litigation Management structuring responses to income tax notices, GST scrutiny, and assessment proceedings with legal and factual rigour 5. Cross-Border Tax Judgment advising on NRI taxation, transfer pricing, DTAA benefits, and FEMA compliance in situations where AI outputs are least reliable |

These are not replaceable skills. They are enhanced by AI but their value lies precisely in the human judgment that AI cannot replicate.

Key Takeaways

| Summary • AI in tax return preparation handles the mechanical and computational layer well data extraction, schedule population, reconciliation flagging. • The gap between an AI-prepared return and a professionally reviewed one lies in reasoning: assumptions, eligibility, risk assessment, and defensibility. • As the Income Tax Department and GST authorities increase AI-driven scrutiny, the cost of indefensible tax positions is rising. • Professional judgment in tax covers interpretation, commercial context, risk management, and accountability across the full compliance lifecycle. • The future of tax practice is not AI replacing professionals it is AI handling scale while professionals provide the judgment that determines outcome. • For any significant tax position, cross-border transaction, notice response, or restructuring, professional review is not a legacy stepit is the critical step. |

Frequently Asked Questions:

1. Can AI tools file income tax returns accurately without a CA reviewing them?

For straightforward salary-based returns with limited income sources, AI tools perform adequately. For business income, capital gains, multiple income sources, or any position that carries interpretation risk—such as deduction eligibility or income characterisation—professional review before filing is strongly recommended. An accurate calculation is not the same as a defensible position.

2. What is the biggest risk in AI-generated tax computations?

The biggest risk is not arithmetic—it is assumption. AI systems apply rules as trained, without evaluating whether those rules apply to the specific facts of a taxpayer’s situation. Where eligibility conditions, limitations, or judgment-based classifications are involved, the AI output may be technically formatted but commercially or legally incorrect.

3. How does the Income Tax Department use AI to scrutinise returns?

The Income Tax Department and CBDT increasingly use risk-scoring systems that cross-reference ITR data with AIS, TDS records, GST turnover, MCA filings, and banking data. Returns are selected for scrutiny based on inconsistency and risk indicators—not just arithmetic errors. A return that is numerically correct but logically inconsistent across data sources can still attract a Section 143(2) notice.

4. What should a business do when it receives an income tax notice?

First, read the notice carefully to identify the specific ground being raised—whether it concerns turnover mismatch, deduction claims, or unreported income. Second, do not respond without professional guidance; an incomplete or poorly structured reply can escalate the matter. Third, engage a qualified CA firm to assess the position and draft a legally adequate response. Adwani and Company provides structured income tax notice reply support across all major notice types.

5. Is professional judgment still needed for GST compliance if I use accounting software?

Yes. Accounting software and AI tools improve GST return preparation speed and reduce data entry errors. They do not evaluate whether your ITC claims are legally valid, whether your GST rate classifications are correct, or whether a vendor-mismatch creates a legal exposure requiring action. GST compliance in 2026 requires both good systems and professional advisory—especially for businesses with complex transactions or ITC-heavy operations.

6. What makes Adwani and Company different from a standard CA firm for tax advisory?

Adwani and Company brings a multi-disciplinary approach to tax advisory. Dr. Haresh Adwani combines a PhD in Commerce with a law degree, allowing the firm to evaluate tax positions through both a financial accounting lens and a legal framework. This is particularly valuable in situations where the tax question involves statutory interpretation, litigation risk, or cross-jurisdictional complexity.

7. How can small businesses use AI in tax without taking on excessive risk?

Small businesses can use AI tools for routine compliance tasks—return preparation, reconciliation, and data organisation—while ensuring that any significant position (deduction claims, ITC eligibility, income characterisation) is reviewed by a qualified professional before filing. Treating AI output as a first draft subject to professional review is the practical approach that balances efficiency with risk management.

Conclusion: Professional Judgment in Tax Is the New Competitive Advantage

AI is not a threat to the tax profession. It is a clarification of what the tax profession is actually for.

When AI handles the mechanical layer data extraction, schedule population, reconciliation flagging what remains is the professional judgment layer: interpretation, risk evaluation, position defence, and client advisory. That layer has always been where the real value sits. AI just makes it more visible.

The future tax professional, as the LinkedIn post that inspired this article noted, will spend less time preparing returns and more time validating assumptions, challenging conclusions, and managing risk. In the context of India’s increasingly analytics-driven tax administration where the Income Tax Department, CBDT, and GST authorities cross-reference multiple data sources in real time that shift is not optional. It is already underway.

For businesses and individuals who want to stay ahead of that curve, the right question is not ‘can AI prepare my return?’ It is ‘who is reviewing the reasoning behind it?’

| Connect With Adwani and Company If you want expert guidance on income tax compliance, GST advisory, tax notice responses, or cross-border taxation, connect with Adwani and Company today. Dr. Haresh Adwani and the team bring the combination of deep tax expertise and legal knowledge that complex tax positions require whether you are a founder filing business income, a company managing GST scrutiny, or an NRI with cross-border tax obligations. → Learn more about our Income Tax Advisory Services → Explore our GST Compliance and Notice Reply Support → Read about our Virtual CFO and Financial Reporting Services Website: adwaniandco.com |

Author

CA Dipesh Gurubakshani is a Chartered Accountant with Adwani & Co LLP, Pune, specialising in income tax audit, direct taxation, and accounting advisory. He supports clients across statutory compliance, financial reporting, and income tax matters with a focus on accuracy, regulatory adherence, and disciplined ex

Leave a Reply