By CA Manish

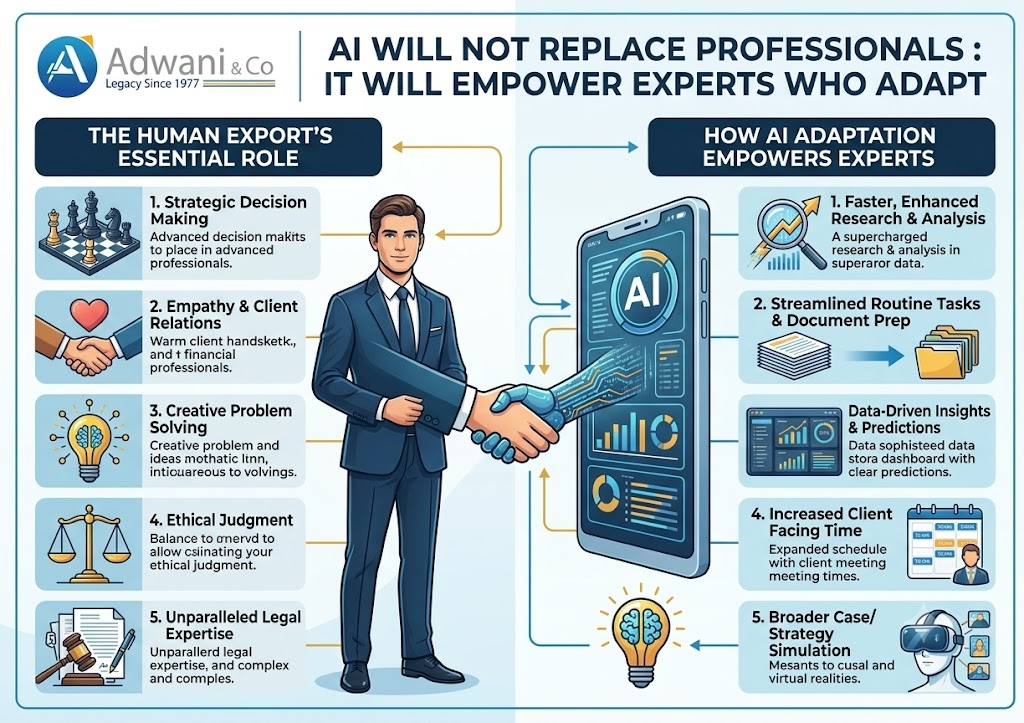

AI Will Not Replace Professionals

The Question Every Professional Is Asking

Will AI take my job?

It is the most common question in boardrooms, CA chambers, law firms, and finance departments across India and globally. And while the anxiety is understandable, most professionals are asking the wrong question or at least framing it incorrectly.

The more productive question is: How do I position myself to work with AI rather than be displaced by it?

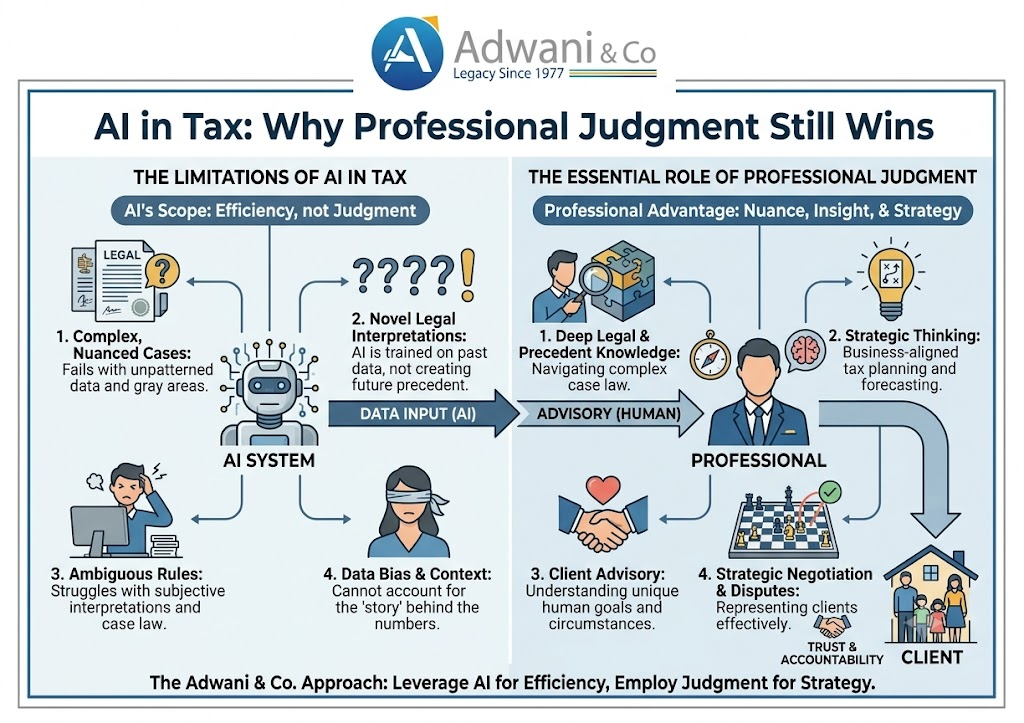

Having been personally involved in training and evaluating Agentic AI models across Indian taxation, US tax compliance, and financial analysis, I can tell you the professionals who will thrive in an AI-driven world are those who bring something no machine can generate on its own: real-world judgment, domain depth, and contextual experience.

What AI Actually Needs to Function

Here is something that often surprises people outside the technology space: AI models, no matter how sophisticated, do not learn from textbooks alone.

Effective AI systems in professional domains are trained on real-world decision-making. They need to understand industry-specific exceptions, regulatory nuances, client scenarios, workflow logic, and professional judgment none of which can be sourced from generic online data alone.

This is precisely where experienced professionals become irreplaceable.

When a large language model is being trained or evaluated for tax advisory, it needs inputs like:

- How a Chartered Accountant thinks through an ITR filing involving multiple income heads

- Why a particular FEMA compliance treatment applies in one cross-border scenario but not another

- How a financial analyst structures a DCF model under real client constraints

- What red flags a seasoned auditor spots in a set of books

These are not answers you find in a compliance manual. They emerge from years of professional practice. And currently, that expertise is in significant demand not despite AI, but because of it.

The Emerging Opportunity: Domain Experts as AI Trainers and Evaluators

The AI industry is entering a phase where the quality of domain-specific training data is becoming the key competitive differentiator.

Building a tax AI for Indian professionals requires Indian tax professionals. Building a financial modeling assistant for global finance teams requires experienced FP&A practitioners and valuation experts. The people who have spent years doing this work are exactly who AI developers need in the room.

What This Looks Like in Practice

Professionals with deep domain expertise are being engaged to:

- Review and annotate AI-generated outputs for technical accuracy

- Develop scenario libraries based on real client cases

- Evaluate model responses for compliance, judgment quality, and practical reliability

- Train AI systems to handle edge cases, exceptions, and regulatory ambiguity

- Build quality benchmarks for AI tools operating in high-stakes advisory settings

These are roles that did not exist five years ago. They require precisely the skills that experienced CAs, tax professionals, lawyers, financial analysts, and industry specialists have spent their careers building.

Which Professionals Are Best Positioned?

Across multiple AI evaluation projects, a clear pattern has emerged: the professionals who bring the most value are those with hands-on, applied expertise rather than purely theoretical credentials.

Professionals particularly well-placed to contribute to AI training and evaluation include:

- Chartered Accountants and Tax Professionals with multi-year client advisory experience

- Financial Analysts and FP&A practitioners familiar with real-world modeling constraints

- Auditors and forensic accountants who can identify anomalies and exceptions

- Legal professionals with regulatory and cross-jurisdictional expertise

- Industry specialists in healthcare, engineering, manufacturing, and supply chains

- NRI and cross-border advisory experts who navigate FEMA, US tax, and double taxation treaties

The common thread? All of these professionals have built something that AI still lacks: the ability to apply judgment in ambiguous, real-world situations.

How Professionals Should Prepare Right Now

The window for professionals to position themselves advantageously in an AI-augmented world is open — but it will not remain so indefinitely. Here is what I would suggest to any professional navigating this transition:

1. Double Down on Core Domain Expertise

AI amplifies expertise it does not substitute for the absence of it. The deeper your knowledge of your professional domain, the more valuable you become as an AI collaborator, trainer, or evaluator. Continuing professional development, advanced certifications, and specialized practice areas all strengthen your position.

2. Understand How AI Systems Are Built

You do not need to become a data scientist or software engineer. But a working understanding of how AI models are trained, how prompts are structured, and how outputs are evaluated gives you a meaningful advantage. This literacy is increasingly available through professional bodies, online courses, and industry events.

3. Articulate Your Practical Experience Clearly

The value AI developers are looking for is not just credentials — it is the specific, real-world scenarios you have worked through. A CA who can describe exactly how they analyzed a complex transfer pricing case, or how they resolved a GST reconciliation issue under audit pressure, is offering something genuinely useful to AI training efforts.

4. Position Yourself as an AI Collaborator

The professionals who will lead in the next decade are those who use AI tools effectively while providing the oversight, judgment, and accountability that clients and regulators will always require. Cultivating this positioning publicly through writing, speaking, or advisory work is a strategic advantage.

The Adwani & Co LLP Perspective

At Adwani & Co LLP, we are actively navigating this intersection between deep professional expertise and emerging AI capabilities. Our work across Indian taxation, international accounting, financial modeling, and cross-border advisory has always been grounded in practical experience which is precisely what the AI economy values.

As CA Manish observes from ongoing AI model evaluation projects: the professionals most sought after by AI developers are not those with the broadest knowledge, but those with the deepest applied judgment in specific domains. The future of professional work is not about competing with AI it is about making AI more useful, more accurate, and more trustworthy by contributing what only experienced humans can provide.

If your firm or practice is thinking about how AI adoption intersects with your advisory workflows, client service delivery, or financial reporting processes, this is a conversation worth having now.

Key Takeaways

- AI systems require real-world professional expertise for training, evaluation, and quality control creating new opportunities for experienced practitioners.

- Domain knowledge in areas like Indian taxation, US accounting, financial modeling, and cross-border advisory is in active demand for AI development projects.

- The professionals most likely to be displaced by AI are those who do not engage with it; those who help build and evaluate AI systems are gaining a first-mover advantage.

- Building deeper domain expertise, understanding AI fundamentals, and positioning yourself as an AI-capable advisor are the three most impactful steps professionals can take right now.

Judgment, contextual reasoning, and professional accountability remain human advantages that AI cannot replicate in high-stakes advisory settings

Read our detailed guide on How Financial Analysts Really Read a P&L Before Building an FP&A Model

Frequently Asked Questions

1.Will AI replace Chartered Accountants in India?

AI is unlikely to replace CAs entirely, particularly those working in complex advisory, international taxation, and strategic reporting. Routine compliance tasks may be increasingly automated, but the judgment-intensive aspects of CA practice cross-border structuring, audit interpretation, business advisory require human expertise. CAs who actively engage with AI tools and contribute to AI training projects are likely to see expanded opportunities rather than displacement.

2.How are professionals involved in training AI models?

Professionals contribute to AI model training through activities such as reviewing and annotating AI-generated outputs, providing expert feedback on model responses, developing scenario libraries based on real client cases, and setting quality benchmarks for AI tools in their domain. These roles are often contract-based engagements with AI development companies and research labs.

3.What skills should finance professionals develop to stay relevant in an AI-driven world?

Beyond maintaining strong core domain expertise, finance professionals should develop familiarity with AI tools used in their field (such as AI-assisted financial modeling or automated bookkeeping review), an understanding of prompt engineering basics, and the ability to critically evaluate AI-generated financial analysis for accuracy and compliance. Communication skills and client advisory judgment remain irreplaceable differentiators.

4.Is there demand for Indian CA and tax professionals in global AI projects?

Yes. Indian taxation, FEMA compliance, cross-border advisory, and international accounting are specialized domains where trained AI models require inputs from qualified Indian professionals. CA Manish has been directly involved in multiple AI evaluation projects across Indian and US tax domains, reflecting the growing global demand for this expertise.

5.How can Adwani & Co LLP help businesses navigate AI adoption in finance?

Adwani & Co LLP provides advisory support at the intersection of traditional finance expertise and emerging AI-augmented workflows. From financial reporting and virtual CFO services to international accounting and FP&A, our team helps businesses build systems that are both AI-ready and professionally robust. Connect with us to explore how your financial operations can evolve with confidence.

Conclusion

The fear that AI will eliminate professional jobs is understandable — but it is driven more by uncertainty than by a clear-eyed assessment of how AI actually works. The reality emerging from live AI development projects is that experienced professionals are not being replaced. They are being recruited.

The professionals who combine deep domain expertise with a genuine understanding of AI capabilities — and the willingness to contribute to shaping those capabilities — will find themselves at the center of the most significant professional transformation in a generation.

Now is not the time to wait and see. Now is the time to go deeper in your domain, engage with AI honestly, and position your expertise where it will be valued most.

| Work With Professionals Who Understand AI Adwani & Co LLP combines deep domain expertise in Indian taxation, international accounting, financial modeling, and cross-border advisory now increasingly integrated with AI-assisted workflows. Whether you are a founder, a finance team, or a professional looking to future-proof your role, our team is here to help. 📧info@adwaniandco.com | 🌐 www.adwaniandco.com | 🌐 www.itradvisor.in Connect with us for international accounting, financial modeling, virtual CFO, and AI-integrated advisory support. |

Explore Our Related Services

- Learn more about our Virtual CFO & Strategic Finance Advisory adwaniandco.com/virtual-cfo

- Explore our Financial Modeling, Valuation & FP&A Services — adwaniandco.com/financial-modeling

- Read about our International Accounting & Cross-Border Advisory adwaniandco.com/international-accounting

- Discover our NRI Tax & FEMA Compliance Services — adwaniandco.com/nri-tax

- Learn about our Indian & US Tax Support for Startups and SMEs itradvisor.in

Disclaimer

Adwani & Co LLP is a multi-disciplinary professional services platform. The blogs shared are for educational and informational purposes only and are intended to promote awareness around finance, accounting, taxation, reporting, and business advisory topics. Nothing contained herein should be construed as solicitation or advertisement of professional services. Where professional services are required under applicable laws or regulations, such services are rendered in accordance with relevant professional and regulatory requirements. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP.

© 2025 Adwani & Co LLP. All rights reserved. | www.adwaniandco.com | www.itradvisor.in