Every tax season, salaried employees and employers spend hours debating what the New Tax Regime took away HRA, LTA, and most of Chapter VI-A. But almost nobody is asking the more useful question: what did it quietly make better? Hidden inside the Income Tax Act is a provision that most taxpayers overlook, and it happens to be one of the few deductions that genuinely improved when the New Tax Regime came into force. That provision is the Section 80CCD(2) deduction, and understanding it properly could change how you and your employer structure salary for FY 2026-27.

If you are a private sector employee, a payroll manager, or a founder trying to design a competitive and tax-efficient compensation package, this guide breaks down exactly how the Section 80CCD(2) deduction works, how much you can legitimately claim, and why so many employers have not yet updated their policies to take advantage of it.

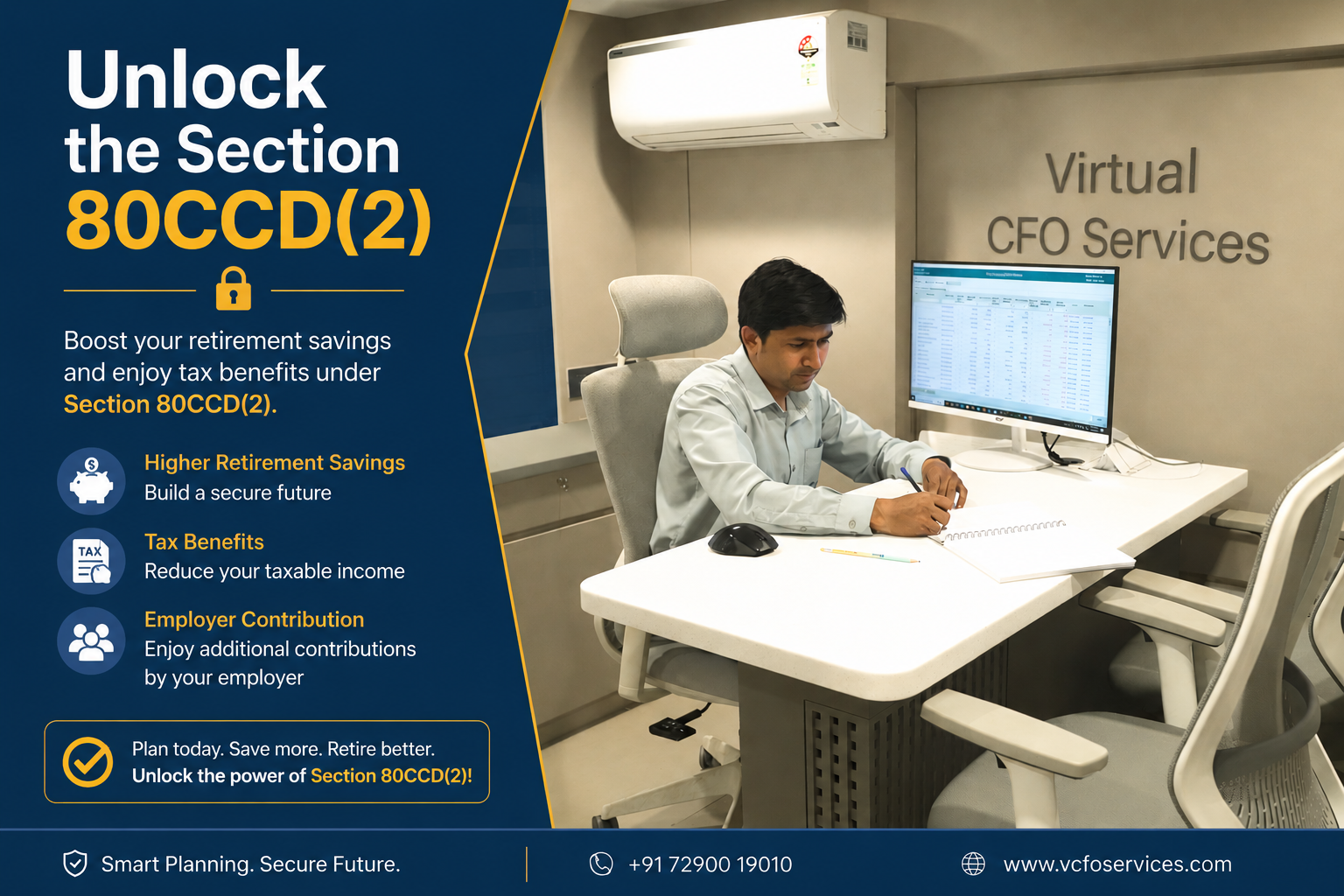

What Is the Section 80CCD(2) Deduction?

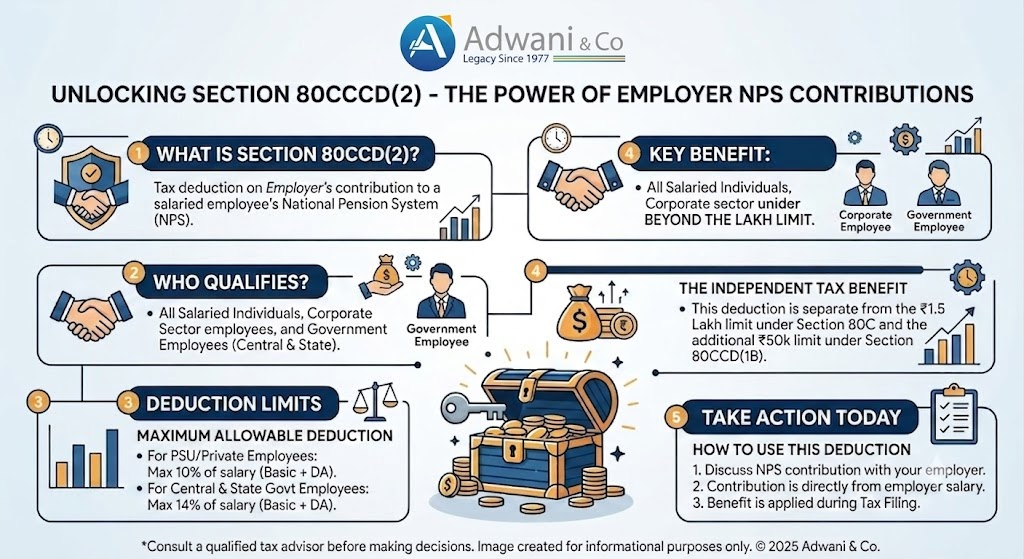

The Section 80CCD(2) deduction relates to the employer’s contribution to an employee’s National Pension System (NPS) account. Unlike most other retirement-linked deductions, it does not disappear if you opt for the New Tax Regime it is one of a small handful of provisions that survives the shift away from the Old Tax Regime’s exemption-heavy structure.

In simple terms, when your employer contributes a percentage of your salary to your NPS account, that contribution is treated as a deductible business expense for the company and, up to a prescribed limit, is not taxable in your hands either. The Section 80CCD(2) deduction is what defines that prescribed limit and it is precisely this limit that changed favourably under the New Tax Regime.

Section 80CCD(2) Deduction Limit: Old vs New Tax Regime Compared

The clearest way to understand the improvement is to compare the Section 80CCD(2) deduction limit across both tax regimes for different categories of employees.

Employee Category

Old Tax Regime

New Tax Regime

Government Employees

Up to 14% of Salary*

Up to 14% of Salary*

Private Sector / Other Employees

Up to 10% of Salary*

Up to 14% of Salary*

*Salary, for the purpose of this deduction, means Basic Salary plus Dearness Allowance, to the extent it forms part of retirement benefits.

Notice what happened here. Government employees always had access to a 14% Section 80CCD(2) deduction, under both regimes. Private sector employees, however, were historically capped at 10% under the Old Tax Regime. Under the New Tax Regime, that cap has been raised to 14% bringing private sector employees to full parity with government employees for the first time.

This makes the Section 80CCD(2) deduction one of the rare instances where choosing the New Tax Regime does not mean giving something up it means gaining a genuinely larger benefit, provided your employer’s compensation structure is designed to use it.

How the Section 80CCD(2) Deduction Works for Private Sector Employees

The Section 80CCD(2) deduction is not something you claim by writing a cheque yourself. It depends entirely on your employer’s payroll and compensation policy. A few operating rules are essential to understand:

The deduction applies only to the employer’s contribution to NPS voluntary or personal contributions you make yourself do not qualify under this section.

Whether your employer contributes to NPS at all, and at what percentage, is a matter of company policy, not a statutory entitlement you can demand individually.

The contribution must be routed through a recognised NPS account structure and reported correctly in payroll and Form 16.

Real Example: Calculating Your Section 80CCD(2) Deduction Benefit

Consider Priya, a private sector employee with a Basic Salary plus DA of ₹12,00,000 per year, who has opted for the New Tax Regime for FY 2026-27.

Under the Old Tax Regime, her employer could contribute a maximum of 10% of ₹12,00,000 = ₹1,20,000 towards NPS, and this entire amount would qualify for the Section 80CCD(2) deduction.

Under the New Tax Regime, her employer can now contribute up to 14% of ₹12,00,000 = ₹1,68,000 towards NPS, and this larger amount qualifies for the Section 80CCD(2) deduction.

That is an additional ₹48,000 of tax-free retirement contribution every year simply by aligning the compensation structure to the New Tax Regime’s enhanced limit.

Over a working career, that difference compounds significantly, both in terms of tax efficiency and retirement corpus growth. This is exactly the kind of practical, numbers-based planning that separates a well-structured salary from a generic one.

The ₹7.5 Lakh Aggregate Cap on Employer Retirement Contributions

The Section 80CCD(2) deduction does not operate in isolation. Under Section 17(2)(vii) of the Income Tax Act, the combined employer contribution to NPS, Recognised Provident Fund (RPF), and Approved Superannuation Fund is capped at an aggregate of ₹7.5 lakh per year. Any amount contributed beyond this combined threshold becomes taxable as a perquisite in the employee’s hands, along with any notional interest or growth attributable to the excess.

Key Takeaways

The Section 80CCD(2) deduction covers only the employer’s NPS contribution, not personal contributions.

Private sector employees can now claim up to 14% of salary under the New Tax Regime, up from 10% under the Old Tax Regime.

Government employees continue to enjoy a 14% deduction limit under both regimes.

Combined employer contributions to NPS, RPF, and superannuation fund are capped at ₹7.5 lakh annually under Section 17(2)(vii). This is one of the few deductions where the New Tax Regime is genuinely more generous than the Old Tax Regime.

Frequently Asked Questions

1. Is the Section 80CCD(2) deduction available under the New Tax Regime?

Yes. Unlike most Chapter VI-A deductions, the Section 80CCD(2) deduction for employer NPS contribution remains available under the New Tax Regime, at an even higher limit for private sector employees.

2. What is the current Section 80CCD(2) deduction limit for private sector employees?

Private sector employees can claim a Section 80CCD(2) deduction of up to 14% of salary (Basic + qualifying DA) under the New Tax Regime, compared to 10% under the Old Tax Regime.

3. Can I claim the Section 80CCD(2) deduction for my own NPS contributions?

No. The Section 80CCD(2) deduction applies only to the employer’s contribution. Personal NPS contributions are governed separately under Sections 80CCD(1) and 80CCD(1B).

4. Is there a cap on combined employer contributions to retirement funds?

Yes. Under Section 17(2)(vii), combined employer contributions to NPS, RPF, and Approved Superannuation Fund are capped at ₹7.5 lakh annually, with any excess taxed as a perquisite.

5. Do government employees benefit from the same Section 80CCD(2) deduction increase?

No change applies to them government employees already had access to a 14% deduction limit under both the Old and New Tax Regimes.

6. Should my employer revise our compensation policy for this deduction?

It is worth a professional review. Structuring part of compensation as an employer NPS contribution can materially improve tax efficiency for employees without added cost to the company.

The New Tax Regime is usually framed as a trade-off — simpler slabs in exchange for fewer deductions. The Section 80CCD(2) deduction tells a different story. For private sector employees, it is a genuine improvement, and it only delivers value when the employer’s compensation structure is built to capture it. As FY 2026-27 progresses, reviewing whether your salary structure is optimised for the Section 80CCD(2) deduction is one of the simplest, highest-value exercises a business can undertake.

If you want expert guidance on structuring your compensation policy around the Section 80CCD(2) deduction, or on any aspect of tax planning under the New Tax Regime, connect with Adwani & Co LLP today.

About the Author:

Mukesh Chavan is a dedicated indirect taxation and compliance professional associated with Adwani & Co LLP, specializing in GST advisory, GST audits, GST assessments, and RERA compliance services. With extensive experience in handling complex regulatory matters, he assists businesses in ensuring compliance with evolving GST laws and real estate regulations while minimizing risks and enhancing operational efficiency.

Mukesh has successfully guided clients through GST registrations, return compliance, departmental assessments, audits, litigation support, and tax planning strategies. He also possesses significant expertise in RERA compliance, helping real estate developers, promoters, and stakeholders navigate regulatory requirements and maintain seamless project compliance.

Through his articles and professional insights, Mukesh aims to simplify complex GST and RERA provisions, offering practical guidance that empowers businesses to remain compliant, avoid disputes, and make informed decisions in an increasingly dynamic regulatory environment. His approach combines technical expertise with practical business understanding, enabling clients to focus on growth while meeting their statutory obligations with confidence.

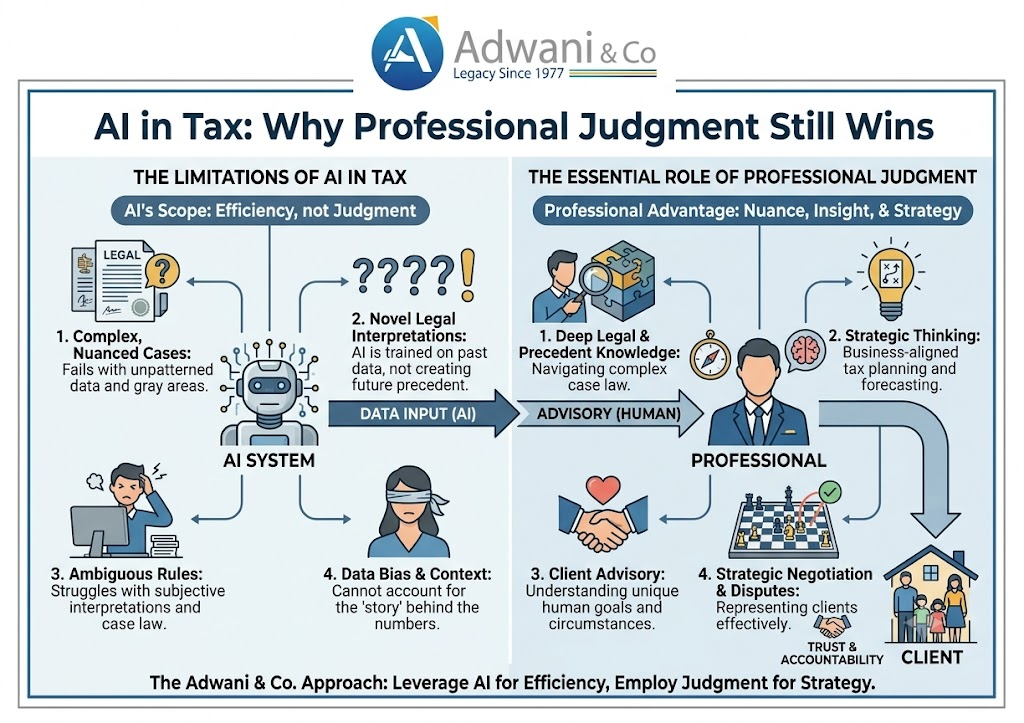

Everyone is asking whether AI can prepare tax returns. Almost nobody is asking the more important question: who will defend the tax position behind them?

That single question who defends the reasoning, not just the numbers is quietly reshaping the future of tax compliance across India and globally. And for businesses, founders, and professionals navigating the increasingly scrutinised landscape of income tax, GST compliance, and cross-border taxation in 2026, it is the question that matters most.

AI in tax return preparation is already impressive. It extracts data from documents, populates schedules, identifies missing information, and generates draft returns in minutes. The Income Tax Department’s own AIS (Annual Information Statement) system and the GST Portal now integrate AI-driven analytics to detect mismatches before a return even reaches a scrutiny desk. In that environment, a technically accurate return is just the starting point not the finish line.

The real risk in modern tax compliance is not a calculation error. It is a reasoning error. And reasoning errors are exactly where AI in tax professional judgment gaps show up most sharply.

AI in Tax Compliance: What It Does Well in 2026

To be fair to the technology, AI is genuinely transforming the mechanics of tax compliance. What previously took hours of manual data entry now happens in minutes. For routine income tax return filing, GST return preparation, and reconciliation tasks, AI-assisted tools have meaningfully improved speed and reduced data-entry errors.

The capabilities that AI brings to tax compliance include:

Extracting structured data from invoices, bank statements, Form 16, and TDS certificates

Pre-populating ITR forms based on AIS and Form 26AS data available on the Income Tax Department portal

Identifying gaps between GSTR-1 and GSTR-3B or flagging GSTR-2B mismatches before filing

Generating draft tax computations with standard deduction and exemption claims

Flagging potential income tax notice triggers based on patterns in prior filings

These are genuine productivity gains. A CA firm that uses AI tools intelligently can serve more clients, reduce routine errors, and spend less time on administrative work.

But productivity is not the same as judgment. And in taxation especially for businesses managing GST compliance 2026, handling cross-border transactions, or responding to income tax notices judgment is where the real risk lives.

Why AI in Tax Return Preparation Is Not Enough on Its Own

Consider a straightforward scenario.

A business files its ITR. The numbers are correct. Every document is available. The return passes all system validation checks. Yet three critical questions remain unanswered:

The Questions AI Cannot Answer for You

→ Is the taxpayer actually eligible for the benefit claimed?

→ Does a restriction or limitation provision apply under the Income Tax Act?

→ Is there a more advantageous tax position available that has not been explored?

→ What assumptions underlie the computation, and can they withstand scrutiny?

→ If the Income Tax Department issues a notice, can the position be professionally defended?

These are not edge cases. They represent the core of professional tax advisory and they are precisely where AI in tax professional judgment gaps become expensive.

The Income Tax Department and CBDT have significantly increased their use of data analytics and AI-driven scrutiny. Cross-referencing of ITR data with AIS, TDS data, MCA filings, GST turnover, and banking transactions is now routine. As per guidance available through the Income Tax Department portal, cases are increasingly selected for scrutiny based on risk-scoring models that evaluate the consistency and commercial logic of reported positions not just the arithmetic.

In that environment, a return that is numerically correct but logically indefensible is not a safe return. It is a delayed problem.

A Real-World Tax Risk Example: Where AI Missed and Judgment Mattered

Practical Example A proprietary trading firm with an annual turnover of ₹3.2 crore used an AI-assisted platform to prepare and file its ITR-3 for AY 2025-26. The AI correctly: • Computed speculative and non-speculative business income separately • Applied the correct tax rates • Populated all required schedules What the AI did not evaluate: • Whether certain derivatives transactions qualified as speculative or non-speculative under Section 43(5) of the Income Tax Act a distinction that affects set-off of losses • Whether the firm’s expenses claimed as business deductions met the ‘wholly and exclusively for business’ test • Whether turnover disclosed in the ITR was consistent with GST returns and bank statements, given the firm also had an NBFC registration Result: An income tax notice was issued under Section 143(2) querying the loss set-off and expense claims. A CA reviewing the return before filing would have identified these risk points and either restructured the position or documented the reasoning making the notice either avoidable or significantly easier to defend.

This is not a rare situation. It is representative of exactly the kind of reasoning error that automated tax preparation cannot prevent because preventing it requires judgment about facts, law, and professional risk, not just calculation.

AI vs. Professional Judgment in Tax: A Practical Comparison

What AI Handles Well in Tax Compliance

Where Professional Judgment in Tax Is Required

Extracting data from Form 16, TDS certificates, AIS

Evaluating whether all income sources are correctly characterised

Populating ITR schedules based on available data

Deciding which ITR form is appropriate given the taxpayer’s income profile

Identifying GSTR-1 vs GSTR-3B mismatches

Determining the legal significance of the mismatch and how to resolve it

Flagging excess ITC claims against GSTR-2B

Advising whether to reverse ITC, dispute the claim, or pursue vendor rectification

Generating draft tax computations

Reviewing whether deductions, exemptions, and set-offs are correctly applied

Detecting variance from prior-year filings

Explaining the variance and assessing whether it creates scrutiny risk

Preparing income tax notice response templates

Drafting a legally sound reply that addresses the actual notice ground

Professional Judgment in Tax: What It Actually Means

The phrase is used frequently in professional circles, but it has a concrete meaning in the context of AI in tax compliance.

Interpreting Provisions:Not Just Applying Them

The Income Tax Act, 1961, and the GST law contain thousands of provisions. Many are straightforward. Some are ambiguous, subject to judicial interpretation, or apply differently depending on facts. An AI system applies the provision as trained. A professional interprets it in context.

Dr. Haresh Adwani, a PhD holder in Commerce and a law graduate, regularly applies this dual lens at Adwani and Company evaluating tax positions not only through a finance lens but through the legal framework that governs their validity.

Evaluating Whether Assumptions Are Commercially Defensible

Every tax return carries assumptions about the nature of transactions, the classification of income, the eligibility for benefits. AI generates those assumptions from patterns. A professional evaluates whether they hold up to scrutiny in a specific business context.

Managing Risk Across the Compliance Lifecycle

Tax risk does not end at filing. It extends to assessments, scrutiny, notices, and appeals. Professional judgment in tax includes structuring positions that can be defended through the full lifecycle of compliance not just at the point of return preparation.

As AI-driven scrutiny by the Income Tax Department and GST authorities becomes more sophisticated, the cost of an indefensible position rises. This is the core dynamic reshaping what tax professionals are paid to do.

AI in Tax and the Income Tax Notice Risk

One of the most practical implications of AI in tax compliance for businesses and individuals is the income tax notice risk.

Under Section 143(2), Section 148, and other scrutiny provisions, the Income Tax Department can issue notices based on risk-scoring that increasingly relies on cross-database analytics. The parameters include:

Significant variation between ITR-reported income and AIS data

Mismatch between GST turnover and income tax turnover

High-value transactions without corresponding income disclosure

Unusual deduction or exemption claims relative to prior years

Discrepancies between MCA-reported financials and tax filings

An AI-prepared return can tick all the validation checkboxes and still contain the exact kind of inconsistency that triggers one of these notices—because the inconsistency is in the reasoning, not the arithmetic.

This is where Adwani and Company‘s approach to tax advisory adds measurable value. The firm’s review process, guided by Dr. Haresh Adwani‘s academic grounding in Commerce and legal knowledge, evaluates both the technical accuracy and the commercial defensibility of every significant tax position before filing.

Everything said about income tax applies equally and in some ways more acutely to GST compliance in 2026.

AI tools can prepare GSTR-3B, match GSTR-2B for input tax credit reconciliation, and flag vendor-level discrepancies. But the judgment questions in GST compliance are substantial:

Is a particular supply correctly classified, and has the right GST rate been applied?

Does a transaction qualify for input tax credit eligibility, or does a restriction under Section 17(5) apply?

Is an export zero-rated correctly, or does a condition remain unsatisfied?

When a GST notice arrives questioning ITC claims, is the response legally adequate?

According to compliance advisories and updates available on the GST Portal (gst.gov.in) and cross-referenced with MCA (mca.gov.in) data, authorities are increasingly scrutinising the commercial rationale of transactions—not just their documentation.

A business with ₹80 lakh in ITC claims but a vendor base that shows irregular GSTR-1 filing is not just a documentation risk. It is a legal risk that requires professional assessment and, where necessary, a structured response strategy.

The Most Valuable Tax Skills in an AI-Enabled World

The LinkedIn post that inspired this article asked a pointed question: what will be the most valuable skill in an AI-enabled tax world?

Based on work across diverse client engagements at Adwani and Company, here is a grounded answer:

High-Value Tax Skills for the AI Era 1. Analytical Review of AI Outputs ability to critically evaluate AI-generated computations, identify reasoning gaps, and flag positions that look correct but carry hidden risk 2. Regulatory Interpretation applying the Income Tax Act, GST law, FEMA, and related frameworks to specific facts in a way that produces a defensible position 3. Risk Communication translating technical tax risk into commercially actionable language for founders, CFOs, and business owners 4. Notice and Litigation Management structuring responses to income tax notices, GST scrutiny, and assessment proceedings with legal and factual rigour 5. Cross-Border Tax Judgment advising on NRI taxation, transfer pricing, DTAA benefits, and FEMA compliance in situations where AI outputs are least reliable

These are not replaceable skills. They are enhanced by AI but their value lies precisely in the human judgment that AI cannot replicate.

Key Takeaways

Summary • AI in tax return preparation handles the mechanical and computational layer well data extraction, schedule population, reconciliation flagging. • The gap between an AI-prepared return and a professionally reviewed one lies in reasoning: assumptions, eligibility, risk assessment, and defensibility. • As the Income Tax Department and GST authorities increase AI-driven scrutiny, the cost of indefensible tax positions is rising. • Professional judgment in tax covers interpretation, commercial context, risk management, and accountability across the full compliance lifecycle. • The future of tax practice is not AI replacing professionals it is AI handling scale while professionals provide the judgment that determines outcome. • For any significant tax position, cross-border transaction, notice response, or restructuring, professional review is not a legacy stepit is the critical step.

Frequently Asked Questions:

1. Can AI tools file income tax returns accurately without a CA reviewing them?

For straightforward salary-based returns with limited income sources, AI tools perform adequately. For business income, capital gains, multiple income sources, or any position that carries interpretation risk—such as deduction eligibility or income characterisation—professional review before filing is strongly recommended. An accurate calculation is not the same as a defensible position.

2. What is the biggest risk in AI-generated tax computations?

The biggest risk is not arithmetic—it is assumption. AI systems apply rules as trained, without evaluating whether those rules apply to the specific facts of a taxpayer’s situation. Where eligibility conditions, limitations, or judgment-based classifications are involved, the AI output may be technically formatted but commercially or legally incorrect.

3. How does the Income Tax Department use AI to scrutinise returns?

The Income Tax Department and CBDT increasingly use risk-scoring systems that cross-reference ITR data with AIS, TDS records, GST turnover, MCA filings, and banking data. Returns are selected for scrutiny based on inconsistency and risk indicators—not just arithmetic errors. A return that is numerically correct but logically inconsistent across data sources can still attract a Section 143(2) notice.

4. What should a business do when it receives an income tax notice?

First, read the notice carefully to identify the specific ground being raised—whether it concerns turnover mismatch, deduction claims, or unreported income. Second, do not respond without professional guidance; an incomplete or poorly structured reply can escalate the matter. Third, engage a qualified CA firm to assess the position and draft a legally adequate response. Adwani and Company provides structured income tax notice reply support across all major notice types.

5. Is professional judgment still needed for GST compliance if I use accounting software?

Yes. Accounting software and AI tools improve GST return preparation speed and reduce data entry errors. They do not evaluate whether your ITC claims are legally valid, whether your GST rate classifications are correct, or whether a vendor-mismatch creates a legal exposure requiring action. GST compliance in 2026 requires both good systems and professional advisory—especially for businesses with complex transactions or ITC-heavy operations.

6. What makes Adwani and Company different from a standard CA firm for tax advisory?

Adwani and Company brings a multi-disciplinary approach to tax advisory. Dr. Haresh Adwani combines a PhD in Commerce with a law degree, allowing the firm to evaluate tax positions through both a financial accounting lens and a legal framework. This is particularly valuable in situations where the tax question involves statutory interpretation, litigation risk, or cross-jurisdictional complexity.

7. How can small businesses use AI in tax without taking on excessive risk?

Small businesses can use AI tools for routine compliance tasks—return preparation, reconciliation, and data organisation—while ensuring that any significant position (deduction claims, ITC eligibility, income characterisation) is reviewed by a qualified professional before filing. Treating AI output as a first draft subject to professional review is the practical approach that balances efficiency with risk management.

Conclusion: Professional Judgment in Tax Is the New Competitive Advantage

AI is not a threat to the tax profession. It is a clarification of what the tax profession is actually for.

When AI handles the mechanical layer data extraction, schedule population, reconciliation flagging what remains is the professional judgment layer: interpretation, risk evaluation, position defence, and client advisory. That layer has always been where the real value sits. AI just makes it more visible.

The future tax professional, as the LinkedIn post that inspired this article noted, will spend less time preparing returns and more time validating assumptions, challenging conclusions, and managing risk. In the context of India’s increasingly analytics-driven tax administration where the Income Tax Department, CBDT, and GST authorities cross-reference multiple data sources in real time that shift is not optional. It is already underway.

For businesses and individuals who want to stay ahead of that curve, the right question is not ‘can AI prepare my return?’ It is ‘who is reviewing the reasoning behind it?’

Connect With Adwani and Company If you want expert guidance on income tax compliance, GST advisory, tax notice responses, or cross-border taxation, connect with Adwani and Company today. Dr. Haresh Adwani and the team bring the combination of deep tax expertise and legal knowledge that complex tax positions require whether you are a founder filing business income, a company managing GST scrutiny, or an NRI with cross-border tax obligations. → Learn more about our Income Tax Advisory Services → Explore our GST Compliance and Notice Reply Support → Read about our Virtual CFO and Financial Reporting Services Website: adwaniandco.com

CA Dipesh Gurubakshani is a Chartered Accountant with Adwani & Co LLP, Pune, specialising in income tax audit, direct taxation, and accounting advisory. He supports clients across statutory compliance, financial reporting, and income tax matters with a focus on accuracy, regulatory adherence, and disciplined ex

One document arrives in your inbox. Thousands of tax filing mistakes follow.

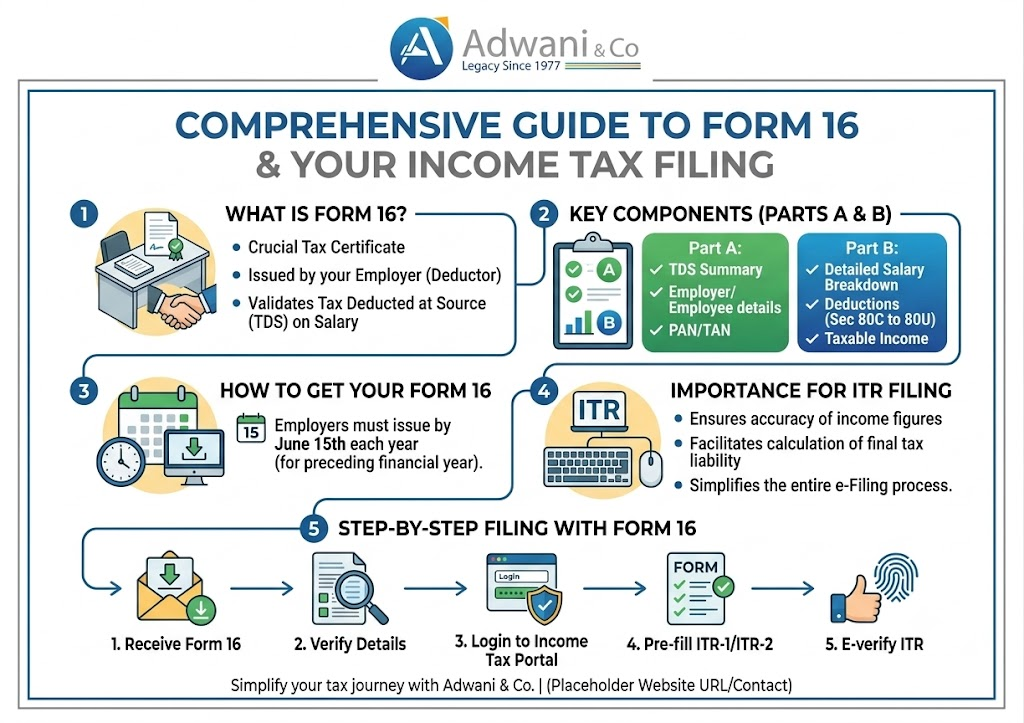

That document is Form 16. Every salaried employee in India receives it from their employer once the financial year ends and almost every year, lakhs of taxpayers make the same critical error: they treat Form 16 as the complete picture, file their Income Tax Return (ITR) based on it alone, and unknowingly leave out income that the Income Tax Department already knows about.

The result? Tax notices, demand letters, and avoidable penalties.

According to the Income Tax Department of India, every taxpayer is individually responsible for disclosing all sources of income even those not reflected in their salary certificate. Form 16 for income tax filing is a powerful starting point, but it is only the beginning.

In this guide, tax experts at Adwani and Companyled by Dr. Haresh Adwani, PhD in Commerce and a law graduate with extensive legal knowledge break down everything you need to know about Form 16, what it covers, what it misses, and how to use it correctly for a clean, accurate ITR filing in AY 2026-27.

What Is Form 16 for income tax filing and Why Does It Matter for Income Tax Filing?

Form 16 is a TDS Certificate issued by your employer under Section 203 of the Income Tax Act, 1961. It serves as a formal record of:

Your total salary paid during the financial year

Tax Deducted at Source (TDS) on your salary by the employer

Deductions claimed under Chapter VI-A (80C, 80D, HRA, etc.)

Tax deposited with the Central Government on your behalf

The document is divided into two critical parts that every taxpayer must understand before proceeding with Form 16 income tax return filing:

Form 16 Part A

Form 16 Part B

Employer details, PAN, TAN

Detailed salary breakup

TDS amount deposited with government

Allowances: HRA, LTA, Special

Quarter-wise TDS deposition summary

Exemptions claimed under Section 10

Generated via TRACES portal (CBDT)

Deductions under Chapter VI-A (80C, 80D, etc.)

Mandatory for all salaried employees

Taxable income computation

The Most Dangerous Misconception About Form 16 for Income Tax Filing

Here is the single most dangerous assumption salaried professionals make every year:

“My employer gave me Form 16. My taxes are sorted. I just upload it and I’m done.”

This assumption is incorrect and it costs taxpayers money, time, and stress every filing season.

Form 16 only captures income your employer paid you and the TDS they deducted on it. It does not cover income you earned independently throughout the year. The Income Tax Department receives data from multiple sources banks, mutual fund registrars, stockbrokers, SEBI-registered entities through the Annual Information Statement (AIS) and Form 26AS. If you omit income that already appears in the AIS, a mismatch notice under Section 143(1) becomes almost inevitable.

As Dr. Haresh Adwani of Adwani and Company explains: “Every year we see clients who receive notices for income they forgot to declare not because they were dishonest, but because they simply assumed Form 16 covered everything. It does not. A complete ITR demands a complete disclosure of all income.”

Income Sources Not Covered in Form 16 for Income Tax Filing

The following income categories are commonly missed by salaried taxpayers who rely solely on Form 16 for income tax filing. You must disclose all of these separately in your ITR:

1. Interest Income from Savings Accounts and Fixed Deposits

Banks and post offices report interest paid to the Income Tax Department. Interest income from savings accounts beyond ₹10,000 per year is taxable (Section 80TTA provides a deduction up to ₹10,000 for savings interest). Fixed deposit interest is fully taxable at your slab rate. Many taxpayers forget to add FD interest and banks already report it to the AIS.

Practical Example: Mr. Suresh earns ₹12 lakh salary. His Form 16 shows ₹1,08,000 TDS. But he also has ₹85,000 interest from three FDs across two banks. He files ITR without adding FD interest. The AIS shows the FD interest. He receives a Section 143(1) demand of ₹26,350 plus interest under Sections 234A/B. A simple ₹85,000 omission costs him over ₹26,000 in taxes and penalties.

2. Capital Gains from Shares and Mutual Funds

If you sold equity shares, equity mutual funds, debt funds, or debt mutual funds during FY 2025-26, the capital gains must be reported. This is among the most frequently missed disclosures:

#

Asset Type

Tax Treatment

1

Equity shares / Equity MFs held > 12 months

LTCG taxable above ₹1.25 lakh at 12.5% (post-Budget 2024)

2

Equity shares / Equity MFs held < 12 months

STCG at 20%

3

Debt mutual funds (all holding periods)

Taxable at slab rate as per FY 2023-24 amendment

4

Unlisted shares held > 24 months

LTCG at 12.5% without indexation

5

Unlisted shares held < 24 months

Taxable at slab rate

The Central Board of Direct Taxes (CBDT) receives transaction data from depositories (CDSL, NSDL) and registrar and transfer agents (CAMS, KFintech). Your gains are visible to the department even if your employer is unaware.

3. Rental Income from Property

If you own and rent out residential or commercial property, the rental income — after deducting a standard 30% on net annual value and home loan interest — must be declared under Income from House Property. Form 16 does not touch this income. Many salaried employees who rent out a second property forget this entirely.

4. Income from Previous Employers

If you changed jobs during FY 2025-26, you will receive multiple Form 16s — one from each employer. Both salaries must be totalled and reported. A common mistake: employees let the new employer compute TDS based only on current employer income, leading to shortfall in tax payment and a demand notice at the time of ITR processing.

5. Freelance, Consultancy, or Business Income

Any income earned through freelancing, content creation, part-time consulting, or online platforms (Upwork, Fiverr, YouTube monetization, Instagram collaborations) is taxable as Income from Business or Profession or Income from Other Sources, depending on regularity and scale. Salaried professionals who moonlight often forget that this income sits outside their Form 16 entirely.

6. Gifts and Other Income

Gifts received from non-relatives exceeding ₹50,000 in a financial year are taxable under Section 56(2)(x). Lottery winnings, game show prizes, and online gaming winnings now face a flat 30% TDS under Section 194BA. All must be declared.

How to Cross-Check Form 16 Against AIS and Form 26AS Before Filing

Before you submit your Form 16 income tax return filing, always cross-check your Form 16 against two government documents:

Annual Information Statement (AIS): Available on the Income Tax e-filing portal. Shows all income reported to the department across 50+ transaction categories.

Form 26AS: The traditional TDS/TCS credit statement. Cross-check that all TDS deducted by your employer matches Form 26AS discrepancies can cause credit denial.

If you find income in the AIS that is not in your Form 16 interest, dividends, mutual fund redemptions, property purchases include all of it in your ITR. Deliberately omitting AIS-reflected income attracts penalties under Section 270A, which can be up to 200% of the tax evaded in cases of under-reporting.

The team at Adwani and Company routinely reconciles AIS data with Form 16 for clients before filing a step that prevents the majority of notices they would otherwise receive.

Choosing the Right ITR Form When Filing With Form 16

Not everyone with a Form 16 should file ITR-1. The form you use depends on your total income profile, not just your salary:

Sr. No.

ITR Form

Who Should Use It

1

ITR-1 (Sahaj)

Salary + one house property + other sources (interest). Total income up to ₹50 lakh. No capital gains.

2

ITR-2

Salary + capital gains + more than one property + foreign assets or income. Total income any amount.

3

ITR-3

Salary + business/profession income (freelancers, consultants with regular clients).

4

ITR-4 (Sugam)

Presumptive income (Section 44ADA for professionals). Total income up to ₹50 lakh.

Filing the wrong ITR form such as using ITR-1 when you have capital gains is treated as a defective return under Section 139(9). The department will issue a notice asking you to re-file in the correct form, which adds unnecessary compliance burden. Dr. Haresh Adwani, with his background in commerce and law, emphasises that correct form selection is as important as accurate income disclosure.

Old vs New Tax Regime: What Form 16 Tells You and What It Does Not

Your employer deducts TDS based on the tax regime you chose at the start of the financial year. Form 16 will reflect deductions accordingly. However, at the time of filing, you can switch your regime subject to conditions:

Old Tax Regime

New Tax Regime (Default from FY 2023-24)

Allows deductions: 80C, 80D, HRA, LTA, home loan interest

No most deductions (except NPS, standard deduction)

Better for those with high investments + home loans

Better for those with fewer deductions

Must be opted in at time of filing for non-business income

Default regime; applies unless you opt out

Higher tax rates at lower slabs

Lower slab rates across all income levels

If your employer deducted TDS under the new regime but you have significant 80C/80D investments and home loan interest, switching to the old regime at the time of filing may result in a tax refund. Adwani and Company helps clients run a quick regime comparison before filing to ensure they do not overpay by defaulting to the employer-chosen regime.

Key Takeaways: Form 16 and Income Tax Filing Checklist

Before You File: Complete Form 16 Tax Filing Checklist Download Form 16 Part A and Part B from your employerLog in to incometax.gov.in and download your AIS and Form 26ASList ALL income sources: salary, FD interest, capital gains, rent, freelance, giftsCollect Form 16A / Broker statements / Mutual fund redemption statementsIf you changed jobs, collect Form 16 from all employersRun a regime comparison (old vs new) to optimise tax outflowSelect the correct ITR form based on your complete income profileFile before July 31, 2026 to avoid Section 234F late filing fee (₹1,000–₹5,000)

Frequently Asked Questions

Q1. Can I file my income tax return using only Form 16?

Technically, Form 16 provides the data you need to file ITR-1 if your only income is salary from one employer with no capital gains. However, if you have any other income — interest, dividends, capital gains, rental income, freelance — you must collect and add those details separately. Relying solely on Form 16 without verifying the AIS is the most common cause of mismatch notices.

Q2. What is the difference between Form 16 Part A and Part B?

Form 16 Part A is generated by the employer through the TRACES portal and contains TDS amounts deposited with the government, quarter-wise. Form 16 Part B is prepared by the employer and contains the detailed salary breakup, exemptions claimed, and deductions allowed. Both parts are required for a complete and accurate ITR filing.

Q3. I changed jobs mid-year. How do I handle Form 16 from two employers?

You will receive two Form 16s — one from your old employer and one from your new employer. Add both salary figures and file ITR-2 or ITR-1 as applicable. Importantly, declare the income from your previous employer to your current employer at the start of your new job so that TDS is calculated on the combined income. Failing to do this leads to a tax shortfall and a demand at ITR processing time.

Q6. What happens if my AIS shows income that I do not recognise?

Log in to incometax.gov.in and raise a feedback on the AIS to mark the transaction as incorrect or not relating to you. However, do not ignore it. Filing an ITR that contradicts unresolved AIS entries can trigger a scrutiny assessment. Consult a CA to evaluate the right course of action.

Q7. What is the penalty for filing ITR late after receiving Form 16?

Under Section 234F, a late filing fee of ₹1,000 applies if total income is up to ₹5 lakh, and ₹5,000 if total income exceeds ₹5 lakh. Additionally, interest under Sections 234A, 234B, and 234C applies on any outstanding tax liability. The due date for most salaried taxpayers for AY 2026-27 is July 31, 2026.

Conclusion:

Every July, millions of Indian salaried employees file their income tax returns with the best of intentions and many still receive demand notices months later. Not because they were dishonest, but because they stopped at Form 16 when the filing process required them to go further.

Form 16 for income tax filing is the foundation the salary certificate that tells you what your employer paid you and what TDS was deducted. But the Income Tax Department sees far more: your FD interest, your mutual fund gains, your stock trades, your rental income. The AIS aggregates it all. Your ITR must match.

A thorough, compliant ITR is not complicated it requires organisation, awareness, and ideally, professional guidance. At Adwani and Company, Dr. Haresh Adwani and the CA team have guided hundreds of salaried professionals through exactly this process: ensuring that their Form 16 data, their AIS income, their investments, and their gains are all correctly disclosed in a clean, penalty-free return.

Tax season does not have to be stressful. With the right advisor, your Form 16 income tax return filing becomes straightforward and accurate filed once, filed correctly, filed with confidence.

Founder and Senior Partner, Adwani and Company. Over 40 years of expertise in income tax, corporate law, GST, and financial advisory.

Legal Disclaimer:This article is published for informational and educational purposes only. Nothing contained herein constitutes legal, financial, or tax advice, nor should it be treated as a substitute for professional consultation tailored to your specific circumstances. Tax laws, rates, and provisions are subject to change; readers are strongly advised to consult a qualified Chartered Accountant or tax advisor before acting on any information in this article.

All content is original. References to government portals and statutory provisions are paraphrased for educational purposes in compliance with fair use principles. No content hasbeen reproduced from third-party sources

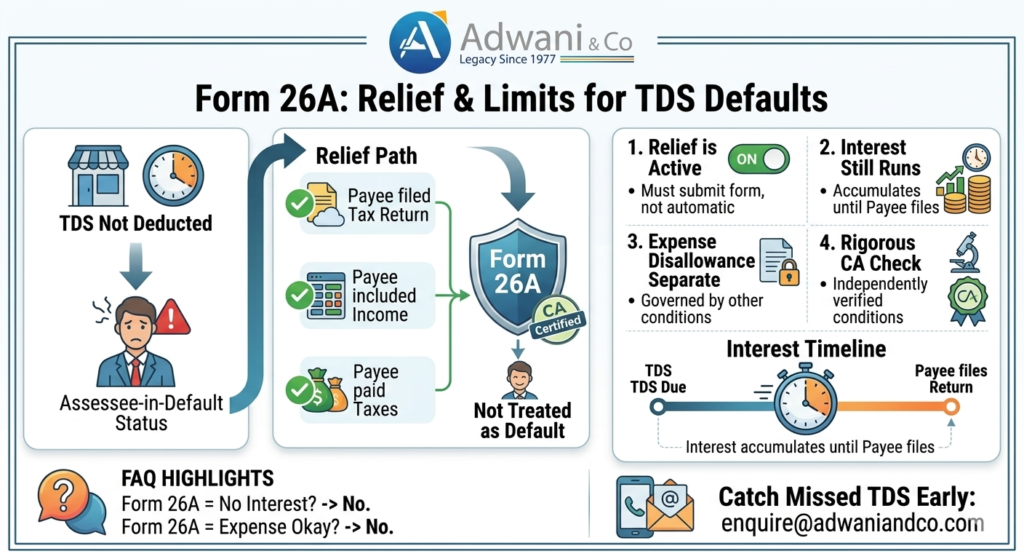

A client called me last year with a familiar problem. His business had made professional payments across two financial years without deducting TDS. Nobody had caught it at the time. The issue only surfaced during his tax audit and by then, interest had already been building for months.

His first question was simple: “Can Form 26A fix this?”

The honest answer is: partly. Form 26A is a genuine and meaningful relief mechanism. But it does not resolve everything, and businesses that assume it does often find themselves with an unexpected interest burden.

Form 26A helps a payer avoid being treated as an assesse in default under Section 201 if the payee has filed their return, included the income, and paid taxes. However, it does not eliminate interest under Section 201(1A) or guarantee expense allowability under Section 40(a)(ia).

Here is what Form 26A actually does and where it stops.

What Is Form 26A and What Does It Do in a TDS Default Situation?

When a payer fails to deduct TDS on a payment, the Income Tax Department typically treats that payer as an assessee-in-default under Section 201(1). This is not a minor label. It carries real consequences: disallowance of the expense under Section 40(a)(ia), interest liability under Section 201(1A), and a formal default on your record.

The proviso to Section 201(1) offers a conditional path out. A payer will not be treated as an assessee-in-default despite failing to deduct TDS if all three of the following conditions are met on the payee’s side:

The payee (a resident) has filed their return of income under Section 139.

The payee has included this specific income in that return.

The payee has paid the tax due on this income.

If all three are satisfied, a Chartered Accountant certifies these facts in Form 26A. Once submitted, the payer escapes the assessee-in-default classification under Section 201(1).

That is meaningful relief. But many businesses stop reading here and that is precisely where the problem starts.

In a typical Form 26A TDS default case, understanding these limitations is critical to avoid further tax exposure.

Understanding the limits of Form 26A is just as important as knowing what it provides. Here are the four key boundaries businesses and their advisors must be aware of.

Limit 1 Relief Is Not Automatic

Form 26A must be formally obtained and submitted. Simply knowing you may be eligible does not protect you. The default remains on record until the form is actually furnished through the proper procedure. Acting on it early matters.

Limit 2 Interest Under Section 201(1A) Still Applies

New subsection to be inserted within the existing “Interest Liability Under Section 201(1A)” section.

What the Interest Actually Costs

Understanding that interest applies is one thing. Knowing the rate is what makes the risk real.

Section 201(1A) prescribes two distinct rates depending on the nature of the default:

Failure to deduct TDS at all: Interest at 1% per month (or part of a month) on the amount of tax that should have been deducted, running from the date TDS was required to be deducted to the date the payee files their return of income.

TDS deducted but not remitted to the government: Interest at 1.5% per month (or part of a month) on the amount deducted, running from the date of deduction to the date of actual payment.

Both rates may appear modest in isolation, but they compound against time and against the full tax amount not just the delayed portion. In a case where TDS was required in, say, April of a financial year and the payee only files their return fourteen months later in June of the following year, the interest calculation covers that entire period. At 1% per month, that is already a 14% charge on the TDS amount, before any penalties are considered.

The interest under Section 201(1A) is treated by law as a compensatory charge not a penalty for the period during which the government was denied timely access to the tax. This characterisation was affirmed by the Supreme Court in Hindustan Coca-Cola Beverages Pvt. Ltd. v. CIT (2007) 293 ITR 226 (SC), where the Court made clear that even where the payee has paid the underlying tax and the payer is not treated as an assessee-in-default, the compensatory interest still runs its course. It does not disappear simply because the substantive default has been regularised through Form 26A.

For businesses reviewing their books after a TDS audit finding, this calculation is usually the first number their CA should work out because it tells you exactly what is at stake before you even begin the Form 26A process.

Limit 3 Disallowance Under Section 40(a)(ia) Is a Separate Question

Form 26A only addresses Section 201(1). Whether your expense is actually allowed as a deduction is governed by Section 40(a)(ia), which has its own conditions and its own logic.

Here is how Section 40(a)(ia) operates. When a payer fails to deduct TDS on payments such as professional fees, contract payments, rent, commission, interest, or royalties made to a resident, the law restricts the deduction of that expense in the year of default. The current restriction reduced from 100% to 30% by the Finance Act 2014, effective from Assessment Year 2015-16 means that 30% of the gross payment can be disallowed and added back to taxable income. For a business making substantial payments without TDS, this can translate into a meaningful increase in tax liability, not just a compliance note.

The critical link between Form 26A and Section 40(a)(ia) lies in the second proviso to that section, read with the first proviso to Section 201(1). If Form 26A conditions are satisfied payee has filed a return, included the income, and paid taxes then the payer is deemed to have deducted and paid the TDS on the date the payee filed their return of income. As a result, the disallowance under Section 40(a)(ia) does not apply for that year.

But this only works if Form 26A is filed. If the form is not furnished even where the payee has genuinely paid taxes the payer cannot claim this relief automatically. The deemed-payment fiction under the second proviso is triggered only by the act of furnishing the form through the prescribed process.

Two situations where the expense remains at risk despite a payee having paid taxes:

Form 26A is not filed before the assessment is concluded. Courts and the CBDT have consistently taken the position that Form 26A must be furnished before the assessment proceedings are finalised. Filing it after an assessment order is passed may not provide retrospective protection.

The payee is a non-resident. Section 40(a)(ia) covers payments to residents. For payments to non-residents, the relevant provision is Section 40(a)(i), and neither Form 26A nor the proviso to Section 201(1) applies in the same way. (This is addressed separately below under the non-resident limitation.)

The practical takeaway: Form 26A and expense allowability under Section 40(a)(ia) are related but distinct outcomes. Getting the form in place, accurately and on time, is what connects the payee’s compliance to the payer’s tax relief. Without it, the payee having paid taxes is a fact but one that the payer cannot use in their own assessment.

Limit 4 The CA Certification Must Be Rigorous

The Chartered Accountant issuing Form 26A must independently verify all three payee conditions: that the return was filed, that this income was included, and that tax was paid. If this verification is done carelessly or without proper documentary checks, the certification itself can be challenged creating fresh risk rather than resolving the existing one.

Limit 5 Form 26A Does Not Apply to Non-Resident Payees

The proviso to Section 201(1) which enables Form 26A relief applies only where the payee is a resident of India. The statute is explicit on this point. If a business makes a payment to a non-resident whether a foreign company, NRI, or overseas service provider without deducting TDS under the applicable section (most commonly Section 195), Form 26A cannot be used to seek relief.

For non resident payments, the TDS obligation has a different character altogether. The government’s collection mechanism for non-resident income depends substantially on withholding at source because once funds leave India, enforcement becomes significantly more complex. Courts have reinforced this view. In matters involving payments to non-residents without deduction under Section 195, tribunals have consistently declined to extend the Form 26A protection, even where the non-resident has filed a return and paid taxes in India.

Businesses operating in cross-border vendor relationships, making royalty or technical service payments overseas, or buying immovable property from NRIs need to be aware that this relief simply does not extend to their situation. The exposure under Section 201(1) in a non-resident default remains unresolved by Form 26A, and the path to remediation if one exists lies in different provisions, including DTAA applicability, lower deduction certificates under Section 197, or representations to the Assessing Officer under Section 195(2) and (3).

If your business makes both resident and non-resident payments, a compliance review should treat these as two distinct categories with different risk profiles and different available remedies.

Form 26A and TDS Default: Relief Under Section 201

Interest Liability Under Section 201(1A) in TDS Default Cases

Many businesses assume that once Form 26A is obtained, the TDS default is fully resolved. That assumption is incorrect, and the consequences of getting this wrong can be significant.

Interest under Section 201(1A) is not a penalty. It is treated by law as a compensatory charge for the period during which the government was deprived of timely tax collection. The interest runs from the date on which TDS was required to be deducted to the date on which the payee actually files their return of income. This is the case even if the payee has correctly disclosed the income and paid all taxes.

In practice, there is almost always a time gap. A payment may be made during the financial year, but the payee’s return is typically filed months later sometimes beyond the due date. During this entire period, interest accrues without interruption.

The real problem arises because TDS defaults are rarely identified immediately. In most cases including my client’s situation the issue surfaces during a statutory audit, tax audit, or income tax scrutiny. By that point, a substantial period has already passed. What started as a minor compliance lapse has become meaningful financial exposure, purely because of time.

The practical advice here is straightforward: act early. If you suspect a TDS default may exist in your books, get a structured compliance review done before it surfaces in a scrutiny notice. The earlier the detection, the lower the interest exposure.

Judicial and CBDT Context: Why the Law Landed Here:

The Form 26A mechanism did not emerge from a vacuum. It was the legislature’s codification of a principle that courts had already been applying — that once the government has received its tax from the payee, the payer should not be subjected to double jeopardy merely for the failure to withhold it.

The Supreme Court in Hindustan Coca-Cola Beverages Pvt. Ltd. v. CIT (2007) 293 ITR 226 (SC) laid the conceptual groundwork. The Court held that if the payee has paid tax on the income received, treating the payer as an assessee-in-default for failure to deduct results in the government recovering the same tax twice. CBDT Circular No. 275/201/95-IT(B) dated 29th January 1997 had already taken a similar position administratively. The Finance Act 2012 formalised this logic by inserting the first proviso to Section 201(1) and, through Notification No. 37/2012, prescribing Rule 31ACB and Form 26A.

What the Supreme Court also made clear — and what CBDT Circular No. 11/2017 subsequently addressed — is that interest under Section 201(1A) occupies a different space. The Court characterised it as compensatory rather than penal: it is the price the payer pays for having denied the government access to the withheld amount during the intervening period. This distinction matters because it means the interest survives even the most complete Form 26A filing. Courts do not treat the two — assessee-in-default status and interest liability — as a single outcome that Form 26A resolves together.

CBDT Circular No. 11/2017 also introduced a narrow relief for interest waiver in specific cases of TDS default under Section 201(1A)(i) for example, where a deductor acted on a jurisdictional High Court order that was subsequently reversed, or in cases involving non-residents where the DTAA was misapplied in good faith. These waivers require an application to the concerned CCIT or DGIT and are granted in exceptional circumstances, not as a matter of routine. Businesses in genuinely ambiguous positions may want to explore whether their facts qualify under these guidelines —but should not assume the waiver as a given.

The overall judicial trajectory is consistent: courts protect bona fide payers from double taxation but do not relieve them of the time-value cost of delayed withholding. Form 26A gives you the former. It cannot give you the latter.

How Form 26A Is Filed: The TRACES Process in Practice

The blog so far has focused on what Form 26A does and where it stops. But a business that has identified a TDS default and wants to act on it has one immediate practical question: how does this actually get done?

Form 26A is filed electronically through the TRACES portal (tdscpc.gov.in), the government’s TDS reconciliation and correction platform. The process is dual-step, involving both the deductor and the Chartered Accountant separately.

Step 1 : The Deductor Initiates the Request

The deductor logs into TRACES and raises a request for Form 26A based on the PAN of the payee for whom relief is being sought. The system auto-populates transactions from the deductor’s filed TDS returns where non-deduction or short-deduction is reflected. The deductor identifies the specific transactions, generates the annexure in the prescribed format, and submits it digitally either using a Digital Signature Certificate (DSC) or through Electronic Verification Code (EVC). The form then moves to a status of “Sent to E-Filing.”

Step 2 : The Chartered Accountant Certifies

The assigned CA receives the request in their Income Tax e-Filing portal login under Worklist → For Your Action. Before certifying, the CA must independently verify the three conditions that the law requires: that the payee has filed their return under Section 139, that the specific income paid by the deductor is included in that return, and that the tax due on the declared income has been paid. This verification must be based on actual examination of the payee’s return, acknowledgement, Form 26AS, and tax payment records — not merely on representations made by the payee or the deductor.

The CA fills in the payee’s return filing details — date of filing, acknowledgement number, ITR form type, declared income, tax payable, and tax paid — and submits the certificate in the prescribed Annexure A format, using their own DSC.

Step 3 : The Deductor Finalises Submission

Once the CA submits, the deductor logs back into the e-Filing portal and submits Form 26A using DSC or EVC. TRACES then processes the form and recalculates the TDS default position. If accepted, the deductor’s status changes from assessee-in-default to relieved, and TRACES recomputes the interest under Section 201(1A) for the applicable period.

What the CA Must Actually Verify

Rule 31ACB of the Income Tax Rules, 1962, which prescribes Form 26A, requires that the CA examine the relevant accounts, documents, and records of the payee — not merely accept verbal confirmation. In practice, this means obtaining and retaining copies of:

The payee’s ITR acknowledgement for the relevant assessment year

The payee’s tax computation showing the disputed income was included

Evidence of tax payment (Challan / Form 26AS / AIS)

The deductor’s TDS return showing the transaction in question

A certification that is done without this documentation is not merely careless it is professionally exposed, and could be challenged during assessment, converting a resolved matter into an active dispute.

Conclusion .

Form 26A is useful in a TDS default scenario, but it is not a complete solution.

Form 26A is a useful and legally sound mechanism. When used correctly, with proper CA verification, it provides genuine protection against the assessee-in-default label under Section 201(1).

But it is not a complete fix. Interest under Section 201(1A) still runs. Expense disallowance under Section 40(a)(ia) is a separate question. And the certification itself carries responsibility it must be done with proper documentary verification, not as a formality.

If your business has missed TDS deductions or if you are not entirely sure whether you have a structured compliance review before scrutiny is always the better path. Catching the issue early limits the damage; discovering it during a notice limits your options.

Frequently Asked Questions

1. What is Form 26A in TDS?

Form 26A is a certificate issued by a Chartered Accountant confirming that the payee has included the relevant income in their return of income and paid the applicable taxes. When furnished properly, it allows the payer to claim relief from being treated as an assessee-in-default under Section 201(1) of the Income Tax Act. (Learn more about TDS defaults and compliance https://www.adwaniandco.com/services

2. Does Form 26A completely remove TDS liability?

No. Form 26A only removes the assessee-in-default classification under Section 201(1), subject to all three payee conditions being met. Interest liability under Section 201(1A) still applies, and the question of expense disallowance under Section 40(a)(ia) is an entirely separate matter.

3. Is interest payable even after filing Form 26A?

Yes. Interest under Section 201(1A) continues to apply and is calculated from the date TDS was originally required to be deducted to the date the payee files their return of income. Form 26A does not eliminate this interest.

4. When should Form 26A be filed?

Form 26A should be filed once it is confirmed that the payee has filed their return of income, included the relevant income in that return, and paid the tax due. The sooner this is done after a default is identified, the better as delay increases interest exposure.

5. What happens if Form 26A is not filed?

Without Form 26A, the payer remains classified as an assessee-in-default under Section 201(1). This can result in a tax demand, interest under Section 201(1A), and potential disallowance of the expense under Section 40(a)(ia). The default also stays on formal record, which can complicate future assessments.

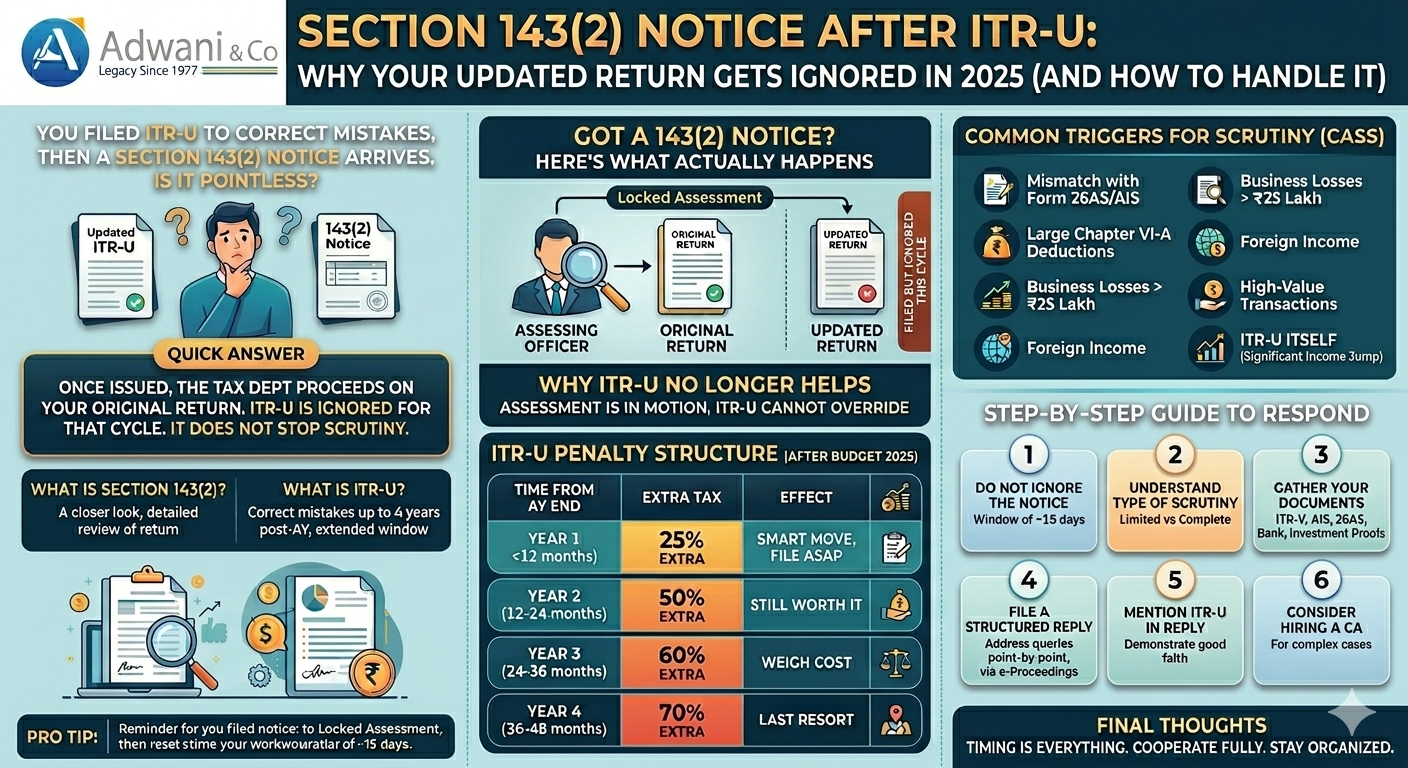

You did everything right. You filed your Income Tax Return, then realized you missed some income a forgotten freelance payment, some interest from a savings account, maybe rental income you overlooked. So you did the responsible thing: you filed an Updated Return (ITR-U) to correct it.

Then the letter arrived.A Section 143(2) notice after ITR-U. And suddenly that correction you filed feels pointless. This is one of the most misunderstood situations in Indian income tax and it catches thousands of honest taxpayers off guard every year.

Quick Answer: Once a Section 143(2) notice after ITR-U is issued, the tax department proceeds on your original return. Your updated return is filed but ignored for that assessment cycle. Filing ITR-U after the notice does NOT stop scrutiny and does NOT update the return being examined.

What is Section 143(2) Notice After ITR-U?

Understanding Section 143(2) in Simple Terms

Section 143(2) of the Income Tax Act is basically the tax department saying: “We have selected your return for a closer look.” It is a scrutiny notice meaning an Assessing Officer (AO) will review your return in detail to make sure you have not underreported income, overclaimed deductions, or underpaid tax.

This notice must be issued within 3 months from the end of the financial year in which you filed your return. If you filed your ITR on 31st July 2024, the last date for this notice is 30th June 2025.

What is ITR-U (Updated Return)?

ITR-U is a provision under Section 139(8A) that lets you correct a previously filed return or even file one you missed entirely. After Budget 2025, the window to file an ITR-U has been extended from 2 years to 4 years from the end of the relevant Assessment Year. This is a huge change that gives taxpayers much more time to come clean voluntarily.

Got a 143(2) Notice After Filing ITR-U? Here is What Actually Happens

Here is where things go wrong. When you receive a Section 143(2) notice after ITR-U, the assessment is locked onto your original return. The Assessing Officer proceeds on what you originally filed your ITR-U correction is set aside for that cycle. It is not that your ITR-U disappears, it is just that it cannot change the course of the ongoing scrutiny.

This is established under CBDT guidelines and supported by multiple tribunal rulings across India.

Filed ITR-U But Got a 143(2) Notice? Here is Why It No Longer

Helps Think of it this way. Imagine a court case is already running. You cannot suddenly submit new evidence from outside and expect the proceedings to restart from scratch. The same logic applies here.

Once scrutiny proceedings begin under Section 143(3), the assessment is in motion. Your ITR-U filed after a Section 143(2) notice after ITR-U cannot override or pause this process. The law is clear on this the updated return has no bearing on an assessment that is already underway.

A Real-World Example

Arjun, a software engineer in Pune, forgot to report Rs. 3 lakh in freelance income from a foreign client. He filed ITR-U to disclose it. But two weeks before filing ITR-U, he had already received a Section 143(2) notice for the same year.

Result: The AO ignored the ITR-U, conducted scrutiny on the original return, added the Rs. 3 lakh as undisclosed income, and imposed a penalty. Arjun had to cooperate with the scrutiny process his ITR-U counted for nothing in that cycle.

Common Triggers That Cause Section 143(2) Notice After ITR-U

Not every taxpayer gets selected for scrutiny.

The tax department uses a system called CASS (Computer Assisted Scrutiny Selection) to automatically flag cases. Here are the most common reasons your case might be picked:

Mismatch with Form 26AS or AIS: If the income shown in your ITR does not match what banks, employers, or other sources have reported, the system flags it automatically.

Large deductions under Chapter VI-A: Claiming very high 80C, 80D, or home loan deductions compared to your income level raises a red flag.

Business losses above Rs. 25 lakh: Loss claims are always scrutinized more carefully.

ITR-U itself can trigger scrutiny: Ironically, filing a large update can draw attention. If your ITR-U shows a significant jump in income from the original, it may invite the very notice you were trying to avoid.

Foreign income or overseas assets: NRIs and those with foreign bank accounts or investments are subject to stricter scrutiny.

High-value transactions not disclosed: Property sales, large cash deposits, or luxury purchases appearing in your AIS but missing from your ITR.

In the financial year 2024-25 alone, over 1.5 lakh cases were selected for scrutiny a 20% increase from the previous year. With AI-driven audits becoming the norm, this number is only going to grow.

Step-by-Step Guide to Respond to Section 143(2) Notice After ITR-U

Receiving this notice is stressful. But it does not have to be a disaster. Here is exactly what to do, in order:

Step 1: Do Not Ignore the Notice

This is the most critical point. Ignoring a Section 143(2) notice after ITR-U is the worst thing you can do. You have a window typically 15 days to acknowledge the notice through the e-Proceedings portal on the Income Tax website. Log in, go to e-Proceedings, and confirm receipt.

Step 2: Understand What Type of Scrutiny You Are Under

There are two types. Limited scrutiny means the AO can only examine specific issues mentioned in the notice for example, a mismatch in capital gains or TDS credits. Complete scrutiny means your entire return is being reviewed. Knowing which one you are dealing with helps you prepare.

Step 3: Gather Your Documents

ITR-V (acknowledgement of your original filed return)

Form 26AS and Annual Information Statement (AIS)

Bank statements for the full financial year

Investment proofs for all deductions claimed (80C, 80D, HRA, etc.)

Details of all income sources including salary slips, rent agreements, freelance invoices

Copy of your ITR-U filing acknowledgement

Step 4: File a Structured Reply

Your reply must address each query raised in the notice, point by point. Use a professional format with clear headings. Attach supporting documents as PDF scans. All replies must go through the e-Proceedings portal emails or physical visits have no legal value under the faceless assessment system.

Step 5: Mention Your ITR-U in the Reply

Even though your ITR-U does not override the scrutiny, mention it in your submission. State clearly that you had filed an Updated Return to voluntarily disclose additional income this demonstrates good faith and may be considered during penalty determination.

Step 6: Consider Hiring a CA

If your case involves complex income sources, large deductions, or significant additional tax demand, hire a Chartered Accountant. Scrutiny proceedings involve technical legal language and strict deadlines. A CA who handles tax assessments regularly will know exactly what to say, what to submit, and how to protect you.

Step 7: Appeal if the Order is Unfavorable

After the AO passes the final order under Section 143(3), you have 30 days to file an appeal with the Commissioner of Income Tax (Appeals) or CIT(A). If you have cooperated fully and have documented everything properly, your chances of getting relief on appeal are good.

Pro Tip: Track your case status by logging into incometax.gov.in and checking the e-Proceedings tab. If a Section 143(2) notice after ITR-U has been issued, it will appear here. You will also receive an email and SMS to your registered contact details.

Three Real Case Studies: What Happened to Taxpayers Like You

Case 1: Salaried Employee Who Cooperated Fully

Rajesh, a 34-year-old engineer from Pune, had forgotten to report a Rs. 2 lakh performance bonus from a previous employer. He filed ITR-U to correct this but had already received a Section 143(2) notice after ITR-U for the same year. His ITR-U was ignored in the scrutiny. However, Rajesh cooperated fully, submitted all documents on time, and mentioned the ITR-U as evidence of good faith. The AO raised a demand of Rs. 50,000. On appeal, Rajesh got relief and the demand was reduced significantly.

Case 2: Small Business Owner Who Caught a Break

Priya ran a small cafe and had claimed excess depreciation on her equipment. She filed ITR-U late. A Section 143(2) notice followed. The AO examined her original return and questioned the depreciation claim. Priya submitted invoices, purchase records, and depreciation schedules. The final demand was reduced by 40% from the initial assessment.

Case 3: Freelancer Who Ignored the Notice A Warning

Vikram, a graphic designer, received a Section 143(2) notice after ITR-U but assumed it would resolve itself. He did not respond. The AO passed a best judgment assessment under Section 144 essentially guessing his income based on available data and raised a demand of nearly double the actual tax due, plus a 200% penalty.

How to Prevent Section 143(2) Notice After ITR-U in the Future

Prevention is always better than a cure. Here is how to reduce the chances of landing in this situation again:

File accurately the first time: Cross-check your ITR against Form 26AS and the Annual Information Statement (AIS) before submitting. Most mismatches that trigger scrutiny are simple oversights.

Use ITR-U only before any notice: If you realize a mistake, file ITR-U as soon as possible before any scrutiny notice arrives. The 4-year window gives you plenty of time, but earlier is always better.

Use the pre-fill option on the e-filing portal: The portal automatically pulls data from your AIS, Form 26AS, and employer records. Using this reduces the chance of missing income.

Keep all financial documents organized: Rent agreements, investment proofs, bank statements, salary slips keep these ready every year. Scrutiny can happen to any return, anytime.

Hire a CA for complex cases: If your annual turnover exceeds Rs. 1 crore, you have multiple income sources, or you have foreign assets do not file alone. Professional guidance upfront is far cheaper than fighting a scrutiny assessment later.

Frequently Asked Questions

1.Can I file ITR-U after receiving a 143(2) notice?

Technically yes you can still file ITR-U after receiving the notice. But it will be ignored for the ongoing scrutiny assessment. The Assessing Officer will proceed on your original return. Your ITR-U may still count as a gesture of good faith during penalty proceedings

2.Does filing ITR-U stop a 143(2) notice?

No. Filing ITR-U has no power to stop, pause, or cancel a Section 143(2) scrutiny notice. Once issued, the notice runs its full course regardless of any ITR-U filed before or after.

3.How long does a scrutiny assessment take?

Typically between 6 months to 1.5 years from the date of the notice. Under the faceless assessment system, the entire process is digital and can move faster than traditional scrutiny.

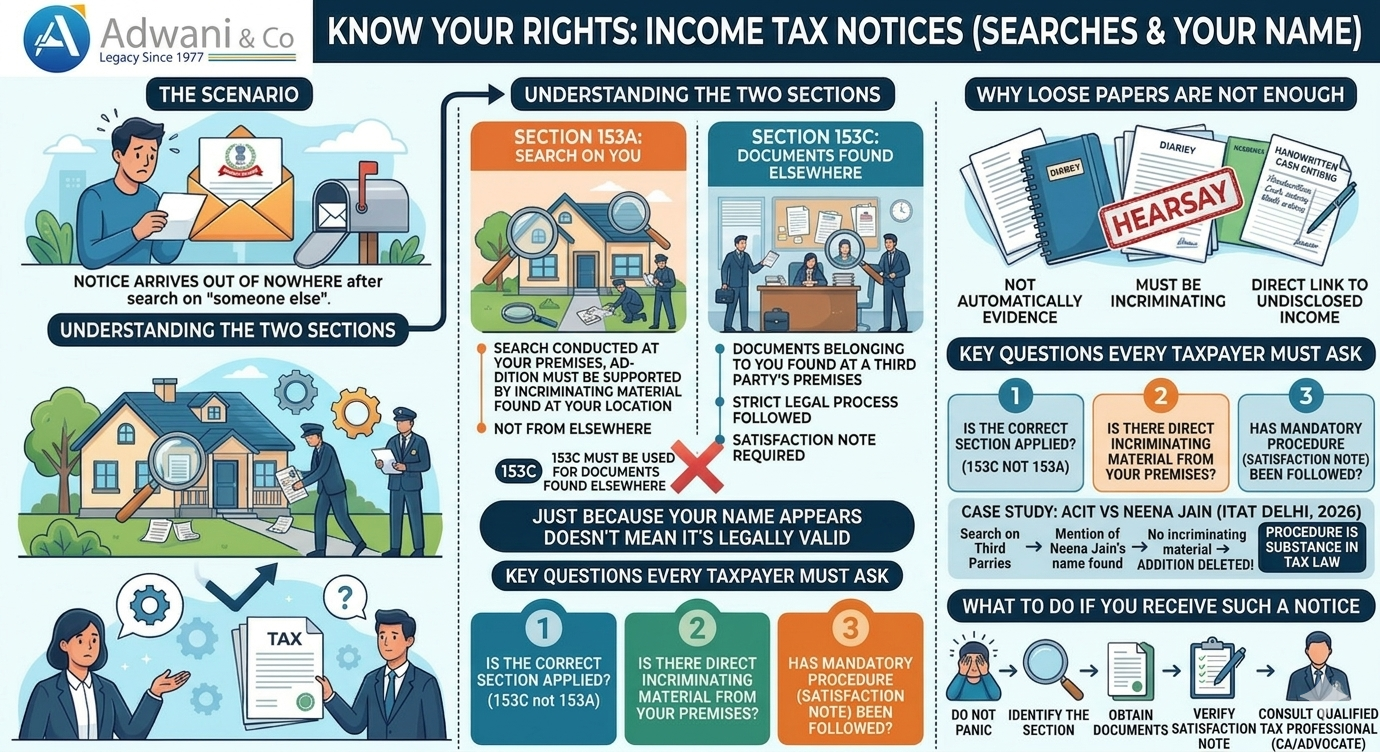

Notice Under Section 153C: What to Do if Your Name is in Someone Else’s Papers. Protect your rights and challenge wrongful tax demands with Adwani & Co.

When tax authorities find your name in a third party’s documents during a search, the law draws a sharp line between what is permissible and what is not. Most taxpayers and even some officers get this wrong.

The Notice That Arrives Out of Nowhere

Imagine opening your mailbox one ordinary morning to find an income tax notice. The search was not on you. No officer visited your home. No documents were seized from your premises. Yet there it is a notice proposing a significant addition to your income, based on papers found at someone else’s address.

This is not a rare scenario. It happens frequently across India, and it leaves taxpayers confused, anxious, and often vulnerable to wrongful demands. The good news? The law is clear if you know where to look.

Key insight: Just because your name appears in a document does not mean an income tax addition against you is legally valid. The section under which proceedings are initiated matters enormously.

The Income Tax Act, 1961 lays down two distinct legal pathways when a search or seizure operation takes place. Confusing one for the other is not merely a paperwork error it can invalidate the entire proceeding.

Section 153A

Search on YOU

Applies when income tax authorities conduct a search directly on your premises. Any addition made must be supported by incriminating material found at your location. Not from elsewhere from your address.

Section 153C

Documents found elsewhere

Applies when documents or assets belonging to you, or referring to you, are found during a search at a third party’s premises. A strict legal process, including a satisfaction note, must be followed before you can be assessed.

The distinction is not technical hair-splitting. It is the foundation of a fair assessment. When the wrong section is applied, the entire addition is built on a procedurally defective foundation and courts have consistently held that such additions cannot stand.

Don’t panic over a Section 153C notice. Follow these 5 critical steps to protect your rights and challenge wrongful tax additions with expert advice.

5 Critical Steps to Take Immediately

Identify the Section: Verify if the notice is under Section 153A or 153C. If no search occurred at your premises, 153A is likely invalid.

Verify the Satisfaction Note: Ensure the Assessing Officer recorded a formal “satisfaction note” before proceeding.

Inspect the Evidence: Demand to see the “incriminating material.” Remember, casual mentions in loose papers are often not enough.

Check for Procedural Errors: In tax law, procedure is substance. A wrong section means the entire addition could be deleted.

Consult a Professional: Engage a qualified tax advocate or CA at Adwani & Co to draft a technically sound response.

What Went Wrong in ACIT vs Neena Jain (ITAT Delhi, 2026)

This recently decided case before the Income Tax Appellate Tribunal, Delhi, is a textbook example of procedural overreach and how the law protects taxpayers when authorities step outside their legal bounds.

Case Study

ACIT vs Neena Jain ITAT Delhi, 2026

A search and seizure operation was conducted but on third parties, not on the assessee.

During that search, loose papers and handwritten cash entries were discovered that allegedly mentioned Neena Jain’s name.

The department initiated proceedings against her under Section 153A the section that applies only when a search is conducted on the taxpayer herself.

No incriminating material was found from the assessee’s own premises. The entire case rested on third party documents.

The mandatory procedure under Section 153C including a formal satisfaction note from the Assessing Officer was not followed.

The ITAT held that the addition was entirely unsustainable. The wrong section had been invoked, there was no incriminating material against the assessee, and the entire addition was deleted.

Why Loose Papers Are Not Enough

Tax law does not operate on suspicion or inference alone. Loose papers found at a third party’s premises a diary, a note, a printed ledger entry are not automatically evidence against the person named in them. The courts have repeatedly emphasised that the word “incriminating” is key.

Incriminating material means evidence that directly implicates the assessee not hearsay, not casual mentions, not unverified entries in someone else’s records. For an addition to survive legal scrutiny, there must be a direct and demonstrable link between the document and the assessee’s undisclosed income.

What counts as incriminating material? Documents, assets, or entries that directly and specifically indicate the taxpayer’s undisclosed income or unexplained investment and which were found during a valid search of their own premises.

The Three Questions Every Taxpayer Must Ask

Before filing a reply to any income tax notice arising from a search whether on you or on someone else take a step back and ask these three questions systematically. The answers could determine whether any addition against you survives at all.

Is the correct section being applied?

If the search was not on your premises, the department must proceed under Section 153C, not 153A. Any notice issued under the wrong section is procedurally invalid from the outset.

Is there direct incriminating material against you?

The tax department must point to specific documents or assets found from your premises that establish undisclosed income. A mere mention of your name elsewhere is not sufficient.

Has the mandatory procedure been followed?

Under Section 153C, the Assessing Officer of the searched person must record a satisfaction note establishing that the documents belong to or pertain to you. Without this, the proceeding has no legal basis.

The Broader Lesson Procedure Is Substance in Tax Law