Unlock the Section 80CCD(2)

Every tax season, salaried employees and employers spend hours debating what the New Tax Regime took away HRA, LTA, and most of Chapter VI-A. But almost nobody is asking the more useful question: what did it quietly make better? Hidden inside the Income Tax Act is a provision that most taxpayers overlook, and it happens to be one of the few deductions that genuinely improved when the New Tax Regime came into force. That provision is the Section 80CCD(2) deduction, and understanding it properly could change how you and your employer structure salary for FY 2026-27.

If you are a private sector employee, a payroll manager, or a founder trying to design a competitive and tax-efficient compensation package, this guide breaks down exactly how the Section 80CCD(2) deduction works, how much you can legitimately claim, and why so many employers have not yet updated their policies to take advantage of it.

What Is the Section 80CCD(2) Deduction?

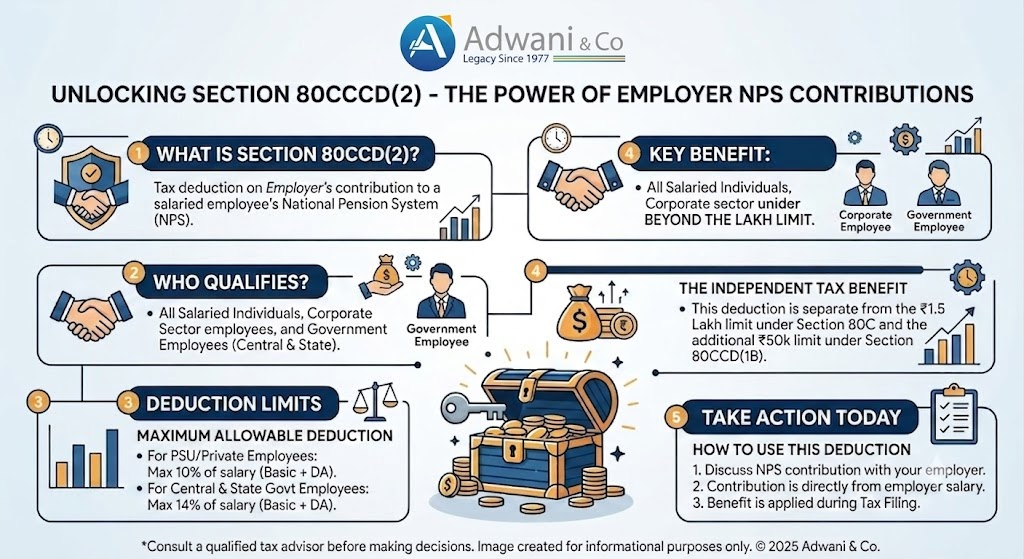

The Section 80CCD(2) deduction relates to the employer’s contribution to an employee’s National Pension System (NPS) account. Unlike most other retirement-linked deductions, it does not disappear if you opt for the New Tax Regime it is one of a small handful of provisions that survives the shift away from the Old Tax Regime’s exemption-heavy structure.

In simple terms, when your employer contributes a percentage of your salary to your NPS account, that contribution is treated as a deductible business expense for the company and, up to a prescribed limit, is not taxable in your hands either. The Section 80CCD(2) deduction is what defines that prescribed limit and it is precisely this limit that changed favourably under the New Tax Regime.

Section 80CCD(2) Deduction Limit: Old vs New Tax Regime Compared

The clearest way to understand the improvement is to compare the Section 80CCD(2) deduction limit across both tax regimes for different categories of employees.

| Employee Category | Old Tax Regime | New Tax Regime |

| Government Employees | Up to 14% of Salary* | Up to 14% of Salary* |

| Private Sector / Other Employees | Up to 10% of Salary* | Up to 14% of Salary* |

*Salary, for the purpose of this deduction, means Basic Salary plus Dearness Allowance, to the extent it forms part of retirement benefits.

Notice what happened here. Government employees always had access to a 14% Section 80CCD(2) deduction, under both regimes. Private sector employees, however, were historically capped at 10% under the Old Tax Regime. Under the New Tax Regime, that cap has been raised to 14% bringing private sector employees to full parity with government employees for the first time.

This makes the Section 80CCD(2) deduction one of the rare instances where choosing the New Tax Regime does not mean giving something up it means gaining a genuinely larger benefit, provided your employer’s compensation structure is designed to use it.

How the Section 80CCD(2) Deduction Works for Private Sector Employees

The Section 80CCD(2) deduction is not something you claim by writing a cheque yourself. It depends entirely on your employer’s payroll and compensation policy. A few operating rules are essential to understand:

- The deduction applies only to the employer’s contribution to NPS voluntary or personal contributions you make yourself do not qualify under this section.

- Whether your employer contributes to NPS at all, and at what percentage, is a matter of company policy, not a statutory entitlement you can demand individually.

- The contribution must be routed through a recognised NPS account structure and reported correctly in payroll and Form 16.

Real Example: Calculating Your Section 80CCD(2) Deduction Benefit

Consider Priya, a private sector employee with a Basic Salary plus DA of ₹12,00,000 per year, who has opted for the New Tax Regime for FY 2026-27.

- Under the Old Tax Regime, her employer could contribute a maximum of 10% of ₹12,00,000 = ₹1,20,000 towards NPS, and this entire amount would qualify for the Section 80CCD(2) deduction.

- Under the New Tax Regime, her employer can now contribute up to 14% of ₹12,00,000 = ₹1,68,000 towards NPS, and this larger amount qualifies for the Section 80CCD(2) deduction.

- That is an additional ₹48,000 of tax-free retirement contribution every year simply by aligning the compensation structure to the New Tax Regime’s enhanced limit.

Over a working career, that difference compounds significantly, both in terms of tax efficiency and retirement corpus growth. This is exactly the kind of practical, numbers-based planning that separates a well-structured salary from a generic one.

The ₹7.5 Lakh Aggregate Cap on Employer Retirement Contributions

The Section 80CCD(2) deduction does not operate in isolation. Under Section 17(2)(vii) of the Income Tax Act, the combined employer contribution to NPS, Recognised Provident Fund (RPF), and Approved Superannuation Fund is capped at an aggregate of ₹7.5 lakh per year. Any amount contributed beyond this combined threshold becomes taxable as a perquisite in the employee’s hands, along with any notional interest or growth attributable to the excess.

Key Takeaways

The Section 80CCD(2) deduction covers only the employer’s NPS contribution, not personal contributions.

Private sector employees can now claim up to 14% of salary under the New Tax Regime, up from 10% under the Old Tax Regime.

Government employees continue to enjoy a 14% deduction limit under both regimes.

Combined employer contributions to NPS, RPF, and superannuation fund are capped at ₹7.5 lakh annually under Section 17(2)(vii). This is one of the few deductions where the New Tax Regime is genuinely more generous than the Old Tax Regime.

Frequently Asked Questions

1. Is the Section 80CCD(2) deduction available under the New Tax Regime?

Yes. Unlike most Chapter VI-A deductions, the Section 80CCD(2) deduction for employer NPS contribution remains available under the New Tax Regime, at an even higher limit for private sector employees.

2. What is the current Section 80CCD(2) deduction limit for private sector employees?

Private sector employees can claim a Section 80CCD(2) deduction of up to 14% of salary (Basic + qualifying DA) under the New Tax Regime, compared to 10% under the Old Tax Regime.

3. Can I claim the Section 80CCD(2) deduction for my own NPS contributions?

No. The Section 80CCD(2) deduction applies only to the employer’s contribution. Personal NPS contributions are governed separately under Sections 80CCD(1) and 80CCD(1B).

4. Is there a cap on combined employer contributions to retirement funds?

Yes. Under Section 17(2)(vii), combined employer contributions to NPS, RPF, and Approved Superannuation Fund are capped at ₹7.5 lakh annually, with any excess taxed as a perquisite.

5. Do government employees benefit from the same Section 80CCD(2) deduction increase?

No change applies to them government employees already had access to a 14% deduction limit under both the Old and New Tax Regimes.

6. Should my employer revise our compensation policy for this deduction?

It is worth a professional review. Structuring part of compensation as an employer NPS contribution can materially improve tax efficiency for employees without added cost to the company.

Read our detailed guide on Old vs New Tax Regime2025: Stop Guessing, Start Calculating

ITR Filing 2026: Deadlines, Penalties & Smart Tax Saving Guide

Conclusion: A Deduction Worth Structuring Around

The New Tax Regime is usually framed as a trade-off — simpler slabs in exchange for fewer deductions. The Section 80CCD(2) deduction tells a different story. For private sector employees, it is a genuine improvement, and it only delivers value when the employer’s compensation structure is built to capture it. As FY 2026-27 progresses, reviewing whether your salary structure is optimised for the Section 80CCD(2) deduction is one of the simplest, highest-value exercises a business can undertake.

If you want expert guidance on structuring your compensation policy around the Section 80CCD(2) deduction, or on any aspect of tax planning under the New Tax Regime, connect with Adwani & Co LLP today.

About the Author:

Mukesh Chavan is a dedicated indirect taxation and compliance professional associated with Adwani & Co LLP, specializing in GST advisory, GST audits, GST assessments, and RERA compliance services. With extensive experience in handling complex regulatory matters, he assists businesses in ensuring compliance with evolving GST laws and real estate regulations while minimizing risks and enhancing operational efficiency.

Mukesh has successfully guided clients through GST registrations, return compliance, departmental assessments, audits, litigation support, and tax planning strategies. He also possesses significant expertise in RERA compliance, helping real estate developers, promoters, and stakeholders navigate regulatory requirements and maintain seamless project compliance.

Through his articles and professional insights, Mukesh aims to simplify complex GST and RERA provisions, offering practical guidance that empowers businesses to remain compliant, avoid disputes, and make informed decisions in an increasingly dynamic regulatory environment. His approach combines technical expertise with practical business understanding, enabling clients to focus on growth while meeting their statutory obligations with confidence.

Leave a Reply