Smart Tax Saving Tips

The Deadline That Most Taxpayers Ignore Until It’s Too Late

Every year, it happens the same way. A taxpayer who earned well, invested wisely, and paid their TDS on time ends up with a higher tax bill than they should have not because they broke any rules, but because they didn’t plan within the rules before the window closed.

That window closes on July 31, 2026.

This is the ITR filing last date for AY 2026-27 the hard deadline set by the Income Tax Department of India under Section 139(1) of the Income Tax Act, 1961. Whether you’re salaried, a freelancer, a business owner, or an investor with capital gains, these final weeks before July 31 are your last legitimate opportunity to optimize your tax position for FY 2025-26.

This guide covers the most powerful, actionable tax saving tips before July 31 for AY 2026-27 backed by real numbers, practical examples, and the kind of strategic clarity that most generic tax articles miss entirely.

Why Tax Saving Before July 31 for AY 2026-27 Matters More Than Ever

Filing on time is no longer just about avoiding the late fee under Section 234F (up to ₹5,000). The consequences of filing late or filing incorrectly now carry deeper implications.

The Income Tax Department’s data infrastructure has expanded significantly. Through the Annual Information Statement (AIS), the department now receives real-time data from banks, brokers, mutual fund houses, property registrars, and even the GST Portal via cross-system data sharing. Credit card transactions, cash deposits, and F&O trading activity are all tracked and matched against your ITR.

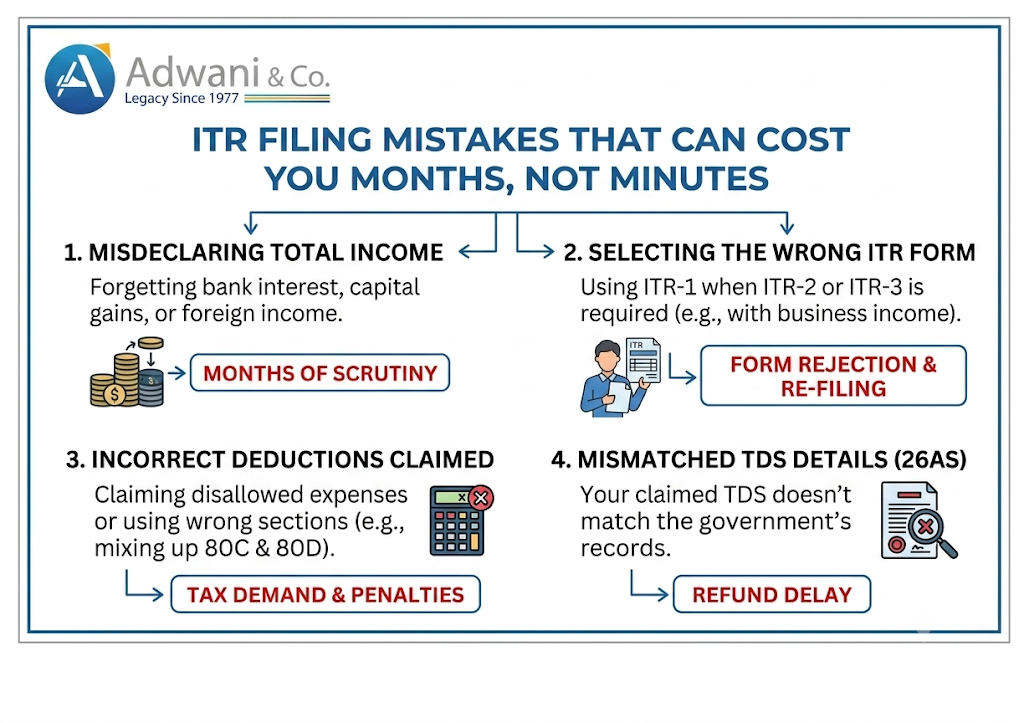

Filing with errors or missing deductions in this environment means:

- Delayed or rejected refunds due to TDS credit mismatches

- Income tax notices triggered by AIS-ITR discrepancies

- Loss of carry-forward rights for F&O losses and capital losses

- Missed deduction claims that can never be retroactively corrected once the deadline passes

The most effective tax saving strategy for AY 2026-27 begins not on July 30th, but right now

Tax Saving Tip 1 : Old vs New Tax Regime: The Most Important Choice of AY 2026-27

If there is one tax saving tip before July 31 for AY 2026-27 that carries more financial weight than all others combined, it is this: choose your tax regime deliberately, not by default.

The new tax regime for FY 2026-27 offers zero tax on income up to ₹12 lakh after the Section 87A rebate, along with a simplified slab structure and a standard deduction of ₹75,000 for salaried employees and pensioners a figure significantly improved from the prior ₹50,000 available under the old regime.

The old tax regime preserves the full deduction ecosystem. This matters enormously for taxpayers who have:

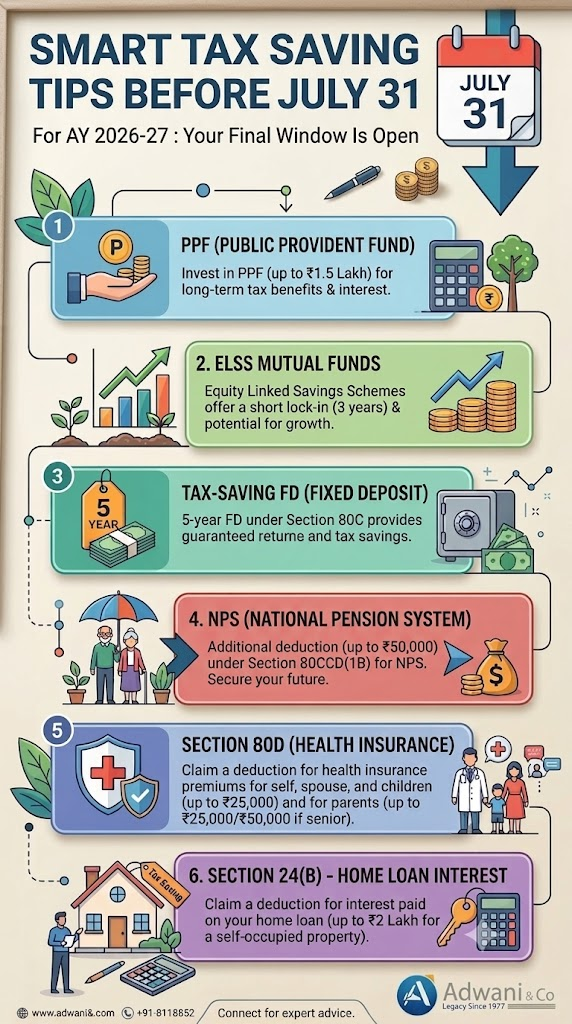

- Section 80C investments : ELSS, PPF, LIC premium, home loan principal, NSC, tuition fees (up to ₹1.5 lakh)

- Section 80D : Health insurance premiums (up to ₹25,000 for self/family; ₹50,000 for senior citizen parents)

- Section 24(b) : Home loan interest deduction (up to ₹2 lakh for self-occupied property)

- HRA exemption : For salaried employees living in rented accommodation

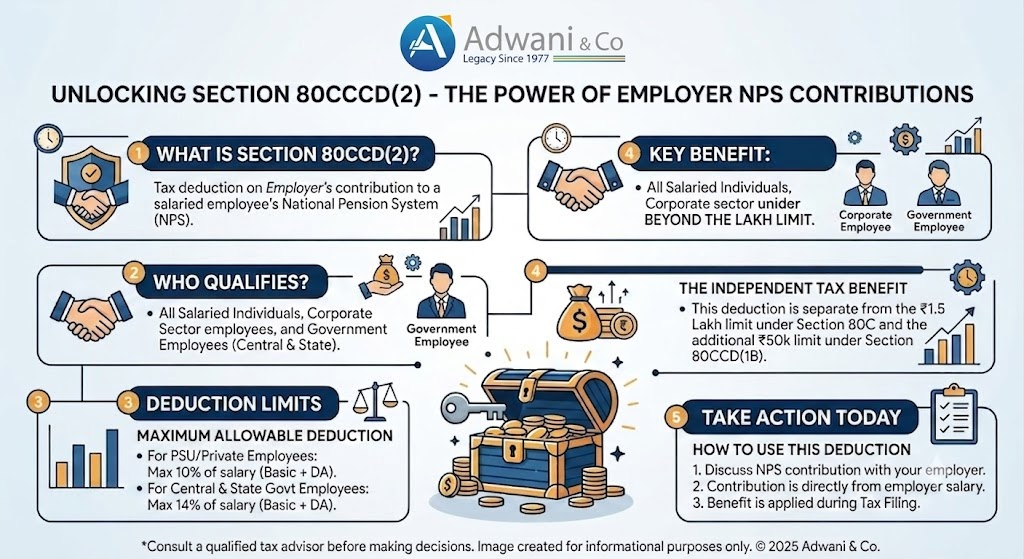

- Section 80CCD(1B) : Additional ₹50,000 for NPS contributions, above the 80C ceiling

Practical Comparison Example:

| Scenario | Salaried, Income ₹14 lakh | New Regime Tax | Old Regime Tax |

| Standard deduction | ₹75,000 | ₹75,000 | ₹50,000 |

| Section 80C | ₹1.5 lakh | Not applicable | Claimed |

| Section 80D | ₹25,000 | Not applicable | Claimed |

| Home loan interest | ₹1.5 lakh | Not applicable | Claimed |

| Effective taxable income | ~₹13.25L | ~₹10.5L | |

| Approximate tax | ~₹1,17,500 | ~₹82,500 |

In this example, the old regime saves approximately ₹35,000. But for someone without these deductions, the new regime wins decisively. There is no universal answer only a calculated one.As Dr. Haresh Adwani, PhD in Commerce and law graduate, founding partner of Adwani and Company, puts it: “The regime decision is not a checkbox. It is a financial calculation. We see taxpayers every year who lock in the wrong regime because they assumed not because they calculated.”Read our detailed guide on Old vs New Tax Regime 2026 before filing your ITR

Tax Saving Tip 2 : Claim Every Deduction Before the July 31 Deadline

Many taxpayers who opt for the old regime still underclaim deductions not because they’re ineligible, but because documentation is incomplete at the time of filing. Here’s the full Section 80C deductions checklist for AY 2026-27:

High-Impact Deductions to Capture Before July 31

Section 80C : ₹1.5 lakh ceiling (Old Regime only): ELSS mutual funds, PPF, LIC premium, EPF (employee’s share), NSC, 5-year tax-saving FD, children’s tuition fees, home loan principal repayment

Section 80D : Health Insurance: ₹25,000 for self/spouse/children + ₹50,000 for senior citizen parents. Preventive health check-up expenses of up to ₹5,000 are included within these limits.

Section 80CCD(1B) : NPS: ₹50,000 additional over and above 80C. For a taxpayer in the 30% bracket, this alone reduces tax by ₹15,600.

Section 24(b) : Home Loan Interest: Up to ₹2 lakh on a self-occupied property. For let-out property, full interest is deductible (subject to the ₹2 lakh set-off cap).

HRA Exemption: Calculated as the least of: actual HRA received, rent paid minus 10% of basic salary, or 50%/40% of basic salary (metro/non-metro cities). Ensure rent receipts are ready and landlord’s PAN is available if annual rent exceeds ₹1 lakh.

Learn more about our ITR Filing Service to ensure every deduction is accurately captured before the filing deadline.

Tax Saving Tip 3 : Reconcile AIS and Form 26AS Before Filing ITR

One of the most impactful and most skipped tax saving actions before July 31 for AY 2026-27 is a thorough pre-filing reconciliation of your AIS (Annual Information Statement) and Form 26AS.

These documents show what third parties banks, employers, brokers, mutual funds have reported to the Income Tax Department against your PAN. Mismatches between your ITR and the AIS cause:

- Delayed refund processing

- Defective return notices

- Demand notices for income you didn’t actually earn (due to PAN errors in the AIS)

Importantly, TDS already deducted from your interest income, rent received, or capital gains transactions is a prepaid tax. If those credits aren’t correctly claimed in your ITR, you’re effectively overpaying the government and getting nothing in return.

Dr. Haresh Adwani notes: “Every filing at Adwani and Company begins with a full AIS-Form 26AS review. It’s the foundation. Without it, you’re filing blind.”

Tax Saving Tip 4 : Capital Gains Reporting: LTCG, STCG & F&O for AY 2026-27

LTCG and STCG tax on shares and mutual funds for AY 2026-27 has been restructured by the Union Budget 2024 amendments. Understanding the current rates is a critical income tax saving strategy before you file.

Revised Capital Gains Tax Rates

| Asset Type | Holding Period | Tax Rate (Post-Budget 2024) |

| Listed equity / equity MFs | < 12 months (STCG) | 20% flat |

| Listed equity / equity MFs | ≥ 12 months (LTCG > ₹1.25L) | 12.5% (no indexation) |

| Debt mutual funds (post Apr 2023) | Any | As per income slab |

| Property / unlisted shares | ≥ 24 months (LTCG) | 12.5% (no indexation) |

Practical Example LTCG Planning:

A taxpayer sold equity mutual fund units in January 2026 with a long-term capital gain of ₹2,80,000. The first ₹1,25,000 is fully exempt. The remaining ₹1,55,000 is taxed at 12.5%, resulting in a tax liability of ₹19,375 compared to ₹46,500 if mistakenly taxed at 30%.

F&O Loss Carry Forward A Time-Sensitive Tax Benefit:

Losses from Futures & Options trading are treated as non-speculative business losses. These can be set off against other business income and carried forward for up to 8 years — but only if the ITR is filed by July 31. Filing late permanently forfeits this benefit under Section 80 of the Income Tax Act.

Tax Saving Tip 5 : Freelancers and Business Owners: Presumptive Taxation for AY 2026-27

For freelancers, consultants, and small business owners, presumptive taxation under Section 44AD and 44ADA in 2026 remains one of the most powerful legal tax reduction tools available.

Section 44ADA (for professionals doctors, architects, lawyers, CAs, engineers):

- Declare 50% of gross receipts as taxable income

- No requirement to maintain books of accounts (for receipts up to ₹75 lakh)

- Significantly simplifies ITR filing for freelancers in India 2026

Section 44AD (for small businesses):

- Declare 8% of turnover (6% for digital transactions) as income

- Available for turnovers up to ₹3 crore

This approach eliminates the complexity of proving individual expenses and reduces effective tax significantly for service professionals.

Tax Saving Tip 6 : GST Compliance Before July 31 Reduces Risk and Penalty

Tax saving isn’t limited to income tax. For business owners and professionals, GSTR-3B filing compliance in 2026 directly impacts cash flow and audit risk.

The GST Portal now uses AI-driven cross-verification to match GSTR-1 against GSTR-3B, flag input tax credit eligibility 2026 mismatches, and identify GSTR-2B reconciliation gaps. Discrepancies between these returns and your income tax filings can trigger both a GST scrutiny notice and an income tax inquiry simultaneously as both systems now share data.

Key GST actions before July 31:

- Reconcile GSTR-2B with your purchase register to ensure no ITC mismatch notice exposure

- Ensure GSTR-3B figures match GSTR-1 for all prior periods

- Clear any outstanding GST return late fee penalties to maintain clean compliance history

- Update GST registration records if business address, directors, or turnover category has changed

Tax Saving Tip 7 : Advance Tax Planning for FY 2026-27

If your income includes freelancing fees, business profits, capital gains, rental income, or F&O trading, advance tax compliance for FY 2026-27 is your responsibility and the next due date matters for AY 2027-28 planning.

| Installment | Due Date | Cumulative % of Tax |

| 1st (already passed) | June 15, 2026 | 15% |

| 2nd | September 15, 2026 | 45% |

| 3rd | December 15, 2026 | 75% |

| 4th | March 15, 2027 | 100% |

Taxpayers who underestimate income especially those with significant capital gains from equity or F&O profits frequently end up with interest under Sections 234B and 234C. Reviewing your expected FY 2026-27 income after filing the AY 2026-27 ITR is proactive planning.

Key Takeaways : Tax Saving Tips Before July 31 for AY 2026-27

- July 31, 2026 is the last date to file ITR for AY 2026-27 late filing attracts ₹5,000 penalty under Section 234F

- Regime selection (old vs new) must be calculated, not assumed it’s the single biggest tax lever available

- Standard deduction of ₹75,000 is available under the new regime for salaried individuals

- AIS and Form 26AS reconciliation is mandatory before filing it protects your refund and prevents notices

- LTCG on equity above ₹1.25 lakh is taxed at 12.5% report it correctly in Schedule CG

- F&O losses can only be carried forward if ITR is filed by July 31 filing late forfeits this right permanently

- Freelancers and professionals can dramatically reduce tax via Section 44ADA presumptive taxation

- GST compliance gaps before July 31 can trigger cross-system notices clean both systems together

Frequently Asked Questions

Q1. What is the last date to file ITR for AY 2026-27?

ITR filing last date for AY 2026-27 is July 31, 2026 for individuals, HUFs, and non-audit cases. Filing after this deadline attracts a late fee of up to ₹5,000 under Section 234F, and you permanently lose the right to carry forward certain losses.

Q2. Which tax regime saves more money in AY 2026-27?

It depends on your deduction profile. The new regime is advantageous if your deductions are limited. The old regime wins when significant 80C, home loan interest, HRA, 80D, and NPS deductions are available. Always calculate both before making the selection.

Q3. What is the standard deduction under the new tax regime for AY 2026-27?

The standard deduction under the new tax regime for FY 2025-26 (AY 2026-27) is ₹75,000 for salaried employees and pensioners. It requires no documentation and is automatically deductible.

Q4. Can F&O losses be carried forward if I miss the July 31 deadline?

No. Under Section 80 of the Income Tax Act, business losses including F&O non-speculative losses can only be carried forward if the return is filed on or before the due date. Missing July 31 permanently forfeits this benefit for FY 2025-26 losses.

Q5. Is LTCG on equity mutual funds taxable in AY 2026-27?

Yes. Long-term capital gains on listed equity shares and equity mutual funds above ₹1,25,000 per year are taxable at 12.5% without indexation, following Budget 2024 amendments. The first ₹1.25 lakh of LTCG remains exempt annually.

Conclusion :Your Tax Saving Window Before July 31 for AY 2026-27 Won’t Wait

The best time to act on tax saving tips before July 31 for AY 2026-27 was three months ago. The second-best time is today.

Every element covered in this guide regime selection, deduction maximization, AIS reconciliation, capital gains reporting, GST compliance, and advance tax planning is available to every taxpayer right now. The difference between those who benefit from these provisions and those who don’t is rarely knowledge. It’s action.

The Income Tax Department has made compliance more transparent and more consequential than ever. Filing with accuracy, on time, with every legitimate deduction claimed isn’t just good practice it’s the most financially rational thing a taxpayer can do before July 31, 2026.

Dr. Haresh Adwani and the expert team at Adwani and Company bring together deep Commerce expertise, legal acumen, and decades of practical tax advisory experience to help individuals, professionals, and businesses make the most of every filing season — and avoid the costly mistakes that come from last-minute, uninformed filing.

About the Author : Prafull Nile

Prafull Nile is a senior taxation and accounting professional associated with Adwani & Co LLP, bringing over 19 years of extensive experience in direct taxation, tax audits, income tax assessments, GST audits, and financial statement finalization. He has successfully managed diverse client engagements across industries, providing strategic guidance on tax compliance, assessments, and regulatory matters. In addition to his technical expertise, Prafull leads and mentors teams, ensuring high standards of service delivery and operational excellence. His practical approach, deep understanding of tax laws, and commitment to client success make him a trusted advisor for businesses and professionals navigating complex financial and compliance requirements.