Imagine running a business that is profitable on paper — yet struggling to pay salaries at the end of the month. It sounds contradictory, but it is one of the most common crises Indian businesses face. Profit is an accounting concept; cash is reality. And the bridge between the two is financial modelling for cash flow — a discipline that, when done right, gives business owners and CFOs the power to see financial turbulence before it arrives.

In today’s fast-moving business environment, financial modelling is no longer a luxury reserved for large corporations and investment bankers. Every small business, startup, and mid-size enterprise in India needs a robust cash flow model to make smarter decisions, attract investors, and stay compliant with frameworks set by the Income Tax Department of India and the Ministry of Corporate Affairs (MCA). This guide explains everything you need to know — with practical examples, expert insights from Adwani and Company, and actionable steps you can implement today.

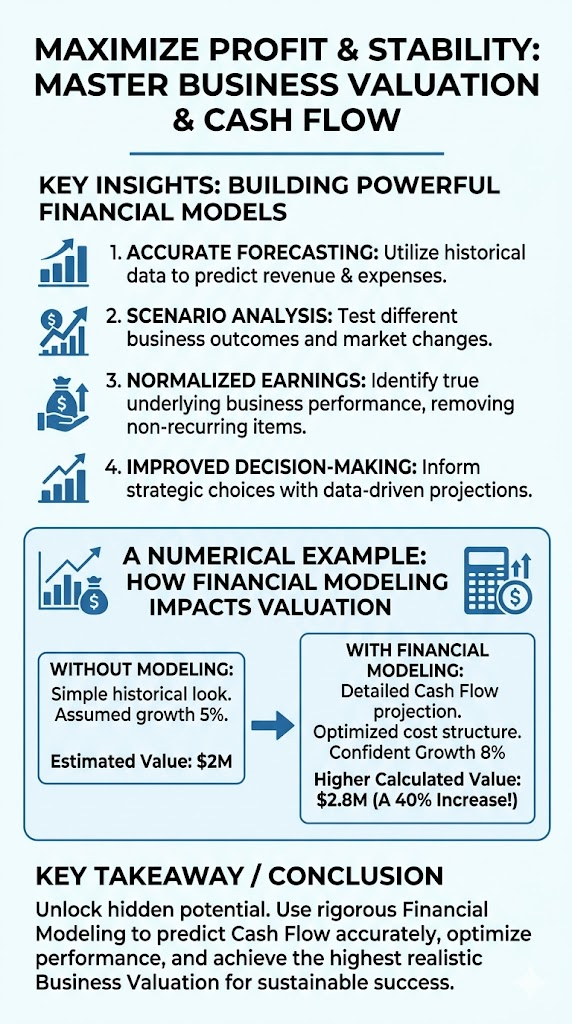

82%

of business failures are linked to poor cash flow management

40%

increase in investor confidence when a financial model is presented

3–6xI

What Is Financial Modelling for Cash Flow?

Financial modelling for cash flow is the process of building a quantitative representation of a business’s expected cash inflows and outflows over a defined period typically 12 to 36 months. Unlike a simple cash flow statement (which is historical), a financial model is forward-looking. It simulates different scenarios: what happens if a key client delays payment by 60 days? What if raw material costs spike 15%? What if a new product line launches six months late?

According to the Ministry of Corporate Affairs (MCA), companies registered under the Companies Act, 2013 are expected to maintain accurate financial records and projections as part of good corporate governance. A cash flow model is at the heart of that expectation.

At Adwani and Company, the approach to financial modelling for cash flow is grounded in three pillars: accuracy of assumptions, transparency of logic, and scenario resilience. This is the philosophy championed by Dr. Haresh Adwani a PhD holder in Commerce with a background in law whose dual expertise in financial strategy and legal compliance makes his advisory uniquely valuable for Indian businesses navigating complex regulatory environments.

Why Financial Modelling for Cash Flow Matters in Business Finance

The phrase “cash is king” is not a cliché it is a survival principle. Many businesses that appear healthy on their Profit & Loss (P&L) statement are dangerously illiquid. A well-constructed financial modelling for cash flow framework serves several critical purposes in business finance:

1. Early Warning System for Liquidity Crises

A rolling cash flow model flags potential shortfalls 60 to 90 days in advance, giving business owners the time to act — whether by negotiating extended credit terms with vendors, accelerating receivables collection, or drawing on a working capital facility.

2. Credibility with Banks and Investors

Whether you are approaching a bank for a term loan or pitching to a venture capital firm, a detailed cash flow model signals that your business is professionally managed. The Reserve Bank of India guidelines on MSME lending increasingly emphasise cash flow-based assessment over traditional collateral-based models making your financial model a direct tool for accessing better credit.

3. GST and Tax Planning Alignment

Integrating your GST outflow cycles into your cash flow model is essential. Many businesses are blindsided by large GST liability payments because they have not accounted for the timing mismatch between revenue recognition and tax payment. The GST Portal provides real-time liability data; incorporating this into your model prevents compliance-driven cash crunches.

4. Strategic Decision-Making

Should you hire five engineers this quarter? Can you afford to offer 60-day payment terms to a major new client? Can you invest ₹50 lakh in new equipment without jeopardising payroll? A financial model for cash flow answers these questions with data, not intuition.

Key Components of a Financial Modelling for Cash Flow Framework

A professional cash flow model the kind Adwani and Company builds for clients is not a single spreadsheet tab. It is an interconnected system with distinct modules:

| Module | What It Captures | Why It Matters |

|---|---|---|

| Revenue Projection | Expected sales by product, geography, or channel | Drives all inflow assumptions |

| Accounts Receivable (AR) Aging | When customers actually pay, not when invoices are raised | Most critical variable in cash timing |

| Operating Expenses | Salaries, rent, utilities, subscriptions | Fixed outflows that define minimum cash requirement |

| Tax & GST Outflows | Advance tax, TDS, GST payable cycles | Prevents compliance-driven cash crises |

| Capital Expenditure (CapEx) | Asset purchases, infrastructure investments | Large one-time outflows that must be planned |

| Debt Service | Loan EMIs, interest payments | Non-negotiable fixed outflows |

| Scenario Analysis | Best case / base case / stress case | Tests model resilience under different conditions |

How to Build a Financial Model for Cash Flow: Step-by-Step

Building an effective financial modelling for cash flow framework requires structured thinking and clean data. Here is the process that Dr. Haresh Adwani and the team at Adwani and Company recommend for Indian businesses:

- Gather 24 Months of Historical Data: Collect actual bank statements, invoices, payroll records, and tax payment receipts. The model is only as reliable as the data it is built on. For registered companies, MCA filings and ITR-6 data provide a useful starting baseline.

- Define Your Cash Inflow Drivers: Identify all sources of cash: customer payments, loans disbursed, investment inflows, asset sales. For each, define the timing lag — how many days after a sale does cash actually arrive in your bank account?

- Map Every Fixed and Variable Outflow: List all cash outflows: salaries, vendor payments, EMIs, GST, advance tax, insurance. Separate fixed costs (which exist regardless of revenue) from variable costs (which scale with activity).

- Build the 13-Week Rolling Cash Flow: Start with a short-range weekly model covering 13 weeks. This is the operational heartbeat of your business finance — it tells you exactly when your cash balance will hit critical lows and by how much.

- Extend to a 12–36 Month Forecast: Expand the model to a monthly view over 12 to 36 months, incorporating your growth assumptions, planned hirings, and capital expenditure roadmap. This is the model you will present to investors and banks.

- Run Scenario and Sensitivity Analysis: Test three scenarios: optimistic (revenue 20% above plan), base (as expected), and stress (revenue 20% below plan, customer payment delay of 30 days). This is where financial modelling for cash flow becomes genuinely powerful and where Adwani and Company adds the most value for clients.

- Review and Update Monthly: A financial model is a living document. Compare actuals versus projections each month, identify deviations, and update assumptions accordingly. The Income Tax Department of India expects businesses to maintain consistent, accurate records a well-maintained model supports that compliance.

Financial Modelling for Cash Flow: A Real World Example

Case Study: Manufacturing Company in Pune

A mid-size manufacturing company with annual revenue of ₹8 crore approached Adwani and Company after facing a sudden cash shortfall despite reporting profits of ₹72 lakh for the year.

When Dr. Haresh Adwani built a detailed financial modelling for cash flow analysis, the root cause became clear:

- The company offered 90-day payment terms to its top 3 clients (who accounted for 65% of revenue)

- But vendor payments were due in 30 days

- GST liability of ~₹9.5 lakh was due on the 20th of each month, regardless of when clients paid

- Advance tax instalments of ₹18 lakh annually were not modelled into their cash plan

The model revealed a recurring cash gap of ₹22–28 lakh every quarter during the collection lag period. The solution was a combination of renegotiating payment terms (reducing client terms to 60 days), applying for a ₹30 lakh working capital line, and restructuring the vendor payment schedule.

Within two quarters, the company’s cash buffer stabilised at ₹18 lakh enough to cover 45 days of operating expenses. Profitability did not change; only the timing management of cash improved. This is the transformative power of professional financial modelling for cash flow.

Financial Modelling Tools for Cash Flow in Indian Businesses

The right tool depends on your business size, technical capability, and the complexity of your financial model for cash flow:

Microsoft Excel / Google Sheets

For most SMEs, a well-structured Excel model remains the gold standard. It is flexible, universally understood, and easy to share with accountants and bankers. The key is disciplined structure — separate input, calculation, and output sheets — so the model does not become an unmanageable tangle of formulas.

Zoho Books / Tally Integration

Businesses already using Tally Prime or Zoho Books can extract live data to feed into their financial model for cash flow, reducing manual data entry errors significantly.

Dedicated Financial Modelling Software

Platforms like Finmark, Causal, or Cube are gaining traction among funded startups and mid-size enterprises for their real-time scenario modelling capabilities and investor-friendly dashboards.

Common Financial Modelling Mistakes That Destroy Cash Flow Accuracy

Even experienced finance professionals make errors that undermine the reliability of their financial modelling for cash flow. These are the most damaging ones to avoid:

Confusing Revenue with Cash Receipts

Recognising ₹1 crore in revenue this month means nothing if none of it has been collected. Always model cash flow based on actual payment collection dates, not invoice dates.

Ignoring Seasonal Patterns

Many Indian businesses experience sharp seasonal cash flow swings — retail peaks around Diwali, agriculture-linked businesses spike post-harvest, and B2B companies slow sharply in March as clients freeze budgets for financial year-end. A flat monthly model misses these entirely.

Not Modelling Tax Outflows

Advance tax under Section 208 of the Income Tax Act, 1961 requires taxpayers with liability exceeding ₹10,000 to pay in four instalments (June 15, September 15, December 15, and March 15). Missing these in your cash flow model creates painful surprises. The Income Tax Department of India has increasingly automated penalty notices — cash flow planning is your best defence.

Over-Optimism in Revenue Assumptions

Hope is not a financial strategy. Build your base case on conservative assumptions, and treat the optimistic scenario as an upside bonus — not the plan.

Learn more about our Taxation & Compliance Services — ensuring your cash flow model is aligned with India’s advance tax, TDS, and GST payment cycles.

Financial Modelling for Cash Flow and Business Fundraising

If you are seeking equity investment, bank funding, or a government MSME scheme, your financial modelling for cash flow is the centrepiece of your pitch. Investors do not just want to see growth they want to see that you understand when cash moves, why it moves, and what you will do when it does not.

The team at Adwani and Company, led by Dr. Haresh Adwani, has supported hundreds of Indian businesses through fundraising exercises —from seed-stage startups to established family businesses seeking structured debt. In each case, the cash flow model was the difference between a credible pitch and a dismissed one.

Investors in India whether angel investors, venture capital firms, or private equity funds increasingly look for SEBI-compliant financial disclosures, MCA consistent corporate structuring, and GST-clean businesses. A model that integrates all these elements does not just present numbers; it presents a governance story.

Conclusion: Financial Modelling for Cash Flow Is a Business Imperative

Cash flow is the lifeblood of every business. It does not matter how strong your brand is, how talented your team is, or how promising your market is if cash runs dry, the business stops. Financial modelling for cash flow is not an exercise in spreadsheet complexity; it is an exercise in business survival, strategic clarity, and stakeholder confidence.

When done well, a financial model transforms the way you make decisions. It tells you when to hire and when to hold, when to invest and when to conserve, when to push growth and when to fortify your cash position. It gives you the language investors, banks, and regulators want to see and it gives you the confidence that comes from knowing your numbers, deeply and honestly.

As Dr. Haresh Adwani often says: “A business without a cash flow model is like a pilot flying without instruments the weather may be clear today, but you won’t see the storm coming until it’s too late.”

The good news is that professional financial modelling for cash flow is more accessible than ever and the right advisory partner can build, maintain, and update your model as your business evolves.

Frequently Asked Questions

1. What is financial modelling in simple terms?

Financial modelling for cash flow is the process of creating a structured, forward-looking spreadsheet or software model that predicts when money will enter and leave your business. Unlike a profit report, it shows you real-time liquidity the actual cash available in your bank account at any future point in time. For Indian businesses, it typically covers 13 weeks in detail and 12 to 36 months at a higher level.

2. Why do Indian business fail despite being profitable?

The most common reason is a timing mismatch between when revenue is earned and when cash is actually received. A business can show ₹50 lakh in profit for a quarter while having zero cash to pay salaries because its clients pay 90 days after invoice. Financial modelling for cash flow reveals and solves this gap before it becomes a crisis.

3. How does financial modelling help with GST and tax planning?

By integrating GST payment due dates (typically the 20th of each month) and advance tax instalments (June, September, December, March) directly into your cash flow model, you can ensure the business always has liquidity set aside for these obligations. Many businesses are caught off-guard by tax outflows; a model eliminates that surprise entirely. Adwani and Company specifically builds tax cycle alignment into every financial model it creates for clients.

4. What is 13-week (or quarterly) rolling cash flow model and do I need one?

A 13-week (or quarterly) rolling cash flow model is a week-by-week forecast of cash inflows and outflows for the next three months. It is the operational backbone of business finance. Banks and investors often request it during due diligence. For businesses facing rapid growth, seasonal swings, or debt obligations, a 13-week model is not optional it is essential.

5. How much does professional financial modelling cost in India?

The cost of a professionally built financial model varies based on business complexity, the number of revenue lines, and the level of scenario analysis required. At Adwani and Company, financial modelling services are offered as part of the Virtual CFO package or as standalone engagements — ensuring businesses of all sizes can access institutional-quality financial planning without needing a full-time CFO.

6. Can financial modelling improve my chances of getting a bank loan?

Absolutely. Banks in India particularly under the RBI’s updated MSME lending guidelines increasingly assess creditworthiness based on projected cash flows rather than collateral alone. A well-prepared financial model demonstrating healthy debt service coverage ratios (DSCR) and positive operating cash flow can significantly strengthen a loan application.

7. What are the most important cash flow ratios for business finance?

The three most critical ratios for business finance are:

(1) Operating Cash Flow Ratio — operating cash flow divided by current liabilities, indicating short-term liquidity;

(2) Cash Flow Margin — operating cash flow as a percentage of revenue, showing how efficiently the business converts sales into cash; and (3) Debt Service Coverage Ratio (DSCR) — net operating income divided by total debt service, which banks use to assess repayment capacity. A DSCR above 1.25x is generally considered healthy by Indian lenders.

About the Author

Dr. Haresh Adwani

Ph.D. in Commerce | Law Graduate | Managing Partner, Adwani & Co LLP Dr. Haresh Adwani holds a Ph.D. in Commerce and is a qualified Law graduate with over two decades of hands-on experience in GST advisory, direct taxation, and statutory compliance for businesses across Pune and Maharashtra. As Managing Partner of Adwani & Co LLP a firm established in 1977 by Advocate N. T. Adwani Dr. Adwani has guided hundreds of

SMEs, startups, and corporates through India’s evolving tax landscape. He is a recognised advisor on GST compliance, company formation, and Virtual CFO services, and regularly

contributes to professional seminars and industry forums in Pune.

Leave a Reply