By Dr. Haresh Adwani, PhD (Commerce), Law Graduate, Adwani and Company

You haven’t changed a single line of your trading strategy. Your win rate looks fine on paper. Yet something feels off your actual take-home profits are quietly shrinking. If this resonates with you, you are not alone, and the culprit may not be the market. The STT hike on trading profits introduced in the Union Budget 2024 is one of the most underreported yet financially significant changes affecting Indian F&O traders and equity investors today.

In this guide, Dr. Haresh Adwani of Adwani and Company walks you through exactly what changed, why it matters far more than most traders realise, and what smart money is already doing to adapt for STT calculation with latest rates,examplees,and tips to understand your real post trading discruption

+150%

Futures STT hike (0.02% → 0.05%)

+50%

Options STT hike (0.10% → 0.15%)

20%

Interest deduction cap on dividends

Capital Gains

Buybacks now taxed as CG, not dividend

What Is the STT Hike on Trading Profits and Why Should You Care?

Securities Transaction Tax (STT) is a small percentage levy charged on every buy or sell transaction on Indian stock exchanges. It is collected at source by the exchange and remitted directly to the government. According to the Income Tax Department of India, STT was introduced under Chapter VII of the Finance (No. 2) Act, 2004, to bring transparency to equity markets and reduce tax evasion.

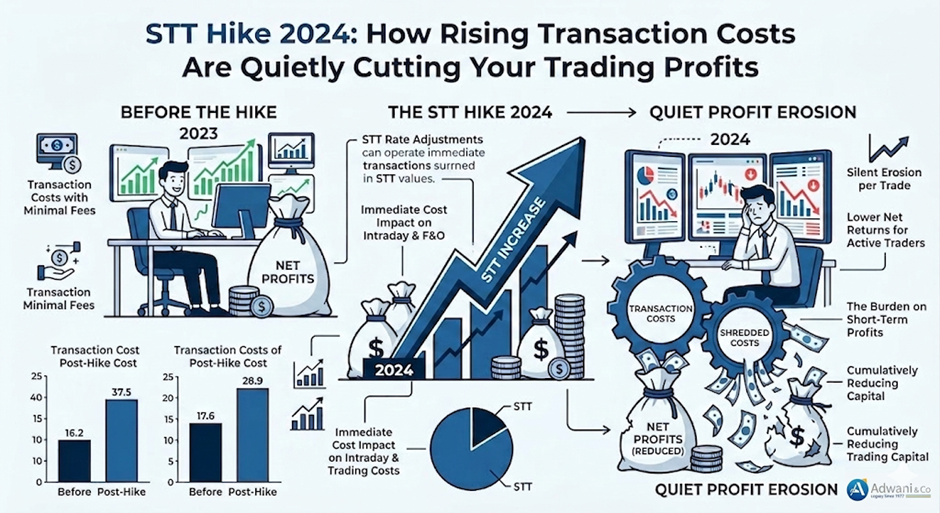

The Union Budget 2024 revised STT rates significantly. The STT hike on trading profits affects two critical segments:

| Segment | Old STT Rate | New STT Rate | % Increase |

| Futures (Sell side) | 0.0125% | 0.02% | +60% |

| Futures (on turnover) | 0.02% | 0.05% | +150% |

| Options (on premium) | 0.10% | 0.15% | +50% |

For a casual investor making a handful of trades per month, this might seem trivial. For an active F&O trader executing dozens of trades per day, the STT hike impact on trading costs is anything but small.

Key insight: STT is charged on the notional value of futures contracts and on the option premium not just your profit. That means you pay STT whether the trade made money or not.

Practical Example: How the STT Hike Drains F&O Trading Profits

Real Numerical ExampleScenario: An active Nifty Futures trader executes 10 round trips per day, with an average notional value of ₹15,00,000 per trade (1 lot Nifty Futures ~ ₹15 lakh notional).

Old STT per lot (sell side @ 0.02%): ₹15,00,000 × 0.02% = ₹300

New STT per lot (sell side @ 0.05%): ₹15,00,000 × 0.05% = ₹750

Extra STT per trade: ₹450

10 round trips/day × ₹450 × 22 trading days: = ₹99,000 extra per month

That is nearly ₹1.2 lakh in additional tax outgo per year from a single lot, trading conservatively. Scale this to a professional trader running multiple lots and strategies, and the STT hike on trading profits can easily erode ₹5–20 lakh annually.

This is the number that most traders miss when they review their P&L. As Dr. Haresh Adwani, with deep legal expertise in taxation, consistently advises clients: “Your gross returns are vanity. Your post-cost, post-tax returns are reality.”

Learn more about calculating your real post-tax trading returns.

https://www.adwaniandco.com/blog/share-trading-tax-business-income-or-capital-gains-2026

How Smart Traders Are Adapting Their Strategy After the STT Hike

The STT hike on trading profits is not a reason to exit the market. It is a reason to trade smarter. Here is what experienced traders and institutions are already doing:Factoring STT into minimum profit targets: Instead of targeting ₹500 per trade, smart traders now set net targets after accounting for STT, brokerage, GST, and SEBI fees.

- Reducing overtrading: More trades do not mean more profit. Post-STT hike, fewer, higher-conviction trades often produce better net P&L.

- Position sizing discipline: Larger positions magnify STT costs. Traders are now more disciplined about lot sizes relative to expected profit.

- Using spread strategies efficiently: Multi-leg strategies that reduce net premium exposure also reduce absolute STT outgo.

- Annual tax-loss harvesting: Working with a CA to book and set off losses before year-end to reduce the tax impact on profitable trades.

As Dr. Haresh Adwani frames it for clients at Adwani and Company: “Edge in trading is no longer just about entry and exit. In 2024 and beyond, it is equally about controlling costs and managing tax leakage. The traders who understand this will survive long-term. The rest will slowly bleed.”

Government Compliance: What Every Trader Must Know

The Ministry of Corporate Affairs (MCA) and the Income Tax Department have been systematically tightening compliance requirements for active market participants. Key compliance checkpoints include:

- F&O trading turnover must be computed correctly for tax audit applicability under Section 44AB of the Income Tax Act.

- Losses in F&O trading require filing ITR-3, not ITR-2. Incorrect ITR form can result in scrutiny or penalty.

- GST registration may be required if your brokerage income or trading-as-business turnover exceeds the threshold.

- STT paid is eligible for a rebate against your income tax liability in certain cases a benefit many traders miss.

The Income Tax Department of India regularly updates guidelines for speculative and non-speculative business income treatment of F&O profits and losses (incometax.gov.in). Staying updated with these is critical.

Read our detailed guide on ITR filing for F&O traders →https://www.adwaniandco.com/blog/fo-trading-taxation-in-india-2026-complete-simple-guide

Conclusion: The STT Hike Is a Behaviour Filter – Adapt Now

The STT hike on trading profits is not just a tax revision. It is the government’s way of filtering casual, high-frequency speculation from disciplined, informed trading. The traders and investors who understand this shift, adapt their cost structures, and plan their taxes proactively will continue to build wealth. Those who ignore it will see their edge slowly eroded not by bad trades, but by invisible costs. As Dr. Haresh Adwani, always emphasises to clients at Adwani and Company: “In the new tax environment, your CA is as important to your portfolio as your broker.” The most

successful investors combine market skill with tax intelligence and that combination is exactly what Adwani and Company delivers.

For further reference on official STT rates and compliance requirements, visit the Income Tax Department’s official portal at incometax.gov.in and the GST portal at gst.gov.in.

Is your trading strategy accounting for the new STT hike?

If you are trading F&O or investing actively and haven’t reviewed your real post-tax returns, now is the time. Connect with Adwani and Company led by Dr. Haresh Adwani, PhD (Commerce) and Law Graduate for personalised tax planning, ITR filing for traders, and compliance guidance that protects your profits.

Frequently Asked Questions

1. What is the STT hike on futures trading and when did it take effect?

The Securities Transaction Tax on futures was revised in Union Budget 2024, effective from October 1, 2024. The rate on the sell side of futures contracts increased from 0.02% to 0.05% of the notional value a 150% increase. This significantly increases the trading cost for active futures traders and directly impacts net trading profits.

2. How does the STT hike affect options traders specifically?

For options, the STT on the sell side increased from 0.10% to 0.15% of the option premium. For high-frequency options traders and those employing multi-leg strategies (straddles, spreads), this hike on trading costs is compounded across every leg of each strategy and across every expiry traded.

3. Can I claim STT as a deduction in my income tax return

Yes, in certain cases. If you are treating your trading as a business (non-speculative income in case of F&O), STT paid can be treated as a business expense and deducted from your gross trading income. However, if you are reporting F&O profits as capital gains (which is not the correct treatment per IT guidelines), the deduction rules differ. Consult a CA for accurate treatment specific to your profile.

4. Will the STT hike on trading affect long-term equity investors?

For long-term buy-and-hold investors, the direct STT impact is minimal since transactions are infrequent. However, the related changes such as buybacks being taxed as capital gains and the 20% cap on dividend interest deduction do affect equity investors’ post-tax returns

5. Is redemption of Sovereign Gold Bonds (SGBs) always tax-free?

No. Tax-free redemption at maturity is available only to original subscribers who purchased directly from the RBI during the issuance window and hold until the 8-year maturity date. If you bought SGBs from the secondary market (stock exchange), your redemption proceeds are subject to capital gains tax.

6. How should I adjust my F&O trading strategy to manage the STT hike impact?

Key adjustments include: recalibrating minimum profit targets to account for higher transaction costs, reducing unnecessary trades, employing tighter position sizing, using spread strategies to reduce net premium and thus absolute STT, and working with a qualified CA to optimise tax-loss harvesting and annual filings.

7. Which ITR form should F&O traders use to report income?

F&O income and loss must be reported under ITR-3 as business income (non-speculative). Filing under ITR-2 as capital gains is incorrect and can attract scrutiny. If total turnover exceeds ₹1 crore (or ₹10 crore in certain cases with cash turnover limits), a tax audit under Section 44AB is mandatory.

Dr. Haresh Adwani holds a PhD in Commerce and brings over 20 years of expertise in GST compliance, income tax advisory, FEMA, and corporate law. Services include GST audit, ITR filing, GST appeal representation, notice response, NRI taxation, and FEMA compliance.

Leave a Reply