Introduction: One Deadline That Affects Every Taxpayer in India

Every year, millions of Indian taxpayers face the same situation: the last week of July arrives, panic sets in, documents go missing, and a return that could have been filed optimally ends up being filed in a hurry with mistakes, missed deductions, and unnecessary penalties.

ITR filing for FY 2025-26 (Assessment Year 2026-27) is your annual opportunity to do this right. Not just to meet a compliance obligation, but to claim every deduction you are entitled to, report your income accurately, and build the financial credibility that banks, visa authorities, and financial institutions increasingly rely on.

This comprehensive guide by Adwani and Company walks you through every dimension of income tax return filing for FY 2025-26 the deadlines, the forms, the rules, the penalties, and the strategies that distinguish a smart, optimized filing from a last-minute scramble.

Why ITR Filing 2026 Is No Longer Optional

Filing your income tax return 2026 is not simply about paying tax. It is about building your financial identity, maintaining compliance, and protecting yourself legally. Here is why the ITR filing last date 2026 must be on every taxpayer’s calendar.

1. Your ITR Is Now Your Financial Identity Document

Banks, NBFCs, housing finance companies, and visa consulates treat your filed ITR as primary proof of income. Whether you are applying for a home loan, personal loan, car loan, or a US/UK/Schengen visa, a missing or inconsistent ITR history is a direct red flag.

According to guidelines from the Income Tax Department of India (incometax.gov.in), taxpayers who maintain a consistent filing record with accurate disclosures face significantly lower scrutiny probability.

2. The Government Now Tracks Most Financial Transactions

The Annual Information Statement (AIS) collects financial data from multiple sources, including:

- Banks

- Mutual funds

- Stockbrokers

- Credit card companies

- Property registrars

- GST portals

This means many of your financial transactions are already visible to the Income Tax Department before you file your return.

Why AIS Reconciliation Matters

If the income shown in your ITR does not match your AIS data:

- refund delays may occur

- notices may be generated

- additional tax scrutiny may arise

As Dr. Haresh Adwani explains:

“AIS mismatches are now one of the most common triggers for scrutiny notices.”As Dr. Haresh Adwani, Managing Partner of Adwani and Company, explains: “If you have even ₹50,000 in unexplained income that appears in the AIS but not in your ITR, you are not evading scrutiny you are inviting it. The AIS-ITR mismatch detection system is fully automated in 2026.”

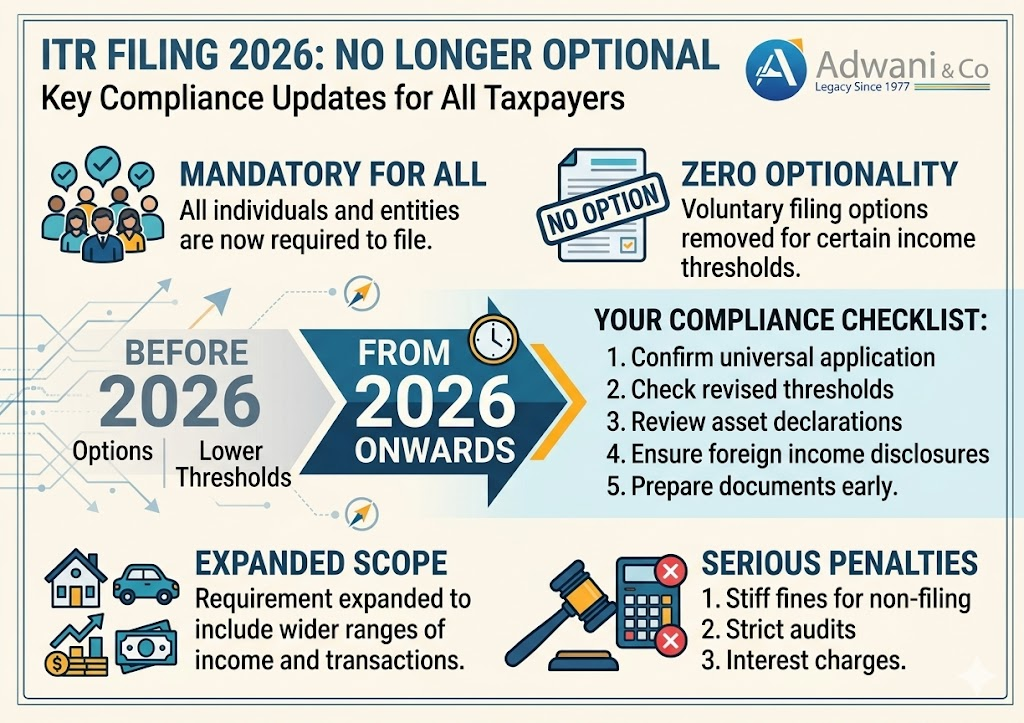

3. Mandatory Filing Regardless of Income Level

Under updated CBDT rules, ITR filing 2026 is legally mandatory even if your income is below the basic exemption limit, if you meet any of these conditions:

- Deposited more than ₹1 crore in bank accounts during FY 2025-26

- Spent more than ₹2 lakh on foreign travel

- Electricity bills exceeded ₹1 lakh in the year

- Have foreign assets or income of any amount

- Received TDS/TCS deductions above ₹25,000 (₹50,000 for senior citizens)

- Business turnover exceeded ₹60 lakh or professional receipts exceeded ₹10 lakh

- F&O trading losses: carry-forward requires timely ITR filing

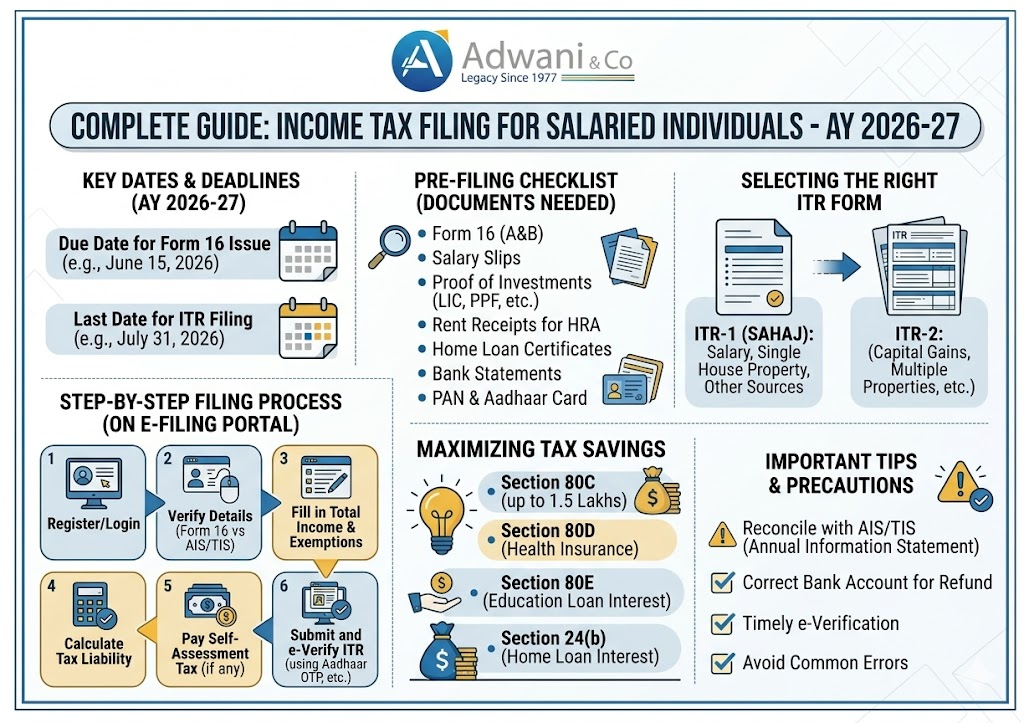

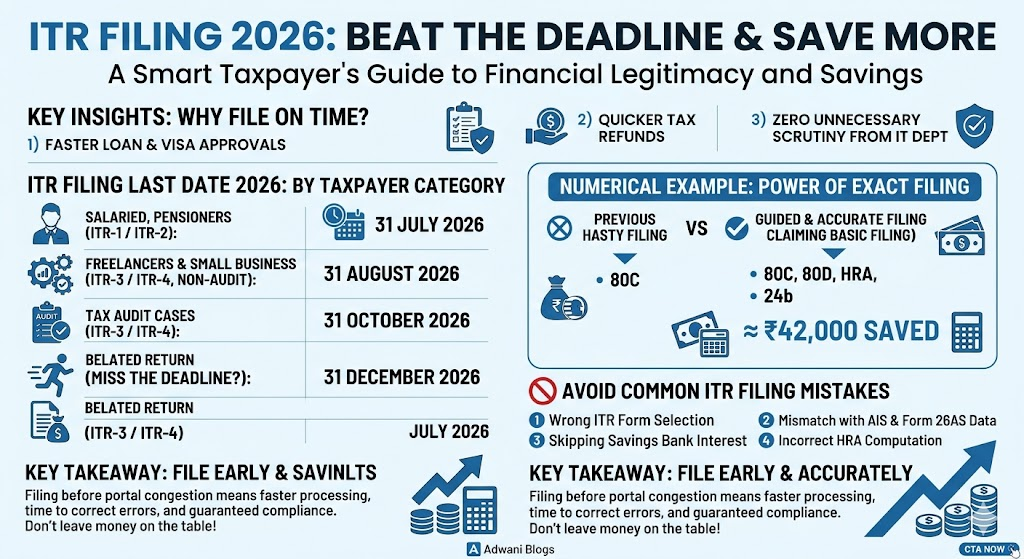

ITR Filing Last Date 2026 Category-Wise Deadlines

Budget 2026 formally bifurcated the ITR filing deadline 2026 by taxpayer category. Missing your deadline has direct financial consequences this table is critical.

| Taxpayer Category | ITR Form | Filing Deadline 2026 |

| Salaried employees & pensioners | ITR-1 / ITR-2 | 31 July 2026 |

| Freelancers, consultants (non-audit) | ITR-3 / ITR-4 | 31 August 2026 |

| Businesses requiring audit (Section 44AB) | ITR-3 / ITR-4 | 31 October 2026 |

| Belated ITR (missed original deadline) | All applicable | 31 December 2026 |

| Revised ITR for AY 2026-27 | All applicable | 31 March 2027 |

| Updated Return under Section 139(8A) | ITR-U | 31 March 2031 |

| ⚠ KEY UPDATE: Budget 2026 extended the Updated Return (ITR-U) under Section 139(8A) to 4 years (48 months) giving taxpayers a wider window to correct unreported income without facing full scrutiny. |

Choosing the Right ITR Form for AY 2026-27

Filing with the wrong ITR form results in a defective return notice forcing you to refile from scratch, often after the deadline. Here is how to choose correctly for ITR filing 2026:

| Form | Who Should File | Key Condition |

| ITR-1 | Salaried individuals, one house property, income ≤ ₹50 lakh | No capital gains, no business income |

| ITR-2 | Salary + capital gains, more than one property, NRIs | No business/professional income |

| ITR-3 | Business/professional income, F&O traders | Must maintain books of accounts |

| ITR-4 | Presumptive income under Section 44AD/44ADA/44AE | Turnover ≤ ₹2 crore (business), ₹75 lakh (professional) |

New Tax Regime vs Old Tax Regime: Which Is Better?

One of the most important decisions while filing your income tax return for AY 2026-27 is choosing between the new and old tax regimes. You can switch between regimes every year if you are a salaried individual but this choice must be made before filing.

| Factor | New Tax Regime 2026 | Old Tax Regime |

| Basic exemption | ₹3,00,000 | ₹2,50,000 |

| Section 80C deductions | Not available | Up to ₹1.5 lakh |

| HRA exemption | Not available | Claimable |

| Section 80D (Health Insurance) | Not available | Up to ₹75,000 |

| Section 24(b) Home Loan Interest | Not available (except let-out property) | Up to ₹2 lakh |

| Standard deduction | ₹75,000 | ₹50,000 |

| Best suited for | Lower income or minimal investments | High deduction claims |

Dr. Haresh Adwani advises clients that the new tax regime is not automatically beneficial for every taxpayer. Individuals with significant deductions under Section 80C, home loan interest, HRA exemptions, and health insurance premiums often save more under the old regime.Key Tax Saving Investments and Deductions for ITR Filing 2026

If you opt for the old tax regime, these tax saving investments 2026 can significantly reduce your tax liability. Missing even one can cost thousands.

Section 80C Deductions 2026 Up to ₹1.5 Lakh

- Public Provident Fund (PPF) contributions

- Employee Provident Fund (EPF) employee share

- National Savings Certificate (NSC)

- ELSS (Equity Linked Savings Scheme) mutual funds

- Life insurance premium payments

- Principal repayment on home loan

- Sukanya Samriddhi Yojana contributions

- 5-year fixed deposits with scheduled banks

- Tuition fees for children (up to 2 children)

Additional Deductions Beyond Section 80C

- Section 80D: Health insurance premium ₹25,000 (self/family) + ₹50,000 (senior citizen parents) = ₹75,000 maximum

- Section 80CCD(1B): NPS additional contribution ₹50,000 over and above 80C limit

- Section 24(b): Home loan interest up to ₹2 lakh per year on self-occupied property

- Section 80E: Education loan interest full deduction for up to 8 years

- Section 80G: Donations to specified funds and charitable organizations

- Section 80TTA/80TTB: Interest on savings accounts ₹10,000 (general) / ₹50,000 (senior citizens)

- HRA Exemption: Calculated as minimum of: actual HRA received, 50% or 40% of basic salary, actual rent paid minus 10% of basic

For a complete review of all available deductions for your specific income profile, Read our detailed guide on Tax Saving Strategies for Salaried Employees 2026.

Real Example: How ITR Filing 2026 Saved ₹78,500 in Tax

Rahul Mehta, a 42-year-old software engineer in Pune earning ₹16.8 lakh annually, had self-filed his ITR for five consecutive years claiming only the standard deduction and Section 80C (₹1.5 lakh). When he approached Adwani and Company for ITR filing 2026, Dr. Haresh Adwani’s team conducted a comprehensive deduction audit:

| Deduction / Exemption | Previously Claimed | Correctly Claimed | Difference |

| Section 80C | ₹1,50,000 | ₹1,50,000 | — |

| Section 80D (Health Insurance self + parents) | ₹0 | ₹75,000 | +₹75,000 |

| HRA Exemption (recalculated correctly) | ₹60,000 | ₹1,26,000 | +₹66,000 |

| Section 80CCD(1B) NPS | ₹0 | ₹50,000 | +₹50,000 |

| Section 80E Education Loan Interest | ₹0 | ₹42,000 | +₹42,000 |

| Section 80TTA Savings Interest | ₹0 | ₹10,000 | +₹10,000 |

| Total Additional Deductions Unlocked | ₹2,43,000 |

| Result: At the applicable 30% tax slab rate, these additional deductions generated a verified tax saving of ₹78,500 compared to Rahul’s self-filed return. He had been overpaying taxes for five years. Cumulative overpayment: conservatively over ₹3.5 lakh. |

This example shows how professional tax planning can help taxpayers identify deductions they may otherwise miss

Section 234F Penalty 2026 The Real Cost of Missing the Deadline

Missing the ITR filing last date 2026 is not just an administrative oversight. Under Section 234F of the Income Tax Act, 1961, the penalties are fixed and unavoidable:

| Total Income | Late Filing Fee | Section 234A Interest |

| Below ₹5 lakh | ₹1,000 (flat) | 1% per month on tax due |

| Above ₹5 lakh | ₹5,000 (flat) | 1% per month on tax due |

| Example: ₹60,000 tax due, filed 4 months late | ₹5,000 penalty | +₹2,400 interest = ₹7,400 extra cost |

Additionally, if you missed filing capital loss carry-forward from F&O trading or equity transactions, you permanently lose that carry-forward benefit potentially costing lakhs in future tax offsetting opportunities.

How to File ITR Online 2026 Step-by-Step

Filing on the Income Tax e-filing portal is straightforward if you follow the right sequence. Rushing without preparation is where errors happen.

- Gather documents before you begin: Form 16, Form 26AS, Annual Information Statement (AIS), bank statements (April 2025–March 2026), capital gains statements (CAMS/KFintech), home loan interest certificate, health insurance receipts, investment proofs

- Download and review AIS: Log into incometax.gov.in → AIS → download and reconcile every entry. Flag incorrect entries before filing.

- Choose correct ITR form: Use the table above filing with the wrong form triggers a defective return notice.

- Compare tax regimes: Compute tax liability under both new and old tax regime 2026 before selecting. This single step can save ₹10,000–₹80,000+ for high-deduction taxpayers.

- Fill ITR form with AIS-reconciled data: Do not rely solely on Form 16 your AIS may include additional income sources.

- E-file and e-verify within 30 days: Use Aadhaar OTP, net banking, or pre-validated bank account. Unverified returns are treated as non-filed.

- Track your refund: Check refund status at incometax.gov.in under ‘My Account → Refund/Demand Status’. Early July filers typically see refunds within 15–21 days.

For advance tax payment 2026: if your estimated tax liability exceeds ₹10,000, you must pay advance tax in four installments (15% by June 15, 45% by September 15, 75% by December 15, 100% by March 15). Shortfall attracts Section 234B and 234C interest

ITR Filing 2026 for Freelancers, Self-Employed & Small Businesses

The ITR filing last date 2026 for freelancers is 31 August 2026 a new one-month extension introduced by Budget 2026 for non-audit professional income cases.

Freelancers and self-employed professionals must pay special attention to:

- Reporting all income: including cash payments, international client transfers, and platform-based income from apps

- Section 44ADA presumptive taxation: 50% of gross professional receipts treated as net income for eligible professionals with receipts below ₹75 lakh dramatically simplifying compliance

- Form 26AS TDS reconciliation: all client TDS deductions under Section 194J must match

- ITR-3 or ITR-4 selection: depending on whether presumptive scheme is adopted

- Advance tax: mandatory in four installments if estimated tax liability exceeds ₹10,000

- GST-ITR consistency: turnover declared in GSTR-3B must align with income declared in ITR

Small businesses and GST-registered entities should cross-verify their GSTR-3B filing 2026 turnover against ITR income to avoid mismatches. The Income Tax Department cross-references both filings automatically.

Trusted Government Sources for ITR Filing 2026 Guidance

For authoritative, up-to-date information on ITR filing 2026, always refer to official government sources:

- Income Tax Department of India incometax.gov.in: Official portal for ITR filing, AIS/Form 26AS download, refund tracking, e-verification, and all CBDT notifications

- Ministry of Finance, Government of India: Budget 2026 tax amendments, new tax regime 2026 slabs, Section 139(8A) updated return provisions, and official press releases on compliance deadlines

Dr. Haresh Adwani and the team at Adwani and Company monitor all CBDT circulars and income tax notifications in real time, ensuring clients always receive advice aligned with current law not last year’s rules.

Conclusion: File Smart, File Early, File Right in 2026

Your ITR filing 2026 is far more than an annual compliance box to tick. It is your proof of income to every bank and lender, your credibility document for visa officers across the world, your legal protection against scrutiny notices, and your only route to recovering overpaid taxes and carrying forward investment losses.

The ITR filing last date 2026 is 31 July for salaried taxpayers and 31 August for freelancers and small businesses. The penalties for delay are real. The cost of an inaccurate return as Rahul Mehta’s story shows can run to ₹78,500 or more in a single year.

With the new tax regime 2026, extended AIS monitoring, tighter GST-ITR cross-checking, and expanded Updated Return windows, the complexity of income tax return filing 2026 has never been higher. The smartest thing you can do is file early, file accurately, and file with professionals who understand that your ITR is not paperwork it is your financial identity.

Filing your return correctly can save far more than just penalties it can help you maximize deductions, avoid notices, and build long-term financial credibility.

Whether you are a salaried employee, freelancer, business owner, investor, or NRI, Adwani and Company can help you file accurately and tax-efficiently.

Q1. What is the ITR filing last date 2026 for salaried employees?

The ITR filing last date 2026 for salaried employees is 31 July 2026, as confirmed by the Central Board of Direct Taxes (CBDT). Freelancers and non-audit business filers have until 31 August 2026. If you miss the original deadline, a belated ITR can be filed up to 31 December 2026 with applicable Section 234F late fees.

Q2. Is ITR filing 2026 mandatory if my income is below the taxable limit?

Yes, ITR filing 2026 is mandatory even if your income is below the basic exemption limit if you meet any of the CBDT’s specified high-value transaction criteria such as bank deposits exceeding ₹1 crore, foreign travel above ₹2 lakh, electricity bills above ₹1 lakh, or TDS/TCS received above ₹25,000. Additionally, filing is essential to claim refunds, carry forward capital losses, and maintain financial credibility for loans and visas.

Q3. Which is better for ITR filing 2026 new tax regime or old tax regime?

The new tax regime 2026 offers lower slab rates but eliminates most deductions including Section 80C, HRA, and home loan interest. The old regime suits taxpayers with significant deduction claims. A comparison must be computed individually for someone claiming ₹3.5 lakh in deductions at a 30% slab, the old regime typically saves ₹70,000–₹1.05 lakh annually. Adwani and Company computes this comparison for every client before filing.

Q4. What is the Section 234F penalty for late ITR filing 2026?

Under Section 234F, a flat late filing fee of ₹1,000 applies if total income is below ₹5 lakh, and ₹5,000 if total income exceeds ₹5 lakh. Additionally, Section 234A charges 1% interest per month on any outstanding tax from the original due date. Beyond financial penalties, late filers also permanently lose the ability to carry forward business losses and capital losses.

Q5. What documents do I need for ITR filing 2026?

Key documents for ITR filing 2026 include: Form 16 (from all employers), Form 26AS and AIS from the Income Tax portal, bank statements for all accounts (April 2025–March 2026), capital gains statements from mutual funds (CAMS/KFintech) and stockbrokers, home loan interest certificate, health insurance premium receipts, Section 80C investment proofs, rental receipts if claiming HRA, and details of any foreign assets or income.

Q6. Can I revise my ITR after filing for AY 2026-27?

Yes. Budget 2026 extended the revised ITR window to 31 March 2027 for AY 2026-27, giving taxpayers an unprecedented correction window. Additionally, the Updated Return under Section 139(8A) is now available for up to 4 years (48 months) from the end of the relevant assessment year, allowing voluntary disclosure of omitted income with a reduced penalty structure.