Every year, millions of salaried employees across India face the same question: “Have I filed my income tax return correctly?” With Assessment Year 2025-26 upon us, navigating new regime defaults, updated standard deductions, and evolving ITR forms makes income tax filing for salaried individuals more consequential than ever. This guide cuts through the complexity giving you everything you need to file accurately, on time, and with complete confidence.

Why Income Tax Filing for Salaried Individuals Matters More Than Ever

Many salaried employees assume their employer’s TDS settlement is the end of the story. It is not. Income tax filing for salaried individuals in AY 2025-26 is a legal obligation under Section 139(1) of the Income Tax Act, 1961 if your gross total income exceeds the basic exemption limit. More importantly, filing your ITR unlocks refunds, validates creditworthiness for home loans and visa applications, and protects you from late-filing penalties of up to Rs 5,000 under Section 234F.

At Adwani and Company a legacy CA firm serving clients since 1977 — we see thousands of salaried professionals make avoidable mistakes each Assessment Year. Missing an income source, choosing the wrong ITR form, or overlooking eligible deductions costs taxpayers crores of rupees in excess taxes paid or penalties levied.

In this comprehensive income tax filing guide, Dr. Haresh Adwani PhD holder in Commerce and qualified law graduate walks you through every step of the AY 2025-26 income tax return process, from choosing the correct ITR form to claiming every deduction legally available to you.

Understanding AY 2025-26: Key Changes for Income Tax Filing

The Assessment Year 2025-26 covers income earned in the Previous Year 2024-25 (April 1, 2024 to March 31, 2025). Several significant changes affect income tax filing for salaried individuals this year:

- New Regime Remains Default: The new tax regime continues as the default under Section 115BAC. You must actively opt for the old regime to claim deductions like 80C, 80D, and HRA.

- Enhanced Standard Deduction: Under the new tax regime, the standard deduction was increased to Rs 75,000 in Union Budget 2024 (from Rs 50,000). Under the old regime, it remains Rs 50,000.

- Rebate Under Section 87A: For new regime filers, income up to Rs 7 lakh attracts zero tax liability due to the rebate. This limit remains Rs 5 lakh under the old regime.

- Annual Information Statement (AIS): The Income Tax Department now captures near-complete financial data through AIS, making it essential to reconcile before filing.

Which ITR Form is Right for Income Tax Filing for Salaried Individuals?

Choosing the correct ITR form is one of the most misunderstood aspects of income tax filing for salaried individuals. Filing the wrong form means your return is treated as defective by the department. Here is how ITR forms are categorised for salaried taxpayers in AY 2025-26:

- ITR-1 (Sahaj): For salaried individuals with total income up to Rs 50 lakh from salary, one house property, and other sources only. Business or capital gains income is NOT permitted.

- ITR-2: For salaried individuals with capital gains from mutual funds, stocks or property, multiple house properties, or foreign assets and income. This is mandatory if you sold equity shares or redeemed mutual funds in FY 2024-25.

- ITR-3: Required if you have both salary income and income from business or profession, including freelance or consultancy work.

- ITR-4 (Sugam): For those opting for presumptive taxation under Sections 44AD, 44ADA, or 44AE along with salary income.

As Dr. Haresh Adwani advises clients at Adwani and Company: the ITR form is the foundation of your income tax return. An error here invalidates the entire filing. Learn more about our comprehensive income tax filing services to ensure you always start on the right form.

Essential Documents for Income Tax Filing in AY 2025-26

Organised documentation is the backbone of stress-free income tax filing for salaried individuals. Collect these before logging into the Income Tax portal:

- Form 16 Part A and Part B from your employer (issued by July 15, 2025)

- Form 26AS and Annual Information Statement (AIS) from TRACES portal

- Salary slips for April 2024 through March 2025

- Bank statements for all accounts including savings, FD, and RD

- Investment proofs: ELSS receipts, PPF passbook, LIC premium certificates

- Home loan interest certificate for Section 24(b) deduction under old regime

- Rent receipts and employer HRA declaration if claiming House Rent Allowance

- Medical insurance premium receipts for Section 80D claims

- Capital gains statements from your stockbroker or mutual fund platform

- PAN card, Aadhaar card, and pre-validated bank account details

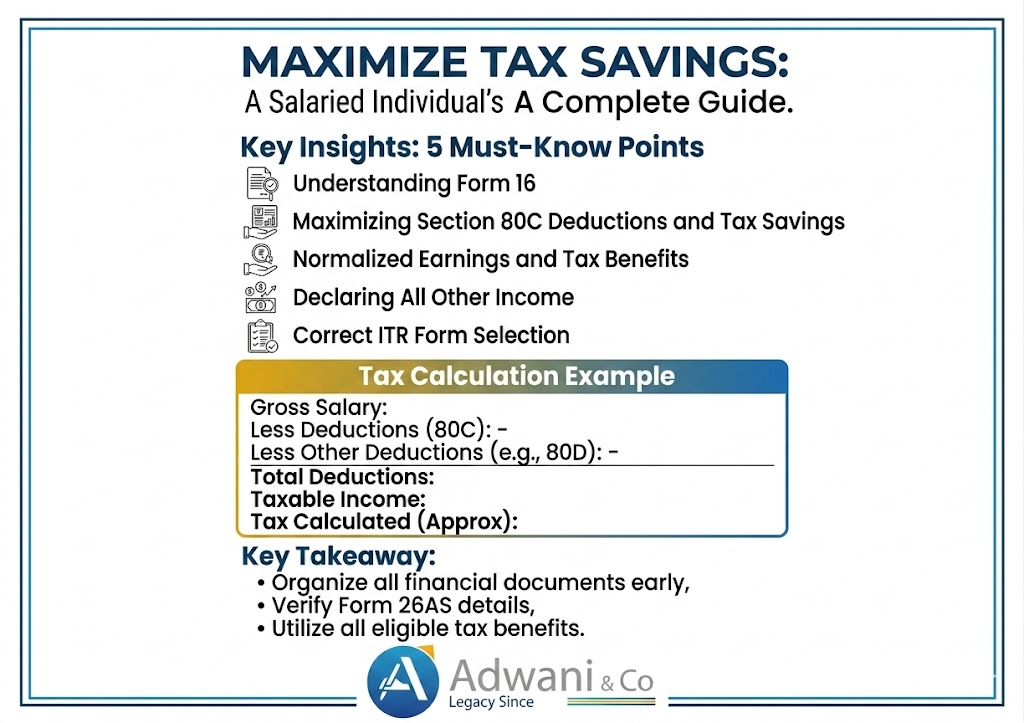

Old Regime vs New Regime: The Most Critical Decision in Income Tax Filing

For income tax filing for salaried individuals in AY 2025-26, the regime choice is the single most impactful financial decision. There is no universally correct answer — it depends on your income level, investments, and specific deductions available to you.

Practical Example: Old Regime vs New Regime (FY 2024-25)

| Particulars | Old Regime (Rs) | New Regime (Rs) |

|---|---|---|

| Gross Salary | 12,00,000 | 12,00,000 |

| Standard Deduction | 50,000 | 75,000 |

| Section 80C (ELSS + PPF) | 1,50,000 | Not applicable |

| Section 80D (Health Insurance) | 25,000 | Not applicable |

| HRA Exemption | 84,000 | Not applicable |

| Net Taxable Income | 8,91,000 | 11,25,000 |

| Approximate Tax (incl. 4% cess) | Rs 82,524 | Rs 65,000 approx. |

Key Insight: In this example the new regime results in lower tax despite a higher taxable income, because the slab rates are significantly reduced. However, this balance shifts if you have higher deductions — particularly for those with home loans or large 80C investments.

Dr. Haresh Adwani’s Rule of Thumb: If your total deductions under the old regime (80C + 80D + HRA + home loan interest) exceed Rs 3.75 lakh for a salary of Rs 12 lakh, the old regime likely benefits you more. Always calculate both before finalising your income tax filing for AY 2025-26.

Section 80C and Key Deductions: Maximising Income Tax Savings

Under the old regime, income tax filing for salaried individuals opens the door to a wide range of deductions. These are the cornerstone of strategic income tax planning:

Section 80C: Up to Rs 1.5 Lakh Deduction

Section 80C allows deductions for PPF contributions, ELSS mutual fund investments, NSC, 5-year tax-saving FDs, life insurance premiums, ULIP, tuition fees for two children, and home loan principal repayment. This is the most important deduction in income tax filing for salaried individuals and should be fully utilised every year.

Section 80D: Medical Insurance Deduction

Premiums paid for health insurance for self, spouse, and children attract a deduction up to Rs 25,000 per year. An additional Rs 25,000 (Rs 50,000 for senior citizen parents) is available for parents’ health insurance. This is a deduction many salaried employees forget to include during income tax filing.

Section 24(b): Home Loan Interest Deduction

If you have a home loan, interest paid up to Rs 2 lakh on a self-occupied property is deductible under the old regime. For a let-out property, there is no upper cap on interest deduction, making income tax filing even more advantageous for property investors. Read our detailed guide on home loan tax benefits for salaried individuals for a complete breakdown.

Section 80TTA and 80TTB: Interest Income Deduction

Under Section 80TTA, savings bank interest up to Rs 10,000 is exempt. Senior citizens enjoy a higher limit of Rs 50,000 under Section 80TTB, covering both savings account interest and fixed deposit interest. These are commonly overlooked deductions in income tax filing for salaried individuals.

Step-by-Step: How to File Income Tax Return for Salaried Individuals

- Gather All Documents: Collect Form 16, bank statements, investment proofs, and all income statements well before the July 31 deadline.

2. Verify AIS and Form 26AS: Log into the Income Tax portal. Cross-check your Annual Information Statement for all income, TDS, and high-value transactions.

3. Choose Your Tax Regime: Calculate tax liability under both old and new regimes. Select the one that results in a lower net tax payment for AY 2025-26.

4. Select the Correct ITR Form: Based on your income sources ITR-1 for simple salary, ITR-2 for capital gains, ITR-3 for business income alongside salary.

5. Fill Income and Deductions: Enter salary details from Form 16, compute eligible deductions, reconcile TDS deducted, and verify pre-filled data from AIS.

6. Pay Self-Assessment Tax: If tax payable exceeds TDS already deducted, pay the balance via Challan 280 at the NSDL portal before submitting your ITR.

7. File and E-Verify Immediately: Submit your return and e-verify within 30 days using Aadhaar OTP, net banking, or demat account. Unverified returns are invalid.

8. Track Your Refund: Monitor ITR processing status on the Income Tax portal. Refunds are typically credited

Common Mistakes in Income Tax Filing for Salaried Individuals

Drawing from over four decades of practice, Dr. Haresh Adwani and the team at Adwani and Company identify these as the most frequent and costly errors during income tax filing for salaried individuals:

- Not reporting interest income from savings accounts, fixed deposits, or recurring deposits all taxable under income from other sources

- Claiming HRA deduction without proper rent receipts or landlord PAN (mandatory if monthly rent exceeds Rs 8,333)

- Ignoring capital gains from mutual fund redemptions or equity share sales — now visible in AIS and easily cross-checked by the department

- Overlooking salary from a previous employer when you changed jobs during FY 2024-25 both Form 16 certificates must be consolidated

- Failing to reconcile Form 26AS with actual TDS deducted, leading to mismatched returns and subsequent notices

- Choosing the wrong ITR form and receiving a defective return notice requiring revised filing

- Forgetting to e-verify the return within 30 days of filing, rendering the entire submission invalid

- Not disclosing foreign assets or RRSP accounts if you are an NRI or returning resident with overseas investments

Income Tax Department Alert: The Income Tax Department of India has significantly enhanced its data matching capabilities through AIS. Income reported in your ITR is cross-verified against information from banks, mutual funds, registrars, and employers. Discrepancies trigger automated notices under Section 143(1) or scrutiny under Section 143(2). Accurate income tax filing for salaried individuals has never been more important.

Income Tax Deadlines for AY 2025-26: Key Dates for Salaried Individuals

Critical Deadlines : Do Not Miss:

July 15, 2025 : Last date for employers to issue Form 16

July 31, 2025 : Last date for income tax filing for salaried individuals (non-audit cases) PRIMARY DEADLINE

October 31, 2025 : Due date for audit cases and partners in firms requiring tax audit

December 31, 2025 : Last date for belated return filing (with penalty under Section 234F)

March 31, 2026 : Last date for revised return if corrections are needed after original filing

A belated income tax return filed after July 31 but before December 31, 2025 attracts a late fee: Rs 1,000 if total income is below Rs 5 lakh, and Rs 5,000 for all others. Additionally, interest under Section 234A applies on the outstanding tax amount from the original due date.

How Adwani and Company Simplifies Income Tax Filing for Salaried Individuals

Since 1977, Adwani and Company has guided thousands of salaried professionals, executives, business owners, and NRIs through every aspect of the income tax filing process. Led by Dr. Haresh Adwani — a PhD holder in Commerce and a law graduate with deep legal expertise — the firm brings an unmatched combination of technical tax knowledge and personalised service.

Our dedicated team for AY 2025-26 income tax filing offers: complete document review, old vs new regime comparison analysis, ITR form selection, deduction optimisation, return preparation, e-filing, and comprehensive post-filing support including handling scrutiny notices and departmental queries. Our practice is registered with the Ministry of Corporate Affairs and maintains full compliance with GST Network regulations for all our clients.

Conclusion

Income tax filing for salaried individuals in AY 2025-26 is far more than a compliance formality it is a financial act that shapes your creditworthiness, refund eligibility, investment planning, and long-term wealth. With the dual-regime system firmly in place, enhanced standard deductions, improved AIS reporting, and stringent deadline enforcement, the stakes for getting your income tax filing right have never been higher.

The core advice remains constant: start early, gather all documents before June, compare both tax regimes carefully, choose the right ITR form, claim every legitimate deduction available under your chosen regime, and e-verify your return immediately after submission. If complexity arises multiple employers, capital gains, foreign assets, or home loan deductions professional guidance is not merely convenient, it is essential for error-free income tax filing.

Dr. Haresh Adwani and the expert team at Adwani and Company have navigated India’s evolving tax landscape with distinction since 1977. Their depth of knowledge — spanning income tax law, corporate compliance, GST advisory, and financial planning makes Adwani and Company the trusted partner for accurate, timely, and optimised income tax filing for salaried individuals across India.

Frequently Asked Questions

Q1. What is the last date for income tax filing for salaried individuals in AY 2025-26?

The due date for income tax filing for salaried individuals in AY 2025-26 is July 31, 2025. Filing after this date without an extension attracts a late fee under Section 234F of Rs 1,000 (income below Rs 5 lakh) or Rs 5,000 (income above Rs 5 lakh). A belated return can still be filed until December 31, 2025.

Q2. Which ITR form should I use as a salaried employee for AY 2025-26?

Most salaried individuals with income below Rs 50 lakh from salary and one house property should file ITR-1 (Sahaj). If you have capital gains from stocks or mutual funds, use ITR-2. If you have freelance or business income in addition to salary, ITR-3 is mandatory. The Income Tax portal offers a guided tool to select the correct form based on your income profile.

Q3. Can I switch between the old and new tax regime every year during income tax filing?

es. Salaried individuals without business income have complete flexibility to choose between the old and new tax regimes at the time of filing their income tax return each year. However, if you have business income, switching back to the old regime after opting out is significantly restricted. Inform your employer of your regime preference at the start of each financial year for correct TDS computation.

Q4. Is income tax filing mandatory even if my employer has already deducted TDS?

Yes. TDS deducted by your employer does not replace your obligation to file an income tax return. Under Section 139(1), income tax filing for salaried individuals is mandatory if gross income exceeds the basic exemption limit Rs 3 lakh under the new regime and Rs 2.5 lakh under the old regime. Filing is also essential to claim tax refunds, carry forward capital losses, and maintain a clean tax compliance record.

Q5. What is Form 16 and why is it the most important document for ITR filing?

Form 16 is a TDS certificate issued by your employer under Section 203 of the Income Tax Act. Part A contains a summary of quarterly TDS deducted and deposited with the government. Part B provides a detailed salary break-up including allowances, perquisites, and deductions declared by you. It is the primary input document for income tax filing for salaried individuals and must be obtained from your employer before filing your ITR.

Q6. How do I claim an income tax refund for excess TDS deducted?

If your actual income tax liability is lower than TDS deducted by your employer (for example, due to investments not declared to the employer or a regime switch at filing time), the excess amount will be refunded by the Income Tax Department directly to your registered bank account. Ensure your bank account is pre-validated and linked to your PAN on the portal before filing your income tax return for AY 2025-26.

Q7. Can I still file my income tax return after the July 31 deadline?

Yes. A belated income tax return can be filed until December 31, 2025 for AY 2025-26. However, this attracts a late fee under Section 234F (Rs 1,000 to Rs 5,000), interest under Section 234A on unpaid taxes, and the loss of the right to carry forward certain capital losses. A revised return, to correct errors in the original filing, can be submitted until March 31, 2026.

Dr. Haresh Adwani

PhD – Commerce | Law Graduate

Founder and Senior Partner, Adwani and Company. Over 40 years of expertise in income tax, corporate law, GST, and financial advisory.