Business Valuation vs ESOP 409A Valuation

You have just closed a Series A round. Investors valued your company at $8 million. Your legal counsel says it’s time to set up an ESOP pool for the team. And then someone in the room says: “The company is valued at $8 million with 800,000 shares so the ESOP exercise price is $10 per share, right?”

Wrong. And this particular misconception that a business valuation and an ESOP 409A valuation are the same exercise is one of the most consequential errors founders and early-stage finance teams make. In the US, getting it wrong can trigger IRS penalties under Section 409A for every employee who receives a stock option grant. In India, it leads to incorrect Ind AS 102 disclosures and potential SEBI ESOP compliance issues.

The two valuations look similar on the surface. They both involve valuing a company. But they answer different questions, use different analytical processes, and produce different outputs and confusing one for the other is not just a technical error, it is a regulatory risk.

The Core Distinction: What Question Is the Valuation Answering?

Start with purpose. Every valuation begins with a question. The answer to that question and the methodology chosen must follow from it.

A business valuation asks: what is this company worth as a whole, today, to a rational buyer, investor, or shareholder?

An ESOP 409A valuation asks something narrower: what is one common share of this company worth today, specifically so that employee stock options can be granted at the correct exercise price?

These are not the same question. And because they are not the same question, they cannot produce the same answer particularly in a startup with multiple share classes, investor preferences, and a complex capitalisation table.

Business Valuation: Determining What the Company Is Worth

A business valuation establishes the aggregate value of the company its enterprise value or total equity value across all share classes. It is the starting point for informed decision-making in:

- Fundraising rounds : providing the valuation basis against which investors subscribe for shares

- Mergers and acquisitions : establishing a reference price for negotiation and due diligence

- Strategic investments and secondary transactions

- Regulatory filings under SEBI, RBI/FEMA, or MCA where a formal valuation certificate is required

- Shareholder buy-sell agreements and restructuring

Common Business Valuation Methodologies

The three primary approaches recognised under US GAAP, IFRS, and Indian accounting standards are:

- Discounted Cash Flow (DCF) : Projects future free cash flows and discounts them to present value at a risk-adjusted rate. Best suited for companies with visible, forecastable cash generation.

- Market Approach : Values the business using comparable public company trading multiples (EV/Revenue, EV/EBITDA) or precedent M&A transaction multiples from the same sector.

- Asset Approach : Derives value from the net realisable value of assets, most applicable to holding companies, asset-heavy businesses, or very early-stage ventures with minimal revenue.

The output is a single number the enterprise value or equity value of the company. It applies to the business as a whole and does not, by itself, tell you the value of any individual share class.

ESOP 409A Valuation: Determining What One Common Share Is Worth

An ESOP 409A valuation builds on the business valuation but then goes several steps further. The additional work is necessary because, in most venture-backed start ups, not all shares are created equal.

Investors who participated in your Series A received preferred shares. Those preferred shares typically come with contractual protections that common shares do not carry liquidation preferences (often 1x or 2x), participation rights, anti-dilution provisions, and conversion features. These protections mean that, in any exit scenario, preferred shareholders receive their invested capital back (and sometimes more) before common shareholders receive anything.

This economic reality creates a systematic gap between the value of a preferred share and the value of a common share. In a $8 million company with, say, $3 million of liquidation preference held by Series A investors, common shareholders do not have a claim on the full $8 million they have a claim on what remains after the preferred waterfall is satisfied.

Treating the fundraise price per share as the ESOP exercise price ignores this gap entirely and overvalues common shares in a way that makes stock options economically worthless for employees, who would need the company to dramatically outperform before their options have any value.

The ESOP 409A Valuation Process: Four Analytical Steps

How the FMV of Common Shares Is Determined

Step 1 : Business Valuation: Establish the company’s total equity value using DCF, market comparables, or the asset approach. This is the starting enterprise value.

Step 2 : Cap Table Analysis: Map every share class founders’ equity, Series A/B preferred, convertible notes, warrants, existing ESOP pool. Identify the specific rights attached to each class: liquidation preferences, participation, anti-dilution, conversion ratios.

Step 3 : Option Pricing Model (OPM): Treat each share class as a call option on the company’s total value. Use the OPM to model how the total equity value would be distributed across share classes under various exit scenarios accounting for the preferred waterfall before common shareholders receive value.

Step 4 : Black-Scholes Model (BSM): Apply the Black-Scholes formula to estimate the fair value of individual stock options. Inputs include the common share FMV derived from Step 3 (the stock price input), the proposed exercise price, expected time to expiry, implied volatility, and the risk-free rate. Output: The Fair Market Value of one common share the price at which ESOP options must be granted to comply with IRS Section 409A (US) or Ind AS 102 (India).

The resulting common share FMV is typically lower than the preferred share price from the most recent funding round. This is not aggressive or conservative it is accurate. It reflects the economic reality of where common shareholders stand in the exit waterfall relative to preferred investors.

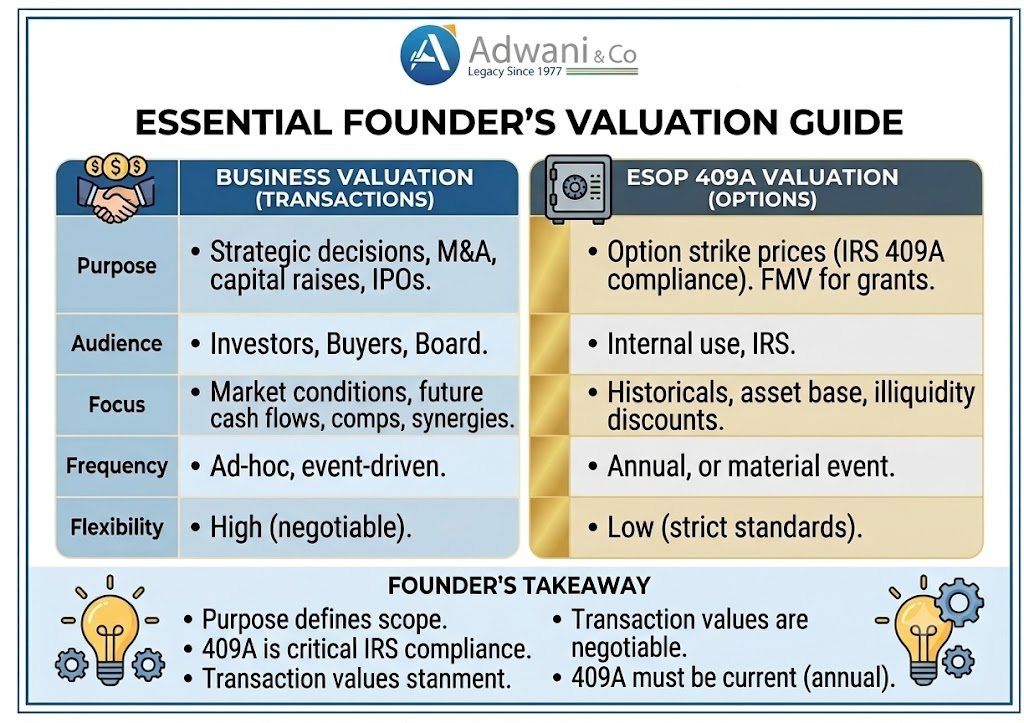

Business Valuation vs ESOP 409A Valuation: At a Glance

| Factor | Business Valuation | ESOP / 409A Valuation |

| Core Question | What is the whole company worth? | What is one common share worth for stock option grants? |

| Primary Use Cases | Fundraising, M&A, investor transactions, shareholder buy-sells | Setting ESOP exercise price per IRS Section 409A / Ind AS 102 |

| Methods | DCF, Market Comparables, Asset Approach | Business valuation → Cap Table → OPM → Black-Scholes (BSM) |

| Output | Enterprise value or total equity value | Fair Market Value (FMV) of common shares |

| Share Class Scope | All share classes | Common shares specifically (after waterfall allocation) |

| Regulatory Basis | SEBI / AICPA / IFRS 13 / US GAAP | IRS Section 409A (US) | IFRS 2 / Ind AS 102 (India) |

| Typical Timing | Event-driven (fundraise, M&A, restructuring) | Annual or before each new ESOP grant round |

Why This Distinction Matters for Founders and Finance Teams

The stakes are real on both sides of the border.

In the United States

IRS Section 409A requires that non-qualified stock options be granted at no less than the FMV of the underlying stock on the grant date. The FMV must be determined by a qualified independent appraisal conducted within the past 12 months, or by another IRS-approved method. Granting options below FMV even inadvertently creates immediate ordinary income tax liability for the employee in the year of grant, plus an additional 20% excise tax penalty, plus applicable interest. The employer can also face reporting obligations and penalties.

In India

Ind AS 102 (Share-Based Payment) requires companies to measure and expense the fair value of share-based awards at the grant date. For listed entities and companies in the preparatory phase for listing, SEBI’s ESOP regulations also prescribe specific valuation requirements. Getting the grant price wrong leads to incorrect financial statement disclosures and potential SEBI scrutiny.

As CA Manish notes from cross-border advisory engagements: “The most common mistake we see is founders equating their fundraise valuation with their ESOP pricing. The fundraise tells you what an investor was willing to pay for preferred shares with full protections. It tells you very little about what a common share is worth on a standalone basis and that difference is exactly what the 409A process is designed to calculate.”

Key Takeaways

- A business valuation and an ESOP 409A valuation answer different questions and serve different purposes they are not interchangeable.

- Business valuation determines total company value; ESOP 409A valuation determines the Fair Market Value of common shares for stock option grant purposes.

- Preferred shares carry superior economic rights liquidation preferences, participation, anti-dilution that systematically make them more valuable than common shares. The 409A process accounts for this.

- The Option Pricing Model (OPM) allocates company value across share classes by modelling the preferred waterfall. The Black-Scholes Model then values the stock options themselves.

- IRS Section 409A (US) and Ind AS 102 / SEBI regulations (India) both require that options be granted at FMV making an accurate, defensible 409A analysis non-negotiable for compliant ESOP programmes.

- The 409A valuation should be refreshed annually and before each new ESOP grant round, or whenever a material event (funding round, acquisition discussion) occurs.

Frequently Asked Questions

Q: What is the difference between a business valuation and a 409A valuation?

A: A business valuation determines the total worth of the company used for fundraising, M&A, or shareholder transactions. A 409A valuation is a more specific exercise that determines the Fair Market Value of common shares alone, for the purpose of setting the correct exercise price on employee stock option grants under IRS Section 409A

Q: What is the Black-Scholes Model and how is it used in ESOP valuation?

A: The Black-Scholes Model (BSM) is a mathematical formula used to estimate the fair value of a stock option. In ESOP valuations, it takes the common share FMV (derived from the OPM), the exercise price, expected time to expiry, implied volatility of the underlying stock, and the risk-free interest rate as inputs. The output is the fair value per option used for financial statement disclosure under IFRS 2 / Ind AS 102 and for IRS Section 409A compliance.

Q: Why is the ESOP exercise price typically lower than the Series A or Series B price per share?

A: Series A/B investors purchase preferred shares, which carry liquidation preferences and other protections that rank ahead of common shareholders in any exit scenario. After modelling the cap table waterfall using the Option Pricing Model, the resulting Fair Market Value of common shares which have no such protections is ordinarily lower than the price paid by preferred investors.

Q: Does Section 409A apply to India-incorporated startups?

A: Section 409A is US-specific. India-incorporated companies follow Ind AS 102 (Share-Based Payment) for accounting and SEBI ESOP regulations for compliance. However, startups with US investors, dual-structure entities (an Indian operating company with a US holding company), or those planning a US listing need to satisfy both frameworks making professional valuation support across both jurisdictions essential.

Q: How often should a company conduct a 409A valuation?

A: The IRS requires a fresh 409A valuation at least once per year, or before each new option grant if more than 12 months have elapsed since the last appraisal. A new 409A is also required after any material event a significant funding round, a change in business trajectory, or a pending sale or merger process.

Conclusion:

Business valuation and ESOP 409A valuation are related but distinct disciplines. One tells you what the company is worth. The other tells you what one common share is worth taking into account the economic realities of your cap table, the rights of different shareholder classes, and the specific regulatory framework governing employee equity compensation.

For founders scaling their teams and building equity compensation programmes, getting this right is not a luxury. It is a compliance requirement, an employee trust issue, and increasingly, a diligence item for future investors who will examine your ESOP programme as part of any financing round or acquisition.

The valuation model matters. But understanding why you are doing the valuation and which output you actually need matters more.

Author

CA. Manish R. Mata Practising In India (Ex – PwC), At Adwani & Co LLP leads the International Accounting & Tax Support vertical, delivering structured execution assistance to US CPA firms and overseas businesses.

Disclaimer

Adwani & Co LLP is a multi-disciplinary professional services platform. The blogs shared are for educational and informational purposes only and are intended to promote awareness around finance, accounting, taxation, reporting, and business advisory topics. Nothing contained herein should be construed as solicitation or advertisement of professional services. Where professional services are required under applicable laws or regulations, such services are rendered in accordance with relevant professional and regulatory requirements. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP.

© 2026 Adwani & Co LLP. All rights reserved. | adwaniandco.com | Pune, Maharashtra, India

Need Business Valuation, 409A, or ESOP Advisory Support?

If your business is building an ESOP programme, preparing for a funding round, or needs accurate valuation support across Indian or US regulatory frameworks, the team at Adwani & Co LLP would be happy to connect. We bring together financial modeling expertise, international accounting knowledge, and cross-border regulatory experience to support your equity and growth objectives.

Explore our Financial Modeling & Valuation Services adwaniandco.com

Leave a Reply