Finance Professionals and AI

There is a version of the future that looks something like this: an AI model prepares your financial statements, flags every variance, models out three scenarios, and suggests a tax treatment all before your morning coffee. No analyst. No partner review. No judgment call required.

That version of the future is both closer than most people realise and more incomplete than most people expect.

Over the last several months, our team at Adwani & Co LLP has spent meaningful time reviewing AI-generated outputs across financial modeling, accounting, tax analysis, and business performance reporting. The exercise has been instructive not because AI performed poorly, but because of precisely where it fell short. And it almost never fell short on the calculation.

The Calculation Is Not the Hard Part

Ask an AI model to build a discounted cash flow model, reconcile a set of accounts, or identify a variance between actuals and budget and it will typically do a competent job. The mechanics of finance: the formulas, the structures, the formats these are well within the capability of today’s AI tools.

What is harder to automate is the layer that sits above the calculation. The reasoning.

Where AI-Generated Finance Outputs Tend to Struggle

• Incorrect assumptions presented without qualification or disclosure

• Technically valid conclusions that are commercially or contextually wrong

• Reasoning that sounds authoritative but does not hold up under scrutiny

• Missing flags on transactions or entries that a practitioner would immediately question

• Tax treatments suggested without considering jurisdiction-specific nuance or recent regulatory changes

This is not a criticism of the technology. It is a structural observation. AI models are trained on patterns in data. Professional judgment is built on experience, context, and accountability. These are genuinely different things.

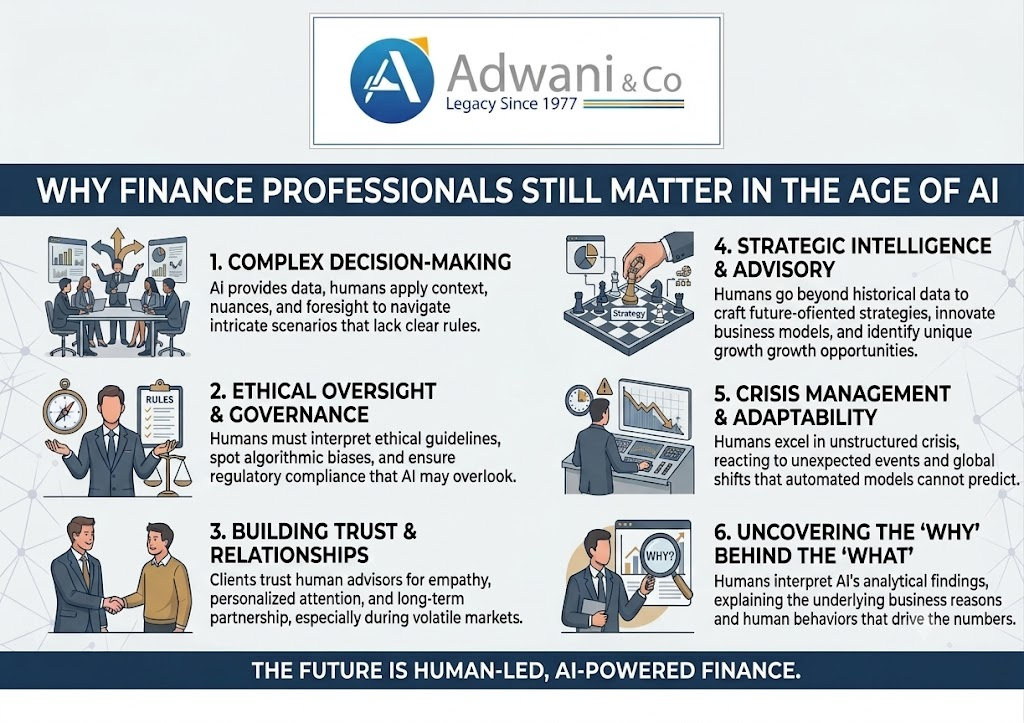

What Finance Professionals Judgment Actually Means in Finance

The term gets used loosely, but in practice, Financial professionals judgment in finance and accounting refers to a set of specific capabilities that go beyond technical execution.

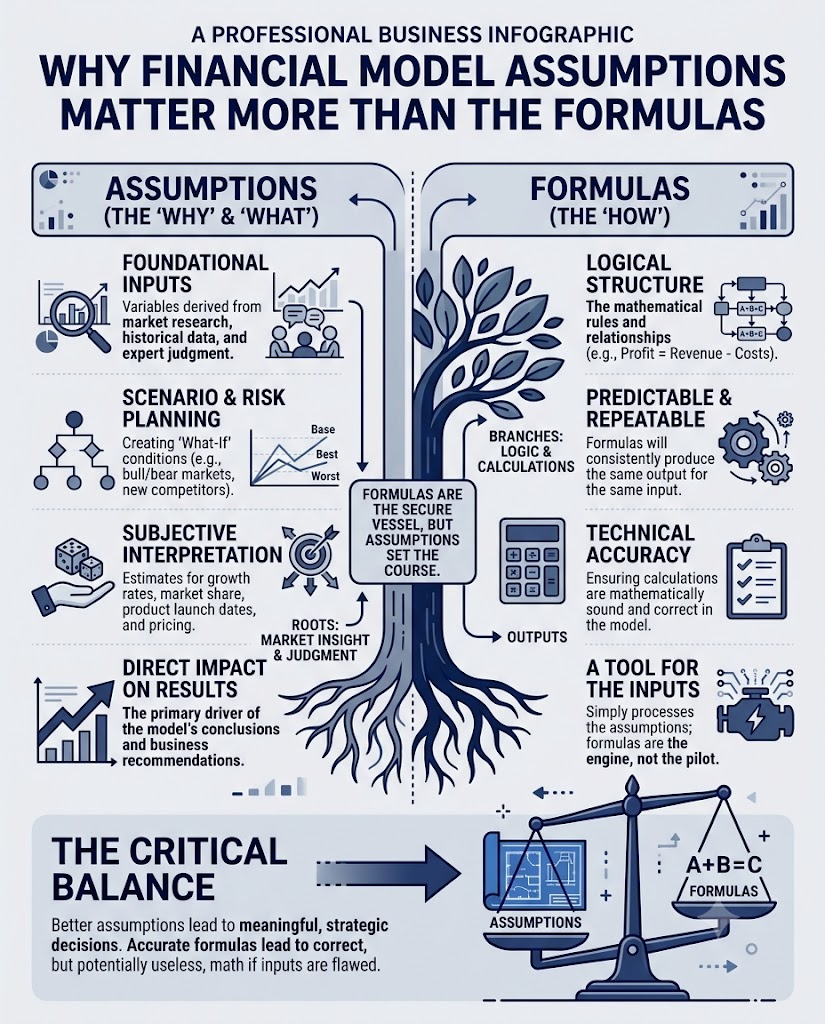

Evaluating Whether Assumptions Are Reasonable

A financial model is only as good as the assumptions it is built on. An AI system can populate assumptions from historical data or industry benchmarks. It will rarely ask whether those benchmarks apply to this specific business, in this specific market, at this specific stage of its development. A finance professional will.

Connecting the Numbers to the Business Reality

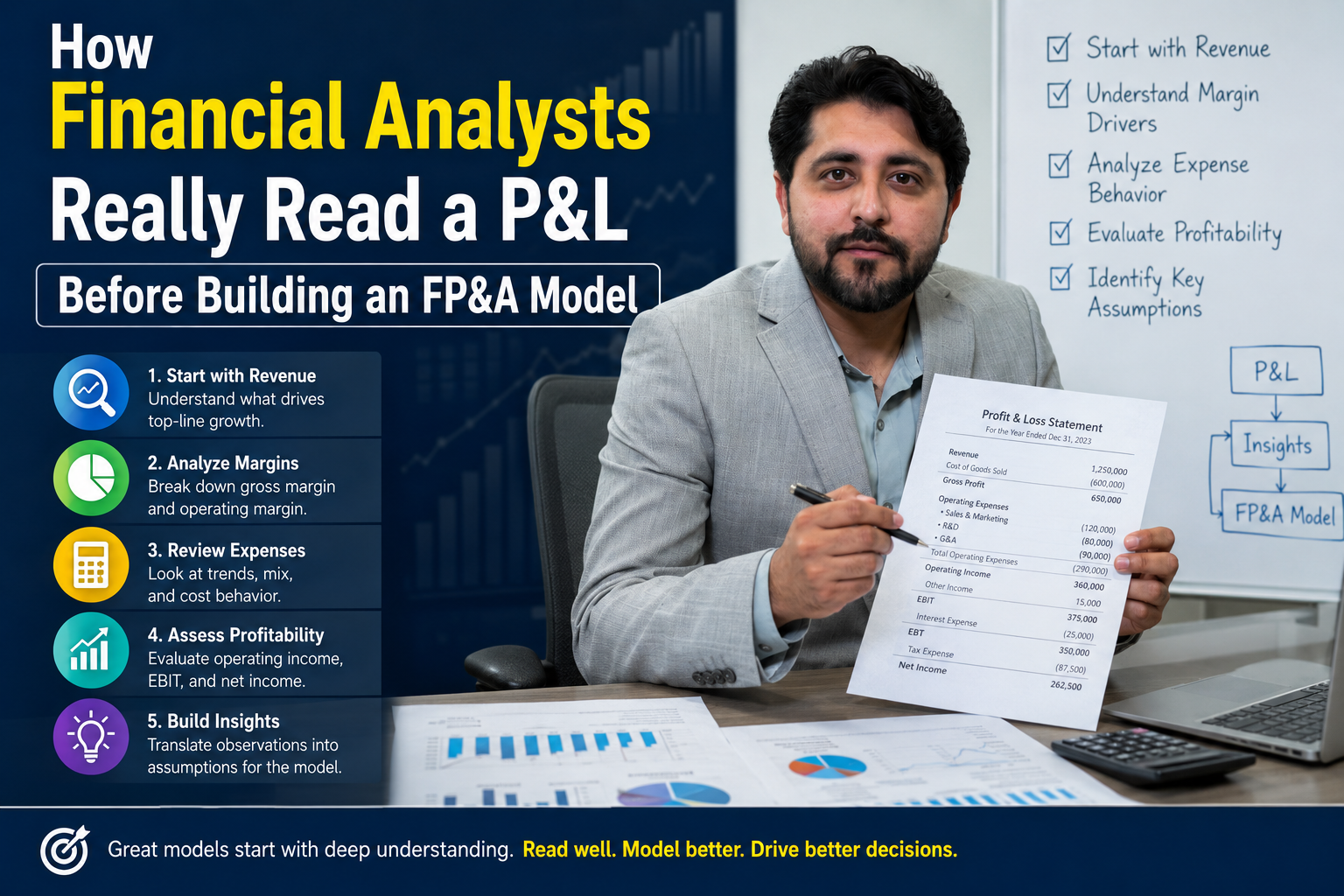

When a variance analysis shows that gross margins have declined by 4 percentage points quarter-over-quarter, the calculation is straightforward. The professional question is: why, and does it matter? That requires knowing something about the business sits pricing model, its cost structure, its competitive position. The number is just the starting point.

Applying Judgment Under Regulatory and Finance Professional Standards

Tax treatments, accounting policies, disclosure requirements these are governed by frameworks like IFRS, US GAAP, the Income Tax Act, or IRS guidance. These frameworks require interpretation. The same transaction can be treated differently depending on facts and circumstances that a practitioner is trained to identify and evaluate. AI can surface the options. The professional makes the call.

Standing Behind the Work

Finance Professionals accountability matters. When a financial report is signed off, when a tax position is taken, when a valuation is presented to a board or an investor someone is professionally responsible for that output. That accountability structure does not transfer to an AI tool. It rests with the professional.

AI Capability vs. Professional Judgment: A Practical Comparison

| What AI Does Well | Where Professional Judgment Is Needed |

| Data processing and structuring at scale | Evaluating whether the data is complete and reliable |

| Applying standard formulas and models | Questioning whether the model structure fits the situation |

| Identifying patterns and variances | Determining what those patterns mean for the business |

| Generating multiple scenarios quickly | Deciding which scenarios are realistic and commercially relevant |

| Drafting tax computations and analysis | Applying jurisdiction-specific judgment and regulatory interpretation |

| Producing formatted financial reports | Reviewing whether disclosures are adequate and positions are defensible |

| Flagging anomalies in large datasets | Knowing which anomalies require action and which do not |

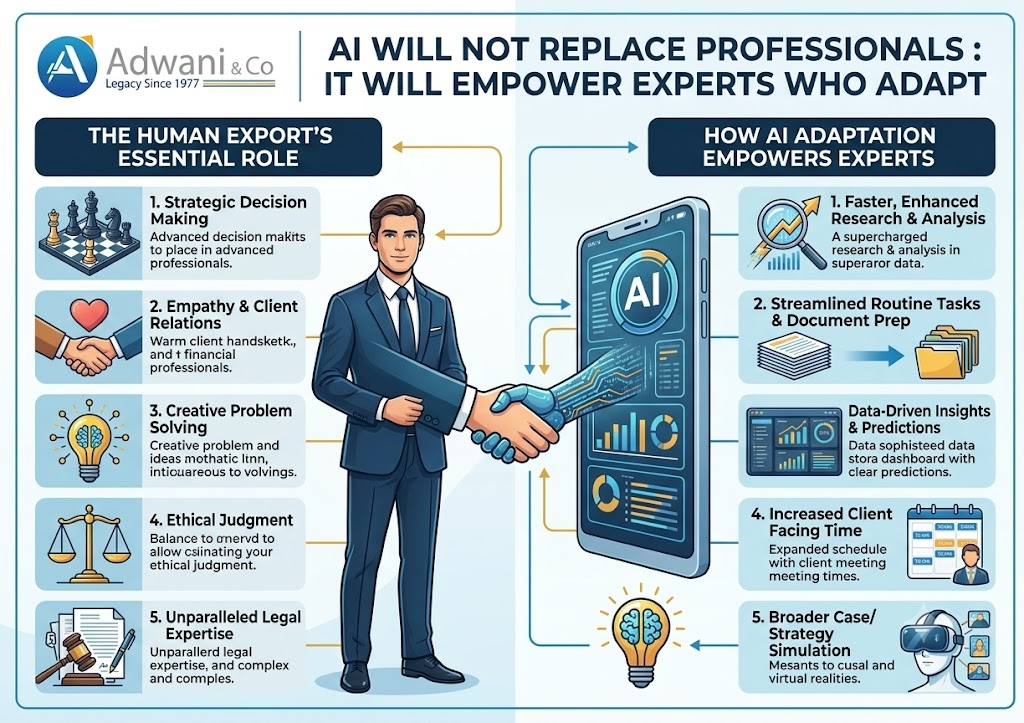

The Right Question Is Not Replacement: It Is Integration

The conversation in professional circles often frames AI as a threat to finance careers. After working closely with these tools across real client engagements, CA Manish Head Consultant for International Accounting and Financial Modeling at Adwani & Co LLP has consistently observed the opposite dynamic.

The better AI becomes at handling the mechanical layer of finance, the more visible the value of the professional judgment layer becomes. AI removes the excuse for spending most of your time on data entry, number-crunching, and report formatting. What is left the interpretation, the advisory, the structured thinking is precisely the work that creates value for clients.

| The Most Effective Finance Teams We Work With Share One Common Pattern They use technology to eliminate repetitive, low-judgment work. They concentrate their best people on analysis, interpretation, and decision support. They treat AI outputs as a starting point for review not a finished product. They understand that speed and scale are AI’s advantage; judgment and accountability are theirs. |

Practical Implications for Finance Professionals and Business Owners

Whether you are a CFO, a CA in practice, a finance team lead, or a business owner who works closely with financial data, the practical implications are similar.

For Finance Professionals

- Develop the ability to critically evaluate AI-generated analysis, not just accept it

- Invest in the interpretive and advisory skills that AI cannot replicate

- Build workflows that combine AI efficiency with human review at decision-critical points

- Stay current on regulatory changes this is an area where AI outputs can quickly become outdated or jurisdiction-specific errors can slip through

For Business Owners and Founders

- Do not mistake a well-formatted AI output for a professionally reviewed one presentation and accuracy are different things

- Ensure there is a qualified professional accountable for the financial work, regardless of the tools being used

- Use AI to get faster, more frequent visibility into your numbersbut invest in the advisory relationship that helps you act on what you see

- When significant decisions fundraising, restructuring, cross-border transactions, tax positions are on the table, professional review is not optional

Read our detailed guide on AI Will Not Replace Professionals : It Will Empower Experts Who Adapt

Key Takeaways

Summary

• AI performs well on the mechanical and computational layer of finance data structuring, model building, report generation, variance identification.

• The gap between AI outputs and professionally reliable conclusions is most apparent in reasoning: assumptions, interpretation, regulatory judgment, and accountability.

• Finance Professionals judgment in finance is built on experience, context, and professional accountability qualities that cannot be automated.

• The most effective approach combines AI’s scale and speed with a human professional’s interpretive and advisory capability.

• For significant financial decisions, professional review remains non-negotiable regardless of the tools being used.

• The future of finance is not AI versus professionals it is AI and professionals, each contributing what they do best.

Frequently Asked Questions

1. Can AI tools replace a CA or CPA for tax filing and financial reporting?

Not reliably. AI tools can assist with data processing, computation, and draft preparation, but tax filings and financial reports carry professional responsibility. A qualified CA or CPA applies judgment to regulatory interpretation, jurisdiction-specific rules, and disclosure adequacy in ways that AI cannot replicate or be held accountable for.

2. What is the biggest limitation of AI-generated financial models?

The most significant limitation is not technical accuracy in the calculations it is the assumptions. AI models will build on available data without always questioning whether the inputs are appropriate for a specific business or situation. A finance professionals reviews both the structure of the model and the reasonableness of the assumptions driving it.

3. How should a business owner use AI in their financial workflow?

AI works well for routine bookkeeping, data extraction, report formatting, and preliminary analysis. For anything involving decision-making, tax positions, investor reporting, or compliance, it should be treated as a first draft that a qualified professional reviews. Think of it as a capable analyst useful, but not the final word.

4. Will AI change what skills are valuable for finance professionals?

Yes, significantly. Finance Professionals who build strong interpretive, advisory, and judgment-based skills will find AI increases their capacity and reach. Those who have primarily relied on technical execution of routine tasks will need to adapt. The premium on analytical thinking, client advisory, and structured reasoning is increasing not decreasing.

5. Does Adwani & Co LLP use AI tools in its advisory and accounting work?

Yes. Our team actively integrates AI-assisted tools in financial analysis, modeling, and reporting workflows. The difference is that every significant output is reviewed by a qualified professional before it informs a client decision or compliance filing. Technology improves our throughput; professional judgment governs our outputs.

Conclusion

The arrival of capable AI tools in finance and accounting does not reduce the value of Finance Professionals expertise it sharpens the focus on where that expertise actually lives. The calculation has never been the hard part. The hard part is knowing whether the reasoning behind the calculation is correct, whether the assumptions are defensible, and whether the conclusion will hold up when it matters.

That combination AI handling scale and efficiency, professionals providing judgment and accountability is where finance advisory is heading. And for businesses navigating complex financial decisions, tax positions, or cross-border reporting obligations, having a qualified professional in that chain is not a legacy requirement. It is a structural necessity.

Work With Adwani & Co LLP

If your business is looking to build stronger financial systems, improve reporting visibility, or benefit from professional review of AI-assisted analysis, the team at Adwani & Co LLP would be happy to connect.

We support clients across financial modeling, Virtual CFO advisory, international accounting, bookkeeping systems, and cross-border tax combining modern tools with qualified professional judgment. Explore our services: Virtual CFO Services | Financial Reporting & MIS Support | International Accounting & Advisory | QuickBooks & Xero Bookkeeping

Author

CA. Manish R. Mata Practising In India (Ex – PwC), At Adwani & Co LLP leads the International Accounting & Tax Support vertical, delivering structured execution assistance to US CPA firms and overseas businesses.

Disclaimer

Adwani & Co LLP is a multi-disciplinary professional services platform. The blogs shared are for educational and informational purposes only and are intended to promote awareness around finance, accounting, taxation, reporting, and business advisory topics. Nothing contained herein should be construed as solicitation or advertisement of professional services. Where professional services are required under applicable laws or regulations, such services are rendered in accordance with relevant professional and regulatory requirements. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP.

© 2026 Adwani & Co LLP. All rights reserved. | adwaniandco.com | Pune, Maharashtra, India