Tax Saving vs Wealth Creation

Every March, millions of Indian taxpayers do something that quietly costs them their financial future. They rush to exhaust their Section 80C limit not because the investment makes sense but because the tax deadline is looming. Sound familiar? If yes, this article is the most important thing you’ll read this ITR season.

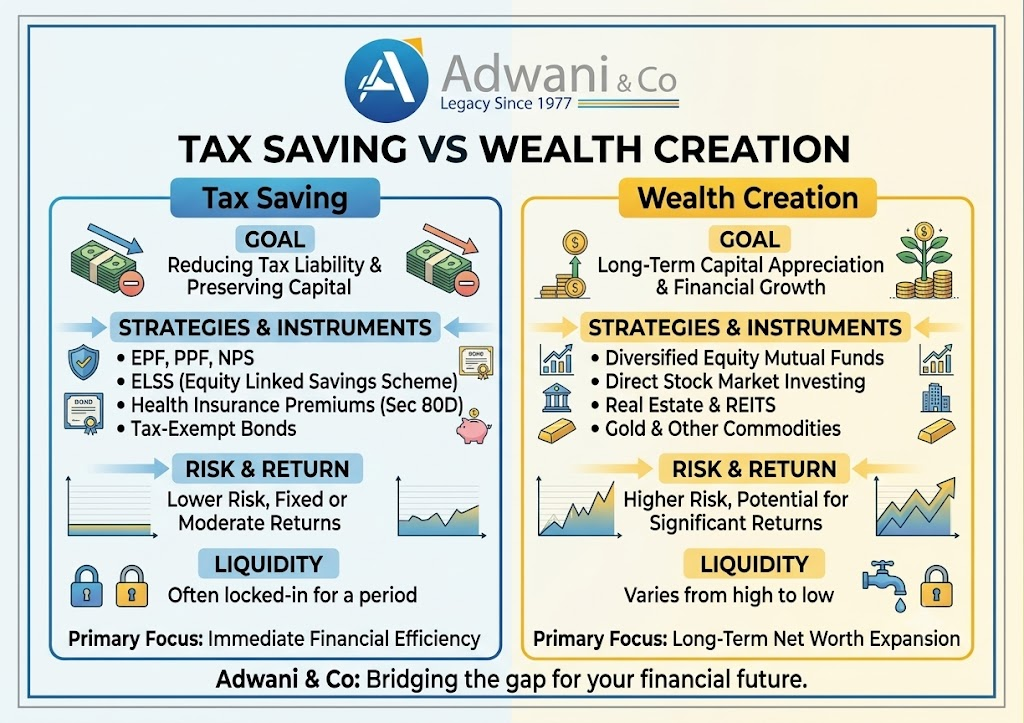

The Section 80C Trap Most Indians Still Fall Into

For decades, the default advice in Indian households has been simple: invest ₹1.5 lakh under Section 80C, save tax, repeat next year. So people poured money into:

- LIC endowment policies with 4–5% effective returns

- Tax-saving Fixed Deposits locked for 5 years at modest interest rates

- ELSS mutual funds often the smartest option in this category

- PPF, NSC, and other government-backed schemes

None of these are bad products. But here is the critical question that most taxpayers never ask: Would I still invest in this if there was no tax benefit?

Common Tax-Saving Mistake to Avoid

- Investing money you cannot afford to lock up just to claim a Section 80C deduction

- Buying high-premium insurance policies primarily as a tax-saving tool not as a life cover need

- Ignoring the new tax regime calculator before deciding on 80C investments for AY 2026-27

Treating tax planning as a once-a-year March activity instead of a year-round wealth strategy

How the New Tax Regime Is Changing the Tax Saving vs Wealth Creation Conversation

The Income Tax Department‘s push towards the New Tax Regime especially after Budget 2024 raised the standard deduction to ₹75,000 and the rebate limit to ₹12 lakh under Section 87A has fundamentally changed the math. For many salaried taxpayers, the new regime now offers a lower effective tax liability without making any additional 80C investments.

What does this mean in practice? If you switch to the new tax regime, you lose the Section 80C deduction benefit. Suddenly, the LIC policy you bought ‘for tax saving’ loses its primary justification. The 5-year tax-saving FD you locked ₹1.5 lakh into does it still make sense at current interest rates compared to liquid mutual funds?

Key Insight: Old vs New Tax Regime Checklist (AY 2026-27)

- Compare your total deductions (80C, 80D, HRA, home loan) against the new regime’s flat rebate

- If your deductions total less than ₹3–4 lakh, the new regime likely offers lower tax outgo

- Under the new regime, prioritise investments for returns not tax deductions

- Use Form 10-IEA to switch regimes if needed consult a tax professional before deciding

From Tax Saving to Wealth Creation: A Mindset Shift India Needs

What’s interesting about this ITR season and something that tax professionals like Dr. Haresh Adwani, founder of Adwani & Co LLP, have been observing closely is that taxpayer conversations are evolving. More people are now asking about long-term mutual fund investments, equity market participation, retirement planning, and financial independence rather than just which Section 80C product to buy before March 31.

This is a deeply positive shift. Because the goal of good financial planning has never been just to save tax it has always been to build real, lasting wealth.

Smart Investing Framework: 3 Questions to Ask Before Every Investment Decision

1. Does This Investment Align With My Financial Goals?

Whether you’re investing in ELSS mutual funds for tax saving and long-term equity growth, or choosing between the old vs new tax regime for AY 2026-27, every rupee you invest should have a purpose beyond tax reduction. Define your goals: retirement corpus, children’s education, or home purchase.

2. Do I Understand the Risk-Return Profile?

ELSS funds carry market risk but deliver equity-linked returns over 3+ years. PPF is risk-free but long-term and illiquid. A tax-saving FD gives certainty but often underperforms inflation. Understand what you’re signing up for not just the tax receipt you’ll get.

3. Would This Investment Make Sense Without the Tax Benefit?

This is the single most powerful question in personal finance. If the answer is no if you wouldn’t invest in that product without the 80C benefit it’s a sign the investment is serving the tax planner in you, not the wealth creator in you.

Smart Investment Alternatives Worth Considering (Beyond 80C)

- Equity mutual funds (not just ELSS) for long-term wealth creation with LTCG benefits post Section 112A

- Index funds and ETFs low-cost, market-linked, ideal for passive wealth building

- NPS (National Pension System) Section 80CCD(1B) gives an additional ₹50,000 deduction over 80C

- Direct equity investing STCG and LTCG tax on shares is now well-defined after Budget 2024 amendments

Goal-based SIPs aligning each SIP with a specific life goal creates wealth with financial discipline

Read our detailed guide on: ITR Filing 2026: Deadlines, Penalties & Smart Tax Saving Guide

Key Takeaways: Tax Saving vs Wealth Creation

| Tax Saving Focus | Wealth Creation Focus |

| Invest to reduce tax liability | Invest to grow net worth over time |

| March deadline drives decision | Goal horizon drives decision |

| Product-first thinking (LIC, FD, ELSS) | Goal-first thinking (equity, NPS, SIP) |

| Returns may lag inflation | Returns aimed to beat inflation consistently |

| New regime may make 80C irrelevant | Investment logic holds in any tax regime |

Frequently Asked Questions

Q: Is Section 80C investment still worth it under the new tax regime for AY 2026-27?

A: Under the new tax regime, Section 80C deductions are not available. If you opt for the new regime, invest in products based on returns and goals not tax benefits.

Q: Which is better for wealth creation in India ELSS mutual funds or equity mutual funds?

A: ELSS offers tax saving plus equity returns with a 3-year lock-in. Plain equity mutual funds offer more flexibility and often better wealth creation for long-term investors beyond 80C

Q: How do I decide between the old vs new tax regime for smart tax planning in 2026-27?

A: Calculate your total eligible deductions (80C, 80D, HRA, home loan interest). If they exceed ₹3–3.5 lakh, the old regime likely saves more tax; otherwise, the new regime wins.

Q: What is the difference between tax planning and financial planning for Indian taxpayers?

A: Tax planning minimises your current tax outgo; financial planning builds your long-term net worth. Good investing requires both but wealth creation goals should always lead the strategy.

Q: Can I invest in LTCG-friendly assets like equity mutual funds and still save tax in India?

A: Yes. Long-term capital gains (LTCG) on equity mutual funds up to ₹1.25 lakh per year are tax-free under Section 112A. Beyond that, gains are taxed at 12.5% still one of the most tax-efficient ways to build wealth

Conclusion:The Goal Is Not Just to Save Tax : It’s Wealth Creation

India’s taxation landscape has shifted. The new tax regime, revised LTCG rules post-Budget 2024, and increasing awareness of mutual funds and equity investing mean that the old template of ‘invest ₹1.5 lakh in 80C products and forget it’ is no longer sufficient or even optimal for many taxpayers.

The question every Indian investor must honestly answer this financial year is not ‘How do I exhaust my 80C limit?’ but rather ‘Am I investing in a way that will make me financially free — with or without a tax benefit?’

Good tax planning is important. But it should serve your wealth creation goals not the other way around. The Income Tax Department’s own resources at incometaxindia.gov.in and SEBI’s investor education portal both emphasise the importance of informed, goal-based investing over reactive tax-saving.

About the Author

Dr. Haresh Adwani

Ph.D. in Commerce | Law Graduate | Managing Partner, Adwani & Co LLP Dr. Haresh Adwani holds a Ph.D. in Commerce and is a qualified Law graduate with over two decades of hands-on experience in GST advisory, direct taxation, and statutory compliance for businesses across Pune and Maharashtra. As Managing Partner of Adwani & Co LLP a firm established in 1977 by Advocate N. T. Adwani Dr. Adwani has guided hundreds of

SMEs, startups, and corporates through India’s evolving tax landscape. He is a recognised advisor on GST compliance, company formation, and Virtual CFO services, and regularly

contributes to professional seminars and industry forums in Pune.

Disclaimer

This article is intended for general informational purposes only and does not constitute professional tax, financial, or legal advice. While every effort has been made to ensure accuracy as of the date of publication, tax laws, forms, and procedures are subject to change. Readers should consult a qualified chartered accountant or tax professional before making decisions based on this content. Adwani and Company accepts no liability for actions taken solely on the basis of this article.