CA Dipesh Gurubakshani June 2026 9 min read

NRI ITR Filing 2026

The Wrong Box That Costs NRIs Thousands

One wrong selection on a single screen. That’s all it takes.

Thousands of Non-Resident Indians file their income tax returns in India every year believing they’ve done everything right only to receive notices, see refunds delayed by months, or discover their tax computation was incorrect all along. The irony? Most of these errors have nothing to do with the amount of income earned. They come from procedural gaps, misunderstood rules, and assumptions that simply don’t apply to NRI taxpayers.

If you are an NRI with income from India bank interest, rent, dividends, capital gains, or even F&O trading this guide on NRI ITR filing in 2026 will walk you through every critical area you cannot afford to get wrong.

Why NRI ITR Filing 2026 Is More Complex Than It Looks

NRI ITR filing is not complicated because NRIs earn more. It’s complicated because the rules that apply to resident Indians including popular benefits like the Section 87A rebate do not automatically extend to NRIs.

The Income Tax Department of India has clearly outlined residential status as the foundation of tax liability determination. Under the Income Tax Act, 1961, your residential status in a given financial year determines which incomes are taxable, which deductions are available, and which ITR form is applicable. Getting any of these wrong can spiral into compliance issues that take months to resolve.

According to Dr. Haresh Adwani PhD in Commerce, law graduate, and founding partner of Adwani and Company “NRIs often approach ITR filing the way a resident would. That’s the first and most expensive mistake they make. The rules diverge significantly, and the cost of that divergence is almost always paid later.”

The Most Common NRI ITR Filing Mistakes in 2026

Mistake 1 : Filing the Wrong ITR Form

This is the single most frequent error in NRI income tax return filing in India. Choosing the wrong form results in a defective return notice under Section 139(9), forcing a refiling under deadline pressure.

Here’s the correct framework for NRI ITR form selection in 2026:

ITR 2 is the correct form if the NRI has:

- Interest income from NRO/NRE bank accounts

- Capital gains from shares, mutual funds, or property

- Dividend income from Indian companies

- Rental income from property in India

- No business or professional income

ITR 3 becomes mandatory if the NRI has:

- Intraday trading income

- F&O (Futures & Options) income

- Any business or professional income earned from India

Many NRIs who do casual trading on Indian exchanges mistakenly file ITR 2, which does not accommodate F&O income. This mismatch is flagged by the Income Tax Department’s automated systems, often triggering scrutiny notices. Learn more about our ITR-2 and ITR-3 Filing Support for NRIs

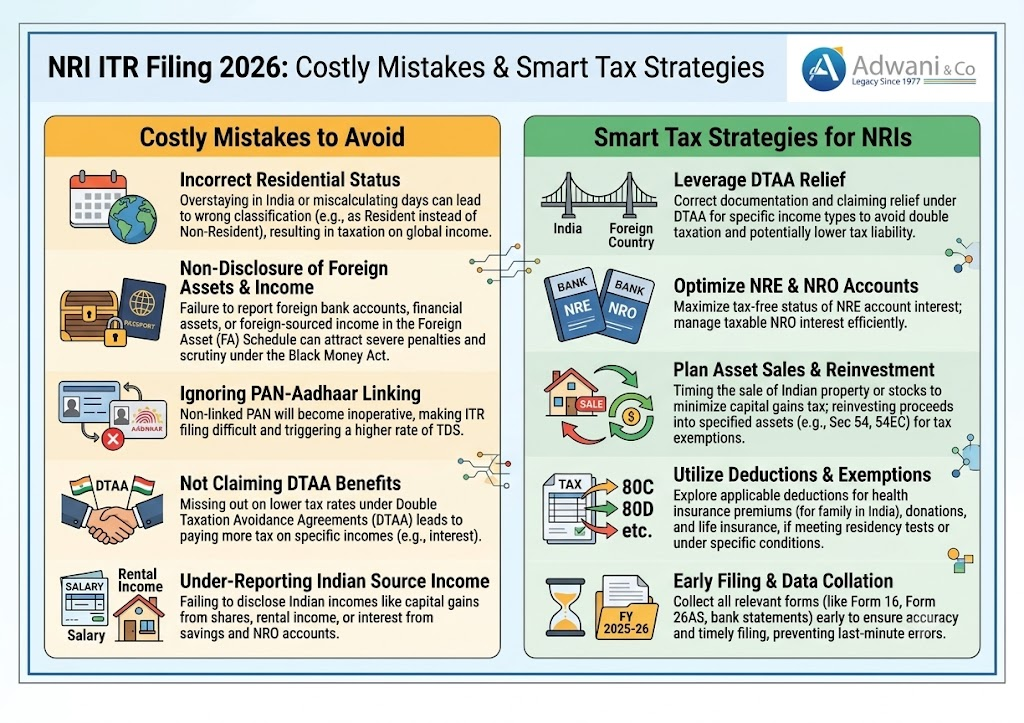

Mistake 2 : Claiming the Section 87A Rebate as an NRI

This is perhaps the most misunderstood provision in NRI ITR filing. Section 87A of the Income Tax Act provides a rebate of up to ₹12,500 (or up to ₹25,000 under the new tax regime) to resident individuals whose total income does not exceed the specified threshold.

Section 87A rebate is NOT available to NRIs. Full stop.

Many NRI taxpayers and even some tax preparers incorrectly apply this rebate, which either creates a mismatch during ITR processing or results in a demand notice later. If you are an NRI with income tax liability in India, the full tax must be paid without this rebate.

Mistake 3 : Skipping the Old vs New Tax Regime Comparison

The old vs new tax regime comparison for NRIs in 2026 is not optional it’s essential. Unlike resident taxpayers who may have a default regime applied by their employer, NRIs must make an informed, independent choice when filing.

Practical Example:

Consider an NRI with the following Indian income profile for FY 2025-26:

| Income Type | Amount |

| NRO Bank Interest | ₹1,20,000 |

| Rental Income (after 30% standard deduction) | ₹2,10,000 |

| Long-Term Capital Gains (LTCG) on Shares | ₹1,50,000 |

| Dividend Income | ₹40,000 |

| Total Income | ₹5,20,000 |

Under the old tax regime, this NRI could claim Section 80C deductions (if applicable) on eligible investments, potentially reducing taxable income. Under the new tax regime, no 80C deductions are available, but a simplified slab structure applies.

Critically, LTCG above ₹1.25 lakh on listed equity is taxed at 12.5% flat (post-Budget 2024 amendment) regardless of regime. The regime choice primarily impacts ordinary income slabs.

Without running this comparison before filing, many NRIs end up paying more tax than required. Read our detailed guide on Old vs New Tax Regime 2026 for NRIs

Mistake 4 : Not Reconciling AIS and Form 26AS

Before filing any NRI income tax return in India, reconciling your AIS (Annual Information Statement) and Form 26AS is non-negotiable. These documents reflect what banks, mutual funds, brokers, and property registrars have reported to the Income Tax Department against your PAN.

In 2026, the Income Tax Department’s data-matching infrastructure is significantly more sophisticated. TDS deducted on NRO interest, rent payments, and capital gains transactions are all pre-populated in the AIS. If your ITR does not match these figures, the return gets flagged automatically.

Dr. Haresh Adwani notes: “We routinely see NRI clients where TDS has been deducted at 30% on NRO interest, but the credit doesn’t appear in their ITR because they didn’t verify Form 26AS. That means a valid TDS credit goes unclaimed, and the refund is delayed or rejected.”

Mistake 5 : Incorrect Residential Status Declaration

Your residential status under the Income Tax Act is determined by the number of days spent in India during the financial year not by your passport or visa status. The rules are precise:

- Resident (Ordinary Resident): 182 days or more in India in the FY, or 60 days in the FY + 365 days in the preceding 4 years

- NRI: Does not meet the above conditions

A person of Indian origin visiting India for extended periods may unknowingly cross the residential threshold and become taxable on global income a scenario that carries serious consequences. The 120-day rule introduced in the Finance Act, 2020 (for Indian citizens with income above ₹15 lakh from India) adds another layer of complexity.

Getting residential status wrong in the ITR not only affects what income is taxable but also which deductions and forms are applicable.

Key Areas of NRI Capital Gains Tax Reporting in 2026

NRI capital gains tax reporting in India is an area where documentation and categorization make all the difference.

For listed equity shares and equity mutual funds:

- STCG (held < 12 months): Taxed at 20% flat (revised from 15% post-Budget 2024)

- LTCG (held ≥ 12 months, above ₹1.25 lakh): Taxed at 12.5% without indexation

For unlisted shares and property:

- STCG: As per slab rate

- LTCG: 12.5% without indexation (property) post-Budget 2024 changes

NRIs must also note that TDS is deducted by the buyer at source on property transactions typically at 20% + surcharge + cess. Filing ITR allows NRIs to claim a refund if actual LTCG tax liability is lower than the TDS deducted.

Smart NRI ITR Filing Strategy for AY 2026-27

Here’s a structured checklist that Dr. Haresh Adwani and the team at Adwani and Company recommend for every NRI preparing to file their ITR for AY 2026-27:

✅ Confirm residential status for FY 2025-26 based on actual days in India

✅ Select the correct ITR form : ITR 2 or ITR 3

✅ Download and reconcile AIS + Form 26AS before filing

✅ Declare all Indian income — interest, rent, dividends, capital gains

✅ Do NOT claim Section 87A rebate

✅ Compare old vs new tax regime based on actual deduction eligibility

✅ Verify all TDS credits reflected correctly for refund claims

✅ Validate Indian bank account (NRO/NRE) linked for refund credit

✅ Ensure correct Schedule CG, Schedule SI, and Schedule OS entries

Frequently Asked Questions

Q1. Which ITR form should an NRI file for AY 2026-27?

Most NRIs with interest, rental, dividend, or capital gains income should file ITR 2. If the NRI has intraday trading, F&O, or business income from India, ITR 3 is mandatory.

Q2. Is Section 87A tax rebate available to NRIs in 2026?

? No. Section 87A rebate is available only to resident individuals. NRIs are not eligible for this rebate regardless of income level or the tax regime chosen.

Q3. Do NRIs need to pay tax on NRE account interest?

Interest earned on NRE (Non-Resident External) accounts is exempt from Indian income tax as long as the individual maintains NRI status. NRO account interest, however, is fully taxable in India.

04. What happens if an NRI files the wrong ITR form?

Filing an incorrect ITR form results in a defective return notice under Section 139(9). The taxpayer is given 15 days to rectify the error. Failure to do so may result in the return being treated as not filed, with applicable penalties.

05. How can NRIs avoid refund delays in ITR filing 2026?

NRIs should validate their Indian bank account (preferably NRO) on the e-filing portal before filing, reconcile AIS and Form 26AS thoroughly, and ensure all TDS credits are correctly claimed in the ITR to avoid processing delays.

Conclusion :

NRI ITR filing in 2026 is not a form-filling exercise — it’s a tax strategy exercise. Every decision, from residential status declaration to ITR form selection, regime comparison, and capital gains reporting, has a direct financial impact.

The Income Tax Department has made it unambiguously clear through its compliance frameworks and AIS data infrastructure that NRIs are now under the same level of scrutiny as resident taxpayers. The difference is that NRIs have fewer automatic safeguards and must actively navigate a more complex set of rules.

Don’t let a procedural oversight cost you money or invite a notice from the Income Tax Department.

Author

CA Dipesh Gurubakshani is a Chartered Accountant with Adwani & Co LLP, Pune, specialising in income tax audit, direct taxation, and accounting advisory. He supports clients across statutory compliance, financial reporting, and income tax matters with a focus on accuracy, regulatory adherence, and disciplined execution.