ESOP Valuation India

Someone at your company just received an ESOP grant worth Rs. 50 lakh. They are delighted. They tell their spouse. They mentally earmark a part of it for a home loan prepayment. Two years later, at the time of exercise, they discover their actual tax outgo is Rs. 17 lakh. They had no idea that was coming. This is not a rare story. It plays out across Indian start ups and growth-stage companies every single year, precisely because ESOP valuation in India is widely misunderstood by employees, and often by the founders who grant the options.

This article is for every founder, CFO, start up leader, and salaried professional who wants to understand ESOP valuation in India properly: how it is determined, what the tax implications are, where governance failures happen, and how to protect both the company and its people.

What Is ESOP Valuation in India and Why Does It Matter?

An Employee Stock Option Plan (ESOP) gives an employee the right to buy company shares at a fixed exercise price typically a fraction of the actual market value after a vesting period. The gap between the Fair Market Value (FMV) of the shares on the date of exercise and the exercise price is what creates the financial benefit for the employee.

But here is what many miss: that same gap is also the taxable income. Under Section 17(2) of the Income Tax Act, 1961, this spread is classified as a perquisite and taxed as part of the employee’s salary in the year of exercise. This means the ESOP valuation in India is not just a philosophical question about company worth. It is a direct, quantifiable input into the employee’s tax liability and the company’s TDS obligation.

When the valuation is arbitrary, unsupported, or incorrectly determined, the consequences can be severe:

- Employees face unexpected and sometimes unaffordable tax demands on gains they have not yet liquidated.

- The company fails in its TDS deduction and deposit obligations under Section 192, exposing it to interest and penalties.

- Investors conducting due diligence question the integrity of the cap table and valuation history.

- SEBI, MCA, or the Income Tax Department may raise compliance objections during fundraising or assessments.

How Is ESOP Valuation Determined for Unlisted Companies in India?

For listed companies, the FMV of shares used in ESOP valuation is straightforward: it is the average of the opening and closing price on the recognised stock exchange on the date of exercise, as prescribed under Rule 3(8) of the Income Tax Rules, 1962.

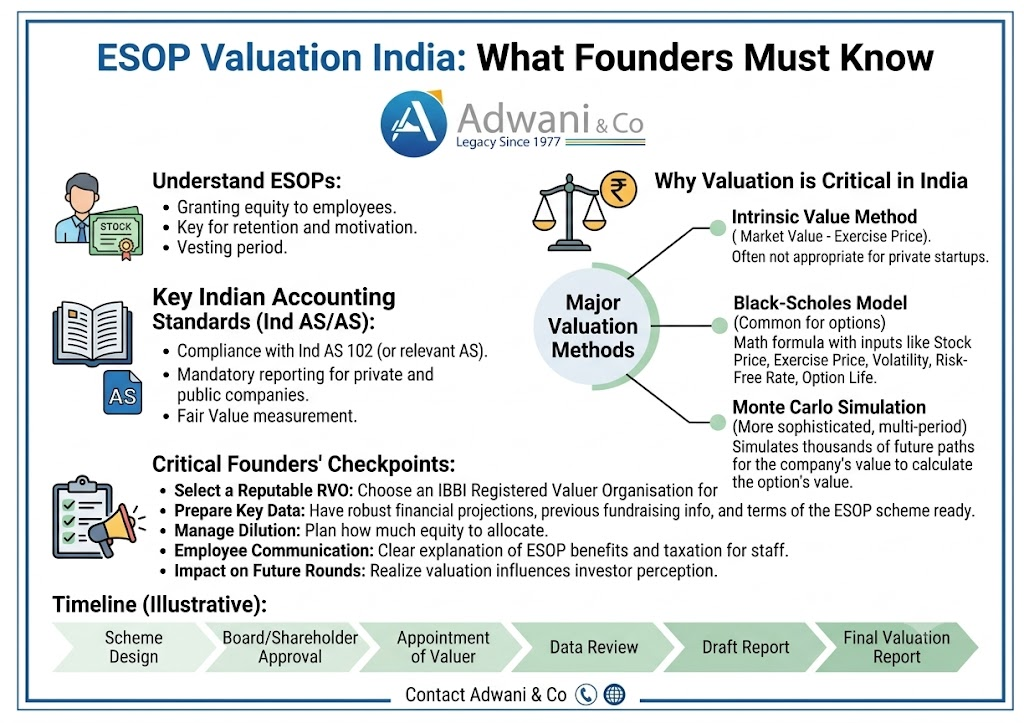

For unlisted companies which includes the overwhelming majority of Indian start ups the rules are more specific and more demanding. As per the Income Tax Rules, the FMV of shares of an unlisted company for ESOP purposes must be determined by a SEBI-registered Category I Merchant Banker. This is a statutory requirement, not a best practice suggestion. An internal valuation, a back-of-the-envelope calculation, or a valuation done by an unregistered consultant does not satisfy this requirement.

The Merchant Banker applies recognised ESOP valuation methods for unlisted companies, including:

- Discounted Cash Flow (DCF) Method: Projects the company’s future free cash flows and discounts them to present value using an appropriate discount rate. Most relevant for companies with established revenue and growth visibility.

- Comparable Company Multiples (CCM): Values the company using revenue, EBITDA, or GMV multiples of comparable listed peers or recently funded private companies in the same sector.

- Net Asset Value (NAV) Method: Based on the adjusted book value of the company’s assets minus liabilities. Generally applied to asset-heavy businesses, holding companies, or early-stage ventures where forward projections carry high uncertainty.

The choice of methodology and the assumptions underlying it must be defensible, documented, and consistent with the company’s stage, sector, and financial profile. Valuation reports that are vague, undated, or produced without a proper engagement letter from a qualified Merchant Banker will not withstand scrutiny.

Adwani and Company routinely advises founders on coordinating the valuation process, reviewing Merchant Banker reports for compliance gaps, and ensuring that the resulting FMV is correctly factored into payroll, TDS, and regulatory filings. For more tailored guidance, learn more about our Business Valuation and ESOP Structuring Services.

ESOP Tax Implications in India: Two Stages Every Employee Must Understand

The tax journey of an ESOP in India has two distinct stages. Understanding both is essential for financial planning — and for avoiding the kind of shock that ruins what should be a moment of wealth creation.

Stage 1: Perquisite Tax at Exercise

When an employee exercises their vested options, the Income Tax Department treats the FMV-minus-exercise-price spread as a perquisite under the head ‘Salaries’. This perquisite is added to the employee’s gross salary income for that year and taxed at the applicable slab rate, which can be as high as 30% plus surcharge and cess for high earners.

The employer is required to deduct TDS on this perquisite under Section 192. If the employer fails to deduct or deposit the correct TDS, both the employer and the employee face consequences: the employer is liable for interest under Section 201, while the employee’s ITR may be flagged for short payment.

One important relief for eligible startups: the Budget 2020 introduced a deferred TDS mechanism for employees of DPIIT-recognised startups. Under this provision, the TDS on ESOP perquisite tax can be deferred until the earlier of: 48 months from the end of the financial year of exercise, the date the employee sells the shares, or the date the employee ceases to be an employee. This is a meaningful cash-flow benefit for employees who may not have liquid funds to pay tax on paper gains. Founders should verify their DPIIT recognition status on the official startup India portal and communicate this benefit clearly to their teams.

Stage 2: Capital Gains Tax at Sale

When the employee eventually sells the shares, a second tax event occurs. The profit calculated as the sale price minus the FMV at the date of exercise (which was already taxed as a perquisite) is treated as capital gain.

For unlisted company shares, if the holding period from date of exercise to date of sale exceeds 24 months, the gain qualifies as Long-Term Capital Gain (LTCG), taxed at 20% with the benefit of indexation. Gains from shares held for less than 24 months are treated as Short-Term Capital Gains (STCG) and taxed at the applicable slab rate. For listed shares, the holding period threshold is 12 months, with LTCG above Rs. 1 lakh taxed at 10% under Section 112A without indexation.

ESOP Valuation in India: A Practical Numerical Example

The following illustration shows how ESOP valuation translates directly into tax liability for an employee of an unlisted startup. Assume an employee was granted 10,000 stock options at an exercise price of Rs. 10 per share. The Merchant Banker-certified FMV on the date of exercise is Rs. 500 per share. The employee later sells the shares at Rs. 600 per share after holding for 26 months post-exercise.

| Item | Amount (Rs.) |

| FMV on Date of Exercise | 500 per share |

| Exercise Price (Grant Price) | 10 per share |

| Taxable Perquisite Spread | 490 per share |

| Number of Options Exercised | 10,000 shares |

| Total Taxable Perquisite Income | 49,00,000 |

| Approximate Tax (at 30% slab + surcharge + cess) | ~17,00,000+ |

| Capital Gain if Sold Immediately at Rs. 600/share | 10,00,000 (Rs. 100/share gain) |

This example makes one thing clear: the FMV at exercise (the ESOP valuation output) is not a passive number. It is the anchor for a chain of financial and tax consequences that can run into crores for senior employees with large option pools. A well-supported, defensible valuation by a qualified Merchant Banker is not a compliance formality. It is a financial planning necessity.

ESOP Governance: Why a Credible ESOP Valuation Protects Your Company

Dr. Haresh Adwani, PhD in Commerce, law graduate, and founding partner of Adwani and Company, has observed across decades of advisory practice that the most avoidable ESOP problems in Indian companies arise not from bad intentions, but from insufficient process. Founders build real enterprise value. They design equity incentive programs with genuine generosity. But when the valuation underpinning those programs is not rigorously supported, the structural weakness creates risk at every subsequent milestone.

During a Series B due diligence, for instance, a new investor’s legal team will examine the ESOP pool’s valuation history. If grants at different points in time cannot be reconciled to defensible, dated Merchant Banker certificates, it raises questions about the company’s financial controls. Similarly, if the Income Tax Department initiates a scrutiny assessment of a senior employee’s return and the perquisite valuation is challenged, the company as the TDS deductor is directly implicated.

Dr. Adwani emphasises three non-negotiables for ESOP governance compliance in India:

- Every ESOP grant must be backed by a valuation report from a SEBI-registered Category I Merchant Banker, obtained before or at the time of grant, not retrospectively.

- The exercise price, vesting schedule, and grant date FMV must be clearly documented in the ESOP scheme and individual grant letters, with no ambiguity about which valuation report applies to which tranche of grants.

- TDS obligations at exercise must be computed correctly, deposited on time, and reflected accurately in Form 16 Part B issued to employees.

A credible ESOP valuation process, managed with the diligence that Adwani and Company brings to every client engagement, also strengthens investor confidence during fundraising. Investors who see a well-documented valuation history and a properly administered ESOP pool are more confident in the company’s governance culture and governance culture increasingly influences term sheets.

ESOP Valuation India: Common Mistakes Founders Must Avoid

Dr. Haresh Adwani has identified the following as the most frequently recurring ESOP errors in Indian startups and growth companies:

- Treating ESOP valuation as a one-time exercise. FMV must be determined at the time of each grant and each exercise event. A valuation report prepared three years ago does not serve as the FMV basis for today’s exercise.

- Using unqualified valuers. Only a SEBI-registered Category I Merchant Banker’s certificate is acceptable for unlisted company ESOP valuation under Income Tax Rules. An independent CA, investment banker, or internal finance team report does not meet the statutory standard.

- Failing to communicate tax implications to employees. Employees who understand the two-stage taxation — perquisite at exercise, capital gain at sale — make more informed decisions about when to exercise, how many shares to exercise, and whether to use the DPIIT deferral if available.

- Retrospective valuation. Producing a valuation certificate after the exercise date, backdated or otherwise, exposes the company to significant regulatory and tax risk. Valuation must precede or coincide with the exercise event.

- Ignoring the impact of recent funding rounds. A new funding round at a significantly higher valuation changes the FMV landscape for all employees yet to exercise. Companies should proactively communicate this to option holders.

Explore More With Adwani and Company

- Read our detailed guide on Business Valuation vs ESOP 409A Valuation: What Every Founder Must Understand

- Explore our Start up Advisory Service

Key Takeaways: ESOP Valuation India

- ESOP valuation in India directly determines the perquisite tax an employee pays at the time of exercising options this is not a formality, it is a financial event.

- For unlisted companies, FMV must be certified by a SEBI-registered Category I Merchant Banker no other valuation source is accepted under Income Tax Rules.

- Tax on ESOPs occurs at two stages: as a perquisite (salary income) at exercise, and as capital gains at sale.

- DPIIT-recognised startups can offer employees a TDS deferral on ESOP perquisite tax for up to 48 months from the year of exercise.

- Employers must correctly compute TDS under Section 192 at exercise and reflect it in Form 16 Part B failures expose both employer and employee to compliance risk.

Good ESOP governance supported by defensible, timely valuations strengthens investor confidence and protects company credibility during fundraising and due diligence.

Frequently Asked Questions on ESOP Valuation India

Q1. What is ESOP valuation in India and how does it affect my tax?

ESOP valuation in India determines the Fair Market Value of your company’s shares on the date you exercise your options. The difference between FMV and your exercise price is taxed as a salary perquisite under the Income Tax Act, directly impacting your income tax liability for that year.

Q2. Who is authorised to determine ESOP valuation for unlisted companies in India?

Only a SEBI-registered Category I Merchant Banker is authorised to certify the FMV of unlisted company shares for ESOP tax purposes under Income Tax Rules. Internal valuations or certificates from unregistered professionals do not meet the statutory standard and can be disallowed during tax scrutiny.

Q3. Can ESOP perquisite tax be deferred for startup employees in India?

Yes, employees of DPIIT-recognised eligible start ups can defer TDS on ESOP perquisite tax for up to 48 months from the financial year of exercise, or until they sell the shares or leave employment whichever is earlier. The employer must confirm DPIIT recognition and apply the deferral correctly in payroll.

Q4. What are the two stages of ESOP taxation in India?

The first stage is at exercise: the FMV-minus-exercise-price spread is taxed as salary income (perquisite) and TDS is deducted by the employer. The second stage is at sale: the profit above the FMV at exercise is taxed as capital gain long-term if held beyond 24 months for unlisted shares, short-term otherwise.

Q5. What ESOP valuation methods are used for unlisted Indian ?

The three most commonly applied methods are the Discounted Cash Flow (DCF) method, Comparable Company Multiples (CCM), and the Net Asset Value (NAV) approach. The Merchant Banker selects the most appropriate method based on the company’s business model, revenue stage, and sector

Q6. What happens if a company does not deduct TDS on ESOP perquisites?

If the employer fails to deduct or deposit TDS on ESOP perquisites under Section 192, the company is treated as an assessee in default and is liable to pay interest under Section 201 of the Income Tax Act. The employee may also receive notices for short payment of advance tax or self-assessment tax.

Conclusion: ESOP Valuation India Is a Governance Issue, Not Just a Tax Issue

The Rs. 50 lakh ESOP that surprises an employee at tax time is not a failure of the tax law. It is a failure of communication, process, and valuation governance. Founders who build extraordinary companies owe it to their teams and to their investors to build equally rigorous ESOP frameworks behind them.

ESOP valuation in India sits at the intersection of the Income Tax Act, the Companies Act, SEBI regulations, and FEMA (for companies with foreign participation). Getting it right requires more than a Merchant Banker’s certificate obtained at the last moment. It requires a structured approach: from the design of the ESOP scheme, to the documentation of each grant and exercise, to the TDS compliance at exercise, to the capital gains reporting at sale.

Dr. Haresh Adwani and the team at Adwani and Company have guided founders, CFOs, and senior employees through this process for decades. Whether you are structuring your first ESOP pool, reviewing an existing scheme for compliance gaps, or helping an employee understand their tax obligations at exercise, the expertise required is the same: deep knowledge of tax law, regulatory requirements, and the practical realities of equity compensation in the Indian context.

Don’t let a preventable valuation error undermine the enterprise value you have spent years building. The right guidance, at the right time, makes all the difference.

Get Expert ESOP Guidance from Adwani and Company

Whether you are a founder structuring your first ESOP pool, a CFO reviewing compliance gaps, or an employee planning to exercise options, Adwani and Company is ready to help.

Contact us: enquiries@adwaniandco.com | +91 7620 127 137 | adwaniandco.com

About the Author

Dr. Haresh Adwani

Ph.D. in Commerce | Law Graduate | Managing Partner, Adwani & Co LLP Dr. Haresh Adwani holds a Ph.D. in Commerce and is a qualified Law graduate with over two decades of hands-on experience in GST advisory, direct taxation, and statutory compliance for businesses across Pune and Maharashtra. As Managing Partner of Adwani & Co LLP a firm established in 1977 by Advocate N. T. Adwani Dr. Adwani has guided hundreds of

SMEs, startups, and corporates through India’s evolving tax landscape. He is a recognised advisor on GST compliance, company formation, and Virtual CFO services, and regularly

contributes to professional seminars and industry forums in Pune.

Disclaimer

The content in this article is intended for informational and educational purposes only. It does not constitute legal, financial, or professional advice. Readers should consult a qualified Chartered Accountant, tax advisor, or legal professional before making any decisions based on the information provided. Laws, rules, and regulations are subject to change; readers are advised to verify the current position with a professional advisor.