Nidhi Adwani June 2026 10 min read

Income Tax Notice After High Credit Card Spending

You paid off a large credit card bill. Life moved on. Then, months later, an income tax notice landed in your inbox or worse, on the Income Tax Portal. Your first instinct might be panic. Your second might be denial. But the truth is: this situation is far more common than most people realise, and it is almost always manageable provided you understand why it happened and how to respond correctly.

Credit card income tax notices are not arbitrary. They follow a precise, rule-based reporting system that the Income Tax Department has been running for years. The good news is that if your spending is genuinely funded by legitimate, declared income, there is nothing to fear. The process is about documentation and explanation not accusation.

Why Does the Income Tax Department Track Your Credit Card Spends?

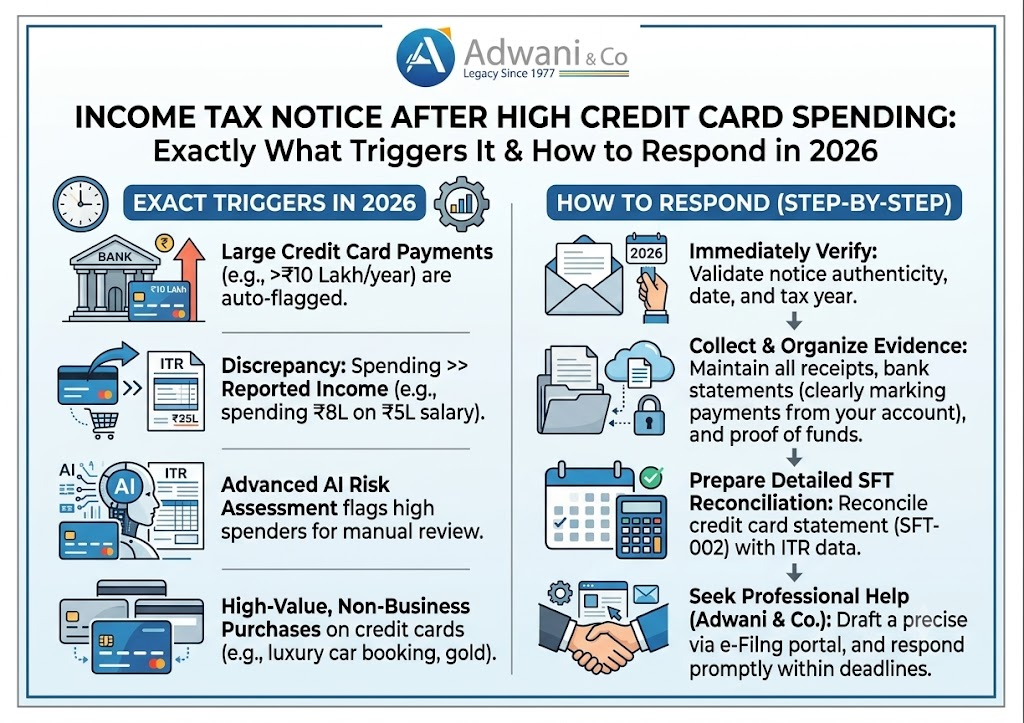

Under Rule 114E of the Income Tax Rules, 1962, banks and credit card companies are legally required to submit a Statement of Financial Transactions (SFT) to the Income Tax Department each year. This reporting captures high-value transactions across multiple financial categories including credit card payments.

Specifically, banks report credit card bill payments that meet either of these thresholds:

- Payment of ₹1 lakh or more in cash against a credit card bill in a single month

- Total credit card bill payments of ₹10 lakh or more in a financial year (by any mode online, NEFT, cheque, or cash)

Once reported, this data flows directly into your Annual Information Statement (AIS) on the Income Tax Portal. When the AIS data and your filed ITR don’t align when the spending pattern suggests a lifestyle that your declared income cannot support the system flags it for income tax scrutiny.

What Is an Annual Information Statement (AIS)? The AIS is a comprehensive tax passbook available on the Income Tax Portal (incometax.gov.in). It aggregates financial data about you from banks, mutual funds, registrars, and other reporting entities under Rule 114E. Checking your AIS before filing ITR is now considered a critical compliance step and any mismatch between your AIS and ITR can directly trigger a notice.

The Real Trigger: Income vs. Lifestyle Mismatch

Here is the core issue that most taxpayers miss. It is rarely the credit card spending itself that triggers a notice. It is the gap between the spending and the income you declared.

If you declared a net income of ₹8 lakh in your ITR but your credit card statements show annual spends of ₹15 lakh the Income Tax Department’s AI-powered systems will notice the inconsistency. This mismatch high-value spends relative to reported income is the primary trigger for credit card income tax scrutiny in 2026.

As Dr. Haresh Adwani of Adwani & Co LLP frequently highlights in client education sessions: the Income Tax Department today does not rely solely on manual checks. Faceless assessment tools powered by data analytics now cross-reference SFT filings, AIS entries, and ITR data automatically and flag outliers with remarkable precision.

High-Risk Transaction Thresholds at a Glance Credit card payment ≥ ₹10L/year: Reported under Rule 114E. Cash payment against CC bill ≥ ₹1L/month: Also reported. Savings account cash deposits ≥ ₹10L/year: Reported. Current account cash deposits ≥ ₹1 crore/year: Reported. All of this data lands in your AIS and is visible to the Income Tax Department.

Income Tax Notice Thresholds: What Gets Reported Under Rule 114E

| Transaction Type | Threshold / Mode | What Happens |

| Credit card bill payment ≥ ₹1 lakh/month | Cash mode | Reported under Rule 114E SFT |

| Credit card bill payment ≥ ₹10 lakh/year | Any mode | Reported under Rule 114E SFT |

| Cash deposit in savings account | ≥ ₹10 lakh/year | Auto-reported by bank |

| Cash deposit in current account | ≥ ₹1 crore/year | Auto-reported by bank |

| High-value spend vs. declared income mismatch | Any amount | AI-flagged for scrutiny / notice |

Types of Notices You May Receive for Credit Card Spending

Section 133(6) : Request for Information

This is the most common type notice received on Credit Card Spending. The Assessing Officer requests information or documents to verify a specific transaction or pattern. It is not a demand it is a query. Respond within the given time limit with supporting documents.

Section 148 : Reassessment Notice

If the income tax officer believes income has escaped assessment meaning you earned money that was not declared a reassessment notice may be issued under Section 148. This carries a defined income tax notice time limit: generally up to 3 years from the end of the assessment year for under-reported income up to ₹50 lakh, and up to 10 years for escaped income of ₹50 lakh or more.

Section 143(2) : Scrutiny Notice

If your ITR has been selected for detailed scrutiny, you will receive a notice under Section 143(2). Credit card income tax scrutiny under this section requires you to explain specific high-value transactions and submit documentation supporting your income claims.

Read our Detailed guide on Income Tax Notice Received?

How to Respond to an Income Tax Notice for Credit Card Spending

The response strategy depends on the notice type, but some principles apply universally:

- Do not ignore the notice : there are strict timelines and penalties for non-response

- Log in to the Income Tax Portal (incometax.gov.in) and check your AIS to understand exactly what was reported

- Gather credit card statements, bank statements, and salary slips or business income proofs for the relevant period

- Match the reported SFT amount with your actual payments sometimes figures are misreported or duplicated

- If the credit card spending was from savings accumulated over prior years, prepare documentation showing those savings

- If it was from gifts, inheritance, or exempt income, have written records in place

- Draft a factual, document-supported reply avoid vague responses

The Income Tax Department’s faceless assessment scheme processes most notices without face-to-face interaction. Every word and document in your response matters. A well-prepared reply often closes the matter at the information-request stage itself.

| ✅ Key Takeaways | |

| Rule 114E & SFT Reporting | Banks and card issuers report credit card payments ≥ ₹10 lakh/year (or ₹1L/month in cash) to the Income Tax Department under Statement of Financial Transactions. |

| Your AIS Reflects It All | Every high-value transaction appears in your Annual Information Statement (AIS) on the Income Tax Portal. Check it before filing your ITR. |

| Notice ≠ Guilt | Receiving an income tax notice for credit card spending is not an accusation — it is a request for explanation. Respond calmly with documentation. |

| Mismatch Triggers Scrutiny | The real risk is not the spend itself but the gap between your declared income and your lifestyle expenses visible through SFT data and AIS. |

| Faceless Assessment Is Real | The Income Tax Department uses AI-powered systems to flag high-value spends. Unexplained credit card bills can trigger faceless assessment proceedings. |

Frequently Asked Questions

Q1. What is the credit card limit that triggers an income tax notice in India?

Under Rule 114E, credit card bill payments totalling ₹10 lakh or more in a financial year are reported to the Income Tax Department. Cash payments of ₹1 lakh or more in a single month are also reported separately.

Q2. What is Rule 114E and how does it relate to credit card income tax scrutiny?

Rule 114E of the Income Tax Rules mandates that banks submit a Statement of Financial Transactions (SFT) covering high-value credit card payments. This data populates your AIS and can trigger scrutiny if it is inconsistent with your declared income.

Q3. Can I get an income tax notice even if I paid my credit card bill from savings?

Yes. The notice is triggered by the reported SFT data, not your source of payment. In your response, you simply need to show that the spending was funded by legitimate savings or income with documentary proof.

Q4. How much time do I have to respond to an income tax notice for credit card spending?

The income tax notice will specify a response deadline typically 15 to 30 days. Missing this deadline can result in ex-parte assessment or penalty. Always respond within the given timeframe.

Q5. Will the Income Tax Department also track UPI and WhatsApp payments in 2026?

UPI payments below ₹10 lakh annually are currently not subject to mandatory SFT reporting. However, large or unusual UPI patterns, especially those linked to business income, can still be flagged through AI-based analysis of financial data across platforms.

Conclusion:

Receiving an income tax notice for credit card spending is alarming but it is not the end of the road. The Indian tax system, now powered by AI-driven scrutiny and comprehensive AIS data, is designed to ensure alignment between lifestyle and declared income. If that alignment exists in your case, a well-prepared, timely response will resolve the matter.

The best long-term protection is not to spend less it is to file accurately, check your AIS before every ITR submission, and ensure your income declarations reflect your actual financial life. In the age of faceless assessments and Rule 114E SFT reporting, compliance is the only sustainable strategy.

About the Author

Nidhi Adwani is the Human Resources Manager at Adwani & Co. She is a Law Graduate and holds an MBA in Human Resources. She manages recruitment, employee engagement, team development, workplace culture, and the firm’s social media and content activities. Passionate about people and organizational growth, she also contributes articles for ITRAdvisor and Adwani & Co. Her writing focuses on HR practices, leadership, workplace engagement, and professional development, offering practical insights for professionals and businesses.

Legal Disclaimer: This article is published for informational and educational purposes only. Nothing contained herein constitutes legal, financial, or tax advice, nor should it be treated as a substitute for professional consultation tailored to your specific circumstances. Tax laws, rates, and provisions are subject to change; readers are strongly advised to consult a qualified Chartered Accountant or tax advisor before acting on any information in this article.

All content is original. References to government portals and statutory provisions are paraphrased for educational purposes in compliance with fair use principles. No content has been reproduced from third-party sources