CA Manish Mata June 2026 12 min read

Financial Model Assumptions

The model was technically perfect. The business was heading toward a cash crisis.

That sentence captures something that gets overlooked far too often in financial planning. A spreadsheet can balance to the last cent, carry every formula correctly, and project a healthy profit while the business it represents is quietly running out of cash. The issue is almost never the math. It is the assumptions sitting behind the math.

This is a reality that surfaces repeatedly when reviewing financial models, FP&A projections, and business planning documents across industries and geographies. The formulas are rarely the problem. The assumptions about when customers pay, how margins hold under pressure, and what working capital actually looks like in motion are where the real risk lives.

The Business Planning Model That Looked Right : And Wasn’t

Revenue Growth: 25% YoY ✓ Realistic target

Gross Margins: Stable ✓ Well-modelled

Cash Flow: Positive ✓ Projected green

Formulas: All correct ✓ No errors found

One assumption changed everything:

Customers paying: 45–60 days late

Suppliers due: Within 15 days Working Capital Gap: $1.2 million invisible in the model.

The $1.2 Million Gap That No Formula Would Catch

Consider a business planning model the kind prepared for investor review, internal planning, or board presentation that shows all the right signals: 25% year-on-year revenue growth, stable margins, positive cash flow projections, and zero formula errors. On paper, it is a credible, well-structured model.

But buried in the payment timing assumptions is a mismatch that the model never surfaces. Customers are taking 45 to 60 days to settle invoices. Suppliers expect payment within 15 days. That is a 30 to 45 day cash conversion gap and at the revenue volumes being projected, it translates to a working capital shortfall of nearly $1.2 million.

The business is profitable. The model is accurate. And yet, without intervention, the company will face a liquidity crisis at precisely the moment its revenue growth is accelerating. This is what happens when financial model assumptions are not stress-tested against operating reality.

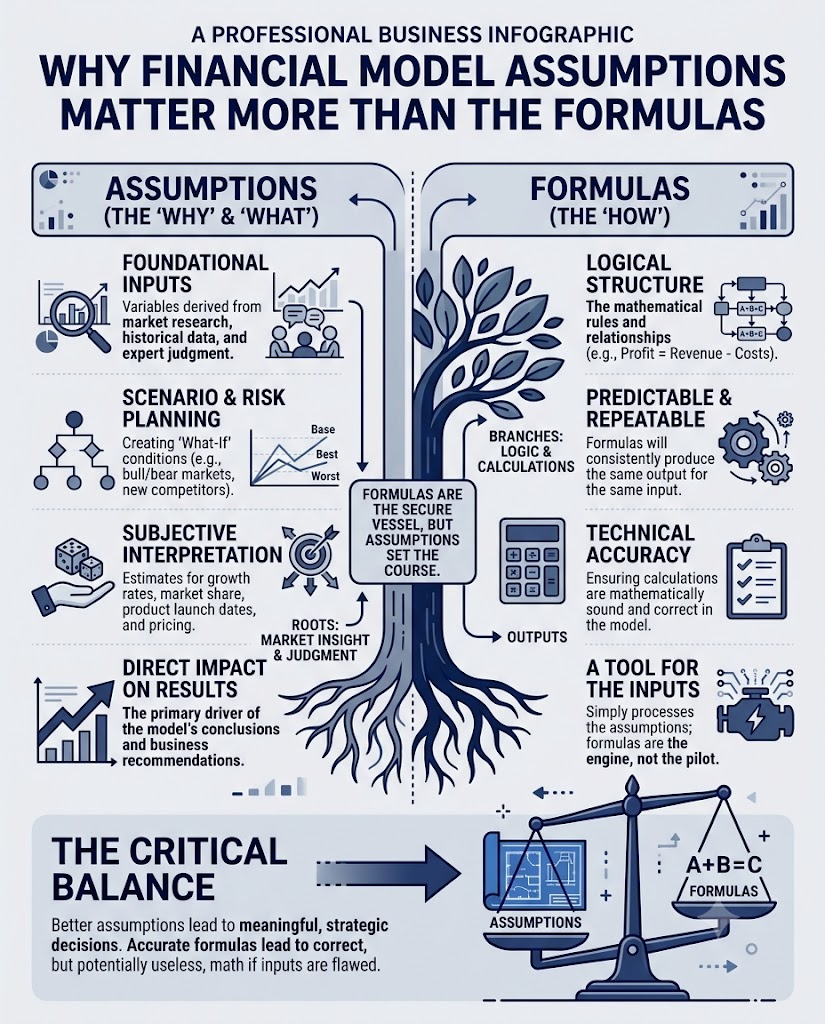

Why Assumptions Drive Model Outcomes : Not Formulas

There is a tendency, especially among founders and non-finance business leaders, to treat a financial model as primarily a technical exercise: build the structure, link the cells, check the formulas. If the spreadsheet calculates without errors, the model is assumed to be sound.

But financial modeling particularly FP&A modeling and business planning is fundamentally an exercise in judgment, not arithmetic. The formulas execute whatever logic you give them. The question is whether the logic reflects what the business actually does.

Three categories of assumptions carry the most risk in any business model:

1. Revenue Assumptions: Is the Growth Rate Grounded in Reality?

A 25% revenue growth projection is neither aggressive nor conservative in isolation it depends entirely on the assumptions underneath it. Is that growth coming from existing customers expanding, new customer acquisition, or a pipeline that has not yet converted? Is it weighted toward a single large contract or distributed across a customer base? Is pricing holding or is it declining to win volume?

Revenue assumptions that are disconnected from pipeline data, customer behavior, and market conditions are the most common source of model optimism. They project a trajectory that sales and operations cannot realistically support.

2. Working Capital Assumptions: What Does Cash Timing Actually Look Like?

Working capital is where most business models lose their grip on reality. The mechanics are straightforward Days Sales Outstanding (DSO), Days Payable Outstanding (DPO), and Days Inventory Outstanding (DIO) together define the cash conversion cycle. But getting these assumptions right requires looking beyond industry benchmarks to the actual payment behaviours of the specific customers and suppliers in the business.

A model that assumes DSO of 30 days for a business where customers routinely pay at 60 days will project working capital needs that are half of what the business actually requires. That gap invisible in the model shows up as a cash shortfall in operations, often at the worst possible time: during a growth phase when cash consumption is already elevated.

3. Margin Assumptions: Will Margins Hold When the Business Scales?

Stable margins in a financial model are a projection, not a guarantee. In practice, gross margins compress as businesses scale for several reasons: input costs increase, pricing becomes more competitive, volume growth requires additional delivery capacity, or the product mix shifts toward lower-margin offerings. A model that holds margins flat at current levels without a clear operational reason to do so is assuming away one of the most common sources of profitability risk.

The Five Questions That Separate Analysis from Arithmetic

When reviewing a financial model or FP&A projection, the structured review process typically works through five core questions. These questions are not about checking formulas they are about stress-testing the assumptions against commercial reality:

| Question | What It Is Testing | Common Risk If Ignored |

| Is revenue growth realistic? | Pipeline quality, market conditions, sales capacity | Overstatement of top-line performance |

| Will margins hold under pressure? | Cost structure, pricing power, operational efficiency | Profitability erosion at scale |

| What happens to cash if collections slow? | DSO sensitivity, working capital adequacy | Liquidity crisis during growth phase |

| Is working capital genuinely supportive? | Cash conversion cycle, DPO vs DSO mismatch | Hidden funding requirement in the model |

| Can the assumptions survive real conditions? | Scenario testing, operational alignment | Model optimism that fails at execution |

Working through these questions transforms the review from a technical check into what it should be: a business judgment exercise. The model becomes a tool for understanding the business, not just recording projections about it.

When Models and Reality Diverge: A Framework for Assumption Review

One of the consistent findings across financial model reviews is that the gap between model output and operational reality is rarely random. It tends to cluster around a few well-defined failure points. Understanding these points helps finance teams, founders, and advisors build more commercially grounded models from the outset.

| Common Assumption Failures DSO lower than actual customer behaviour Margin stability assumed without basis Headcount costs phased too optimistically Cap Ex timing misaligned with operations Revenue recognized before cash is received Supplier terms not matched to actual DPO | What Sound Assumptions Look Like DSO benchmarked against actual AR aging Margins stress-tested at lower price points Hiring plan tied to operational milestones Cap Ex schedule cross-referenced with ops Revenue phased with cash receipt timing Payment terms built from supplier contracts |

The discipline of assumption documentation explicitly stating what each key assumption is, where it comes from, and what happens if it moves by 10–20% is what separates a model built for decision-making from one built for presentation. Under US GAAP and IFRS reporting frameworks, the emphasis on substance over form is precisely this: financial information should reflect economic reality, not just technical compliance.

FP&A, AI Workflows, and the Irreplaceable Role of Commercial Judgment

Finance teams are increasingly working alongside AI-driven analytical tools, automated reporting workflows, and integrated FP&A platforms. These systems can process large datasets, identify variances, and surface anomalies faster than any manual review. But they operate on the assumptions they are given. They calculate with speed and precision whatever the model has been told to calculate.

The working capital gap in the scenario above would not be flagged by an automated system if the payment timing assumption was entered as 30 days instead of the 45 to 60 days that customers actually take. The system has no way to know the assumption is wrong. Only a reviewer with commercial context who has seen how businesses in this sector actually behave can identify the mismatch.

As CA Manish Mata observes from cross-border engagements at Adwani & Co LLP: “The models I review that require the most intervention are not the ones with broken formulas. They are the ones where every formula works perfectly, but the assumptions were set to show what the business hoped would happen rather than what is operationally likely. That gap is where financial analysis earns its value.”

What This Means for Founders, Finance Teams, and CPA Firms

Whether you are building a financial model for fundraising, preparing a board-level FP&A deck, or reviewing a client’s business planning projections, the practical implication is the same: the assumptions deserve as much scrutiny as the structure.

A few disciplines that make a tangible difference in practice:

- Document every key assumption explicitly. If it is not written down, it cannot be challenged or refined.

- Build a sensitivity table. Showing what happens to net profit and cash if DSO moves from 30 to 60 days, or if margins compress by 5%, gives decision-makers the context they need.

- Reconcile assumptions against operational data. AR aging reports, supplier payment records, and historical margin trends should directly inform the model not industry benchmarks alone.

- Separate revenue recognition from cash timing. Under both IFRS 15 and US GAAP ASC 606, revenue is recognized when performance obligations are met but cash collection timing can diverge significantly. Models should reflect both.

- Revisit assumptions quarterly. Business conditions change. A model built on assumptions that were reasonable six months ago may no longer reflect operating reality today.

Key Takeaways

- A financially accurate model can still misrepresent reality if the underlying assumptions are not commercially grounded.

- Working capital assumptions DSO, DPO, and the cash conversion cycle are the most common source of hidden risk in business planning models.

- A 25% revenue growth projection means very little without understanding the pipeline, pricing, and operational capacity behind it.

- Stress-testing assumptions (not just checking formulas) is what transforms a model into a genuine decision-making tool.

- AI-driven workflows and automated FP&A systems are only as reliable as the assumptions fed into them.

- The most valuable finance work is not spreadsheet construction it is the commercial judgment applied to the assumptions that determine what the spreadsheet calculates.

Frequently Asked Questions

1.What are financial model assumptions and why do they matter?

Financial model assumptions are the inputs — growth rates, payment timelines, margin percentages, cost behaviors — that determine what a model projects. They matter because even a technically perfect model produces misleading outputs if the assumptions are disconnected from commercial reality. In practice, assumption quality determines forecast reliability far more than formula accuracy does.

2.What is a working capital gap in a financial model?

A working capital gap occurs when the timing of cash outflows (paying suppliers, meeting payroll, servicing debt) runs ahead of cash inflows (collecting from customers). A financial model can project profitability accurately while missing this gap entirely if it uses idealized payment timing rather than actual customer and supplier behavior. The result is a business that is profitable on paper but cash-constrained in practice.

3.How should FP&A teams stress-test financial model assumptions?

Effective stress-testing typically involves building sensitivity tables that show how key outputs (net profit, cash balance, EBITDA) change when one or two critical assumptions move. Scenarios to test include slower revenue growth, margin compression of 5 to 10 percentage points, extended customer payment cycles, and capex overruns. The goal is not to predict the worst case but to understand the range of outcomes the business could realistically face.

4.Why do financial models often look better than the actual business performs?

The most common reason is assumption optimism — the tendency to model the scenario the business hopes will happen rather than the scenario that is operationally most likely. This shows up as revenue growth that outpaces pipeline reality, margins that hold flat despite scaling pressures, and working capital assumptions that ignore how customers actually pay. Addressing this requires deliberate assumption documentation and regular reconciliation against actual financial data.

5.What is the role of analytical review in financial modeling?

Analytical review is the process of interrogating whether financial data — modeled or actual — makes commercial sense. It involves comparing ratios, trends, and relationships across periods and against industry benchmarks, then asking why deviations exist. In financial modeling, analytical review is the discipline that catches assumption-driven errors before they translate into flawed business decisions or misleading investor presentations.

Conclusion

The gap between a technically accurate financial model and a commercially grounded one is almost always found in the assumptions. Revenue projections that do not reflect pipeline reality, working capital assumptions that ignore actual payment behaviours, margins held flat despite operational pressure these are the places where models quietly diverge from the businesses they are meant to represent.

That divergence is not a failure of Excel. It is a failure of the analytical discipline applied before the spreadsheet is opened: the discipline of asking hard questions about what the business actually does, how cash actually moves, and whether the projections describe a plausible future or a convenient one.

Financial modeling, at its best, is structured commercial judgment made visible. The formulas execute the logic. The assumptions determine whether that logic reflects reality. Getting the assumptions right is not a technical task it is the most important analytical work in the entire process.

| Looking to build stronger financial visibility for your business? The team at Adwani & Co LLP supports founders, SMEs, and accounting firms with: → Financial Modeling & FP&A Support → Virtual CFO & Management Reporting → P&L Review & Analytical Financial Services → International Accounting & Cross-Border Advisory → QuickBooks / Xero Bookkeeping & Cleanup To learn more, connect with Adwani & Co LLP at adwaniandco.com |

Author

CA. Manish R. Mata Practising In India (Ex PwC), At Adwani & Co LLP leads the International Accounting & Tax Support vertical, delivering structured execution assistance to US CPA firms and overseas businesses.

Disclaimer

Adwani & Co LLP is a multi-disciplinary professional services platform. The blogs shared are for educational and informational purposes only and are intended to promote awareness around finance, accounting, taxation, reporting, and business advisory topics. Nothing contained herein should be construed as solicitation or advertisement of professional services. Where professional services are required under applicable laws or regulations, such services are rendered in accordance with relevant professional and regulatory requirements. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP.