CA Manish Mata June 2026 9 min read

Financial Analysts P&L and FP&A Model

A person can live in one country, earn in another, invest in a third…

and still get their taxes wrong.

That is the reality of today’s world.

International taxation is no longer relevant only to multinational corporations.

Cross border transactions, overseas investments, remote work, global mobility, and NRI related matters have made international tax considerations a part of everyday professional practice.

Concepts such as DTAA, Tax Residency, Permanent Establishment (PE), Beneficial Ownership, Transfer Pricing, Foreign Asset Reporting, Equalisation Levy, and Global Minimum Tax are increasingly influencing business and investment decisions.

At Adwani & Co LLP, we have seen a growing need for advisory services relating to NRI taxation, returning Indians, foreign income disclosure, FEMA compliance, cross-border investments, and international reporting obligations.

As tax professionals, our role goes beyond understanding domestic tax laws.

We also need to stay updated with global tax developments so that we can provide practical and compliant solutions to clients operating across different countries.

One thing is becoming clear.

The future belongs to professionals who can combine strong local expertise with a global perspective.

Because in a world where people, businesses, and investments move across borders, tax knowledge cannot stop at the border.

What do you believe is the most challenging aspect of international taxation today?

The P&L scenario that changes everything:

Revenue: $500K → $600K (+20%)

Gross Margin: 65% → 55% (−10 pts)

Payroll % Rev: 28% → 38% (+10 pts)

Net Profit: $80K → $40K (−50%) Revenue grew. Net profit fell by half. What story is the P&L really telling?

The P&L Is Not an Accounting Report : It Is an Investigative Document

Most business owners treat the Profit & Loss statement as a summary: revenue in, expenses out, profit at the bottom. That is technically correct but practically limiting. A finance professional — particularly one working in FP&A or financial modeling reads a P&L the way a detective reads a case file: looking for patterns, inconsistencies, and early warning signals.

The scenario above makes this clear. A 20% jump in revenue looks encouraging on the surface. But strip away the top-line growth and you find a business that:

- Spent more to generate each dollar of sales (gross margin compression from 65% to 55%)

- Added payroll at a pace that outstripped revenue growth (payroll ballooned from 28% to 38% of revenue)

- Ended the month with a net profit that was half of what it was before the revenue increase

This is not a sign of a scaling business. It is a sign of a business that grew its top line while quietly eroding its underlying profitability. And without a structured P&L analysis, it would be easy to miss entirely.

Also Read :How Financial Modeling and FP&A Drive Smarter Cash Flow Decisions for Businesses

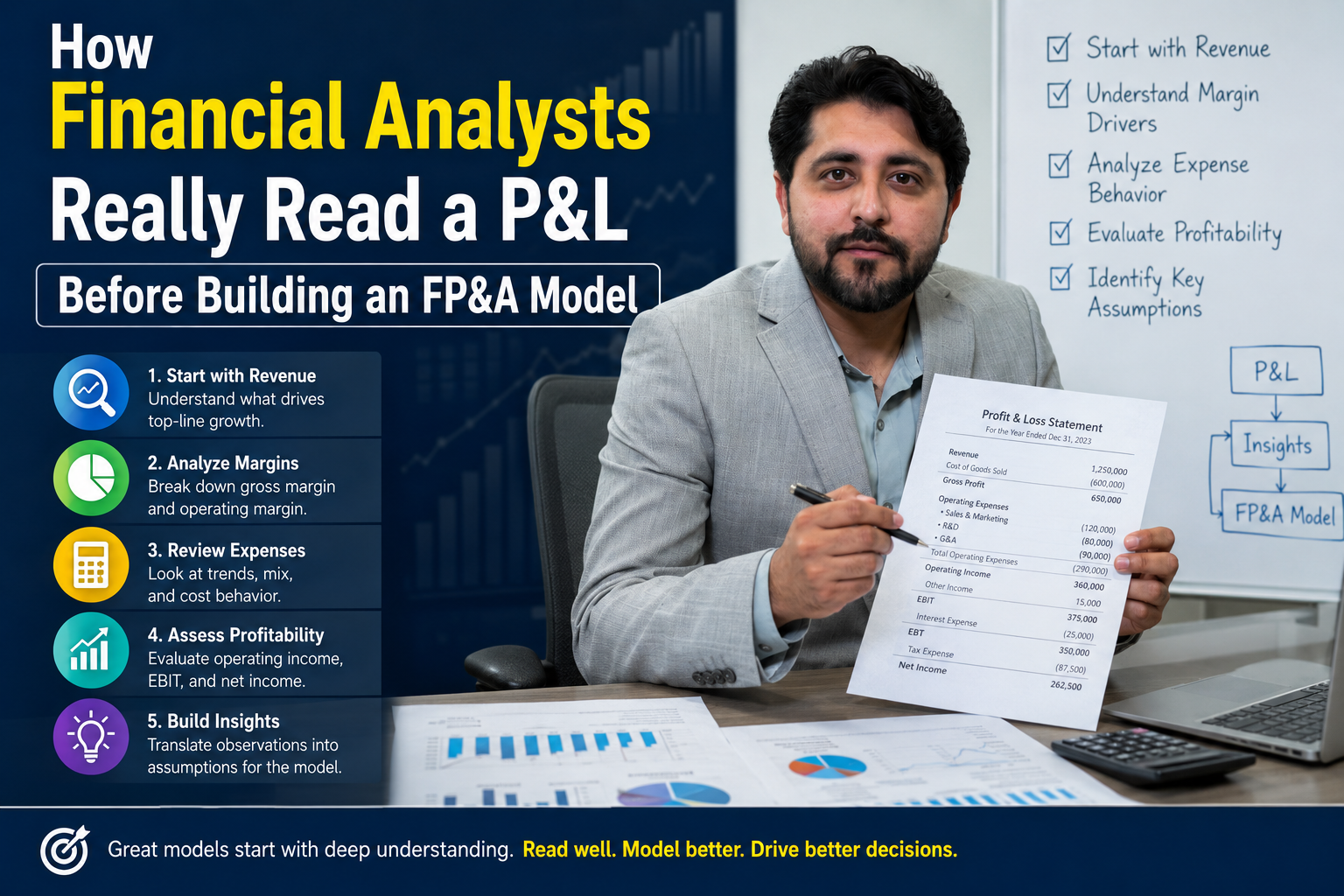

Five Questions Every Finance Professional Asks When Reading a P&L

Before building any FP&A model or financial forecast, the analytical review of the P&L typically centers on five foundational questions. These questions are deceptively simple but the answers reveal the actual health of the business.

1. Is Revenue Growth Actually Sustainable?

Top-line growth can come from many sources: a one-time contract, a seasonal spike, aggressive discounting, or a genuine shift in demand. A finance analyst looks at the composition of revenue not just the total. Are new customers driving this growth or is it from a single large client? Is pricing holding steady or declining? Is volume growth coming at the cost of margins?

These questions matter because unsustainable revenue growth can mask structural problems. In a P&L model, projecting that growth forward without understanding its source leads to forecasts that look optimistic on paper but fall apart in reality.

2. Are Direct Costs Growing Faster Than Sales?

Gross margin compression like the drop from 65% to 55% in the example above is one of the most important signals in any P&L review. It means the cost of delivering your product or service is growing faster than what you are charging for it. This can happen gradually: a supplier raises prices, delivery costs increase, or material waste goes untracked. Left unaddressed, gross margin erosion destroys profitability even in growing businesses.

3. Is Payroll Healthy Relative to Revenue?

Payroll as a percentage of revenue is one of the most reliable efficiency indicators in a P&L, especially for service businesses. In the scenario above, payroll climbing from 28% to 38% of revenue in a single month is a significant shift. It could reflect new hires ahead of a ramp-up, overtime costs, or a misalignment between headcount and output. In FP&A modeling, payroll ratios are often used as benchmarks against industry standards and internal targets.

4. Which Expense Line Is Quietly Eroding Profit?

P&L analysis is partly about finding the expense that does not announce itself loudly. Rent, software subscriptions, travel, contractor fees these often drift upward month over month without triggering an obvious alert. A structured review identifies which line items are growing disproportionately and traces them back to a business decision or oversight.

5. What Happens If These Trends Continue?

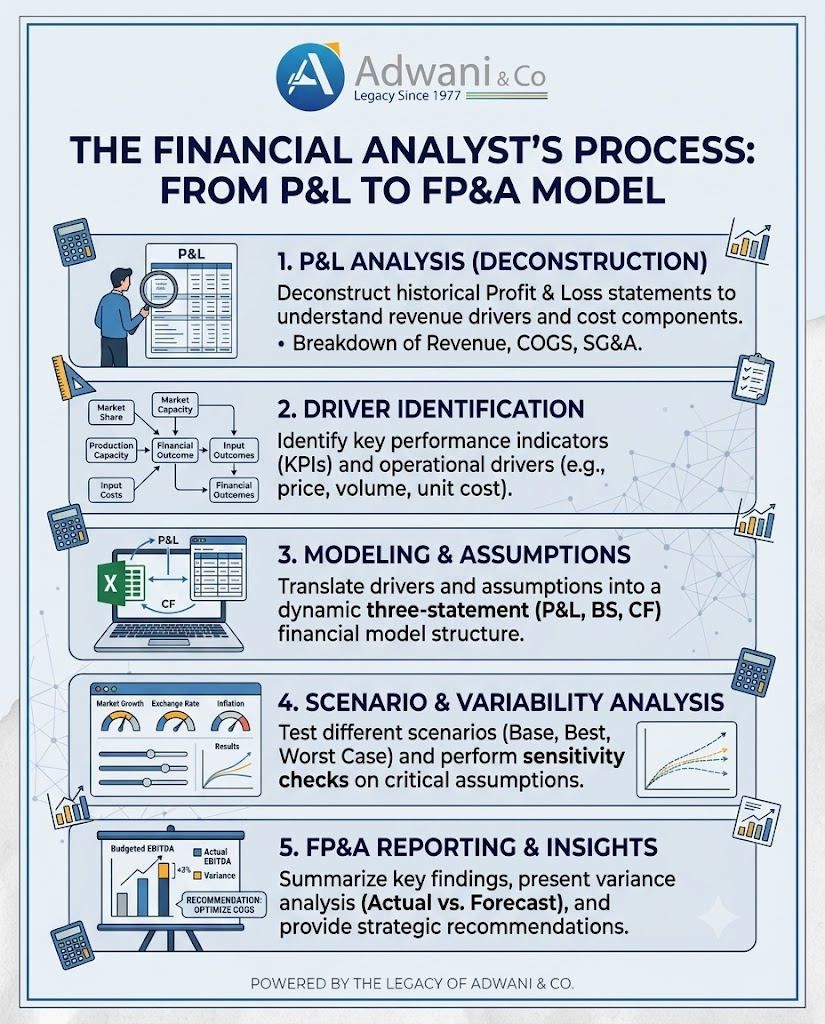

This is where P&L analysis transitions into FP&A. Once the current period’s numbers are understood, the logical next step is extrapolation: if gross margin continues compressing at the same rate, where will profitability be in three months? If payroll as a percentage of revenue keeps climbing, at what point does the business become loss-making? These forward-looking questions are the foundation of any financial model or management reporting framework.

Two Ways to Read the Same P&L: Accounting vs. Financial Analysis

| Accounting Lens Revenue recognised: $600K Total expenses recorded: $560K Net profit recorded: $40K Books are balanced. Filing is clean. Conclusion: Business operated profitably. | FP&A / Analytical Lens Revenue grew 20% but why? Gross margin fell 10 pts cost issue? Payroll ratio +10 pts overhiring? Net profit halved scalability concern. Conclusion: Business needs course correction. |

Both lenses are looking at the same set of numbers. The difference lies entirely in the questions being asked and what those questions reveal about the business’s trajectory.

Both lenses are looking at the same set of numbers. The difference lies entirely in the questions being asked and what those questions reveal about the business’s trajectory.

Why P&L Analysis Is the Foundation of Every FP&A Model

A financial model is only as reliable as the assumptions feeding it. And those assumptions come from a thorough reading of the P&L. Before building a forecast, projecting headcount costs, or stress-testing scenarios, an analyst needs to understand the underlying dynamics of the business: which revenue lines are sticky, which cost structures are variable, and which trends carry forward.

In practice, as CA Manish , Head Consultant for International Accounting and Financial Modeling at Adwani & Co LLP observes across client engagements: “The most common modeling mistake is projecting revenue and costs independently, without understanding how the two interact. When you read the P&L analytically first, you stop treating expenses as fixed rows in a spreadsheet and start seeing them as business behaviors. That shift changes everything about how you build a model.”

What This Means for Founders and Business Owners

You do not need to be a finance professional to benefit from this approach. But you do need to ask the right questions when you review your monthly P&L with your finance team or accountant.

A few practical habits that make a real difference:

- Review gross margin month over month not just the absolute profit figure

- Track payroll and key overhead lines as a percentage of revenue, not just in dollar terms

- Ask your finance team to flag any expense category that moved more than 2–3% relative to the prior period

- Do not treat a revenue increase as automatically positive always check whether it came with a margin cost

- Use the P&L as the starting point for your quarterly forecast review, not just as a historical record

If your business does not have a structured framework for reviewing its P&L analytically, building one is a practical first step toward stronger FP&A and financial decision-making.

Key P&L Ratios Every Business Should Monitor

| P&L Metric | Formula | Why It Matters |

| Gross Margin % | (Revenue − COGS) ÷ Revenue × 100 | Measures efficiency of core business operations |

| Payroll as % of Revenue | Total Payroll ÷ Revenue × 100 | Key efficiency benchmark, especially for service businesses |

| Operating Expense Ratio | Total OpEx ÷ Revenue × 100 | Tracks overhead efficiency as revenue scales |

| EBITDA Margin | EBITDA ÷ Revenue × 100 | Proxy for cash profitability before financing & tax |

| Net Profit Margin | Net Profit ÷ Revenue × 100 | Reflects true bottom-line profitability after all costs |

| Revenue Growth MoM / QoQ | (Current − Prior) ÷ Prior × 100 | Tracks revenue trajectory and growth quality |

| Cost of Revenue Growth vs. Revenue Growth | Compare % changes side by side | Flags gross margin pressure early |

Key Takeaways

- Revenue growth alone is not the metric to watch. Always evaluate it alongside gross margin and net profitability.

- Gross margin compression is one of the earliest warning signs in a P&L catching it early prevents structural damage.

- Payroll ratios are a reliable efficiency indicator and should be tracked as a percentage of revenue, not just in absolute terms.

- The purpose of P&L analysis is not just to understand what happened it is to anticipate what will happen next.

- Every FP&A model is built on the back of analytical P&L reading. Weak analysis leads to weak forecasts.

- Finance professionals ask the questions behind the numbers and that is the mindset founders need to adopt.

Frequently Asked Questions

01. What is the difference between reading a P&L as an accountant vs. a finance analyst?

An accountant’s primary concern is accuracy and compliance ensuring transactions are recorded correctly and the books balance. A finance analyst reads the same P&L looking for trends, ratios, and business signals: what is growing, what is shrinking, what is out of proportion, and what those patterns imply for the future. Both are important, but they serve different purposes.

02.Why does gross margin matter more than net profit in P&L analysis?

Gross margin reflects the fundamental profitability of your core business operations how efficiently you deliver your product or service. Net profit, while important, is influenced by many factors including financing costs, depreciation, and one-time items. A declining gross margin signals a structural cost problem that needs to be addressed at the operational level, which is why finance professionals treat it as a primary indicator.

03.What is FP&A and how does P&L review connect to it?

FP&A Financial Planning & Analysis encompasses budgeting, forecasting, financial modeling, variance analysis, and management reporting. A thorough P&L review is the first step in any FP&A cycle: it establishes the baseline understanding of business performance that all forecasting and planning activities build on. Without a clear analytical read of the P&L, FP&A models lack grounding in actual business dynamics.

04.How often should business owners review their P&L analytically?

At minimum, a structured P&L review should happen monthly — ideally within five to seven business days of the month-end close. For businesses with tighter cash cycles or faster-moving cost structures, a mid-month flash review of key metrics (gross margin, payroll ratio, major expense lines) adds an important layer of visibility. Quarterly reviews should include trend analysis across the trailing three months.

05.When does a P&L review translate into a financial model?

A P&L review becomes the foundation for a financial model when you move from understanding what happened to projecting what will happen. Once you have identified the key revenue drivers, cost behaviors, and margin trends in the P&L, those observations can be structured into a forward-looking model that supports forecasting, scenario planning, fundraising, or strategic decision-making.

Conclusion

A Profit & Loss statement is one of the most information-dense documents a business produces every month. But most of that information only becomes visible when you read it analytically — with the right questions, the right ratios, and the right frame of reference.

The ability to read a P&L not just as a historical record but as a forward-looking diagnostic tool is what separates financial analysis from bookkeeping. It is the starting point for FP&A, financial modeling, and every strategic conversation a business has about its own performance.

Whether you are a founder trying to understand your monthly numbers, a finance team building a forecast model, or a business looking to strengthen its reporting infrastructure — the P&L is where every serious financial conversation begins. The numbers are always there. The skill lies in learning to ask what they are trying to tell you.

| Looking to build stronger financial visibility for your business? The team at Adwani & Co LLP supports founders, SMEs, and accounting firms with: → Financial Modeling & FP&A Support → Virtual CFO & Management Reporting → P&L Review & Analytical Financial Services → International Accounting & Cross-Border Advisory → QuickBooks / Xero Bookkeeping & Cleanup To learn more, connect with Adwani & Co LLP at adwaniandco.com |

Author

CA. Manish R. Mata Practising In India (Ex – PwC), At Adwani & Co LLP leads the International Accounting & Tax Support vertical, delivering structured execution assistance to US CPA firms and overseas businesses.

Disclaimer

Adwani & Co LLP is a multi-disciplinary professional services platform. The blogs shared are for educational and informational purposes only and are intended to promote awareness around finance, accounting, taxation, reporting, and business advisory topics. Nothing contained herein should be construed as solicitation or advertisement of professional services. Where professional services are required under applicable laws or regulations, such services are rendered in accordance with relevant professional and regulatory requirements. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP.