Self-Invoice Under RCM

Most businesses are careful about paying GST on time. Far fewer are careful about the paperwork that proves it. Under the Reverse Charge Mechanism (RCM), the recipient not the supplier is responsible for paying GST on certain transactions. But there is a step many businesses quietly skip: issuing a self-invoice under RCM. It sounds like a minor formality. In an actual GST audit, it is often the difference between a smooth assessment and an uncomfortable notice.

This guide explains exactly what a self-invoice under RCM is, when it is required, how to prepare one correctly, and why treating it as an afterthought is one of the most common and most avoidable GST compliance mistakes businesses make.

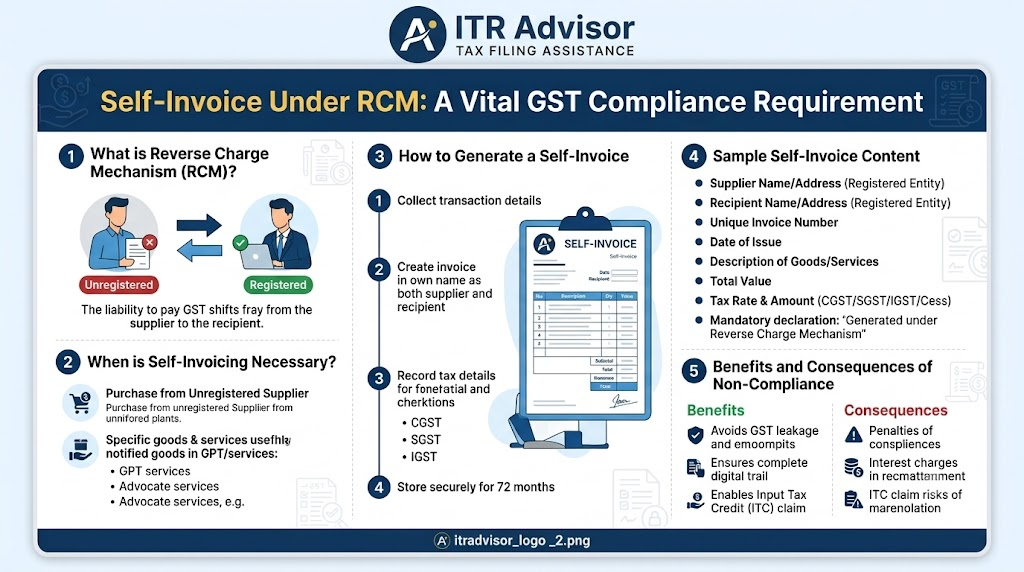

What Is a Self-Invoice Under RCM?

Under the Reverse Charge Mechanism, GST liability shifts from the supplier to the recipient of goods or services. This typically happens when the supplier is unregistered, or when the transaction falls under a category the government has specifically notified as subject to RCM.

Because the supplier in these cases usually cannot issue a valid tax invoice either because they are unregistered or because the law places the documentation obligation on the recipient GST law requires the recipient to raise their own document: a self-invoice under RCM. This self-invoice becomes the primary evidence that a taxable supply took place, that GST was correctly computed, and that the tax paid under reverse charge relates to a real, identifiable transaction.

In simple terms, paying RCM tax without a corresponding self-invoice under RCM is like paying a bill without keeping the receipt. The payment may be accurate, but the paper trail that proves it is incomplete.

Why the Self-Invoice Under RCM Requirement Exists

GST is fundamentally a documentation-driven tax system. Every rupee of tax paid or credit claimed needs to trace back to a valid document. The self-invoice under RCM requirement exists to close a specific gap: when the supplier cannot issue a compliant invoice, someone still has to create a record that satisfies the law’s documentation standard.

- It supports and substantiates the GST paid under reverse charge in your returns.

- It strengthens your documentation during GST audits, assessments, and departmental scrutiny.

- It helps maintain proper books of accounts that align with your GSTR-3B filings.

- It reduces the risk of compliance lapses, interest demands, and penalties for unsupported RCM claims.

Many businesses remember to pay the tax but forget the paperwork that substantiates the transaction. That gap is exactly where GST notices tend to originate not from unpaid tax, but from tax paid without adequate backing documentation.

When Do You Need to Issue a Self-Invoice for RCM Transactions?

A self-invoice under RCM is typically required in situations such as:

- Procurement of goods or services from an unregistered supplier where RCM applies to the transaction.

- Notified categories of supply where the law specifically places the tax and documentation obligation on the recipient.

- Any other RCM-applicable transaction where the supplier is not in a position to issue a valid GST-compliant tax invoice.

Businesses should not assume that paying tax under RCM in their GSTR-3B is sufficient on its own. The self-invoice under RCM is the underlying document that gives that tax payment legal and audit-ready support.

Real Example: How a Missing Self-Invoice Under RCM Creates Risk

Consider a manufacturing business that regularly hires local transport services from unregistered goods transport agencies. Over a financial year, it pays approximately ₹6,00,000 in freight charges and correctly deposits GST under RCM in its monthly GSTR-3B filings.

During a routine GST audit, the department asks for supporting documentation for each RCM payment. The business can show bank payment records and ledger entries, but has not issued a single self-invoice under RCM for any of these transactions. Without this document, the department raises a query on whether the underlying supply, value, and tax rate applied were correctly determined even though the tax itself was paid on time.

What could have been a routine audit turns into a documentation dispute, consuming time and inviting further scrutiny of other filings. Had a self-invoice under RCM been issued and maintained for every transaction, the audit response would have taken minutes rather than weeks.

What Should Your Self-Invoice Under RCM Include?

A compliant self-invoice under RCM should capture the same core details expected of any tax invoice, adapted to reflect that the recipient is issuing it on the supplier’s behalf:

| Field on Self-Invoice | What to Record |

| Recipient’s GSTIN and Address | Your own registered business details |

| Supplier’s Name and Address | Unregistered supplier details, even without a GSTIN |

| Invoice Number and Date | Sequential numbering as per your invoice series |

| Description of Goods/Services | Nature of supply received under RCM |

| Taxable Value and GST Rate | Value on which RCM liability is computed |

| Applicable GST (CGST/SGST/IGST) | Tax paid under reverse charge, matching GSTR-3B |

Maintaining this level of detail consistently not just for large transactions, but for every RCM-applicable purchase is what separates businesses with strong GST compliance from those exposed to audit risk.

Consequences of Skipping the Self-Invoice for RCM Transactions

Businesses that treat the self-invoice under RCM as optional paperwork often face avoidable consequences later:

- Difficulty substantiating RCM tax payments during departmental audits or assessments.

- Questions raised on Input Tax Credit (ITC) claimed against RCM payments without adequate backing documentation.

- Increased likelihood of a GST show cause notice where transaction values or classifications are disputed.

- Weakened defence position if turnover or expense figures are cross-verified against Income Tax Department or MCA filings.

Key Takeaways

A self-invoice under RCM is the primary document proving that GST paid under reverse charge relates to a genuine transaction.

It is required whenever the supplier is unregistered or cannot issue a valid GST-compliant invoice under a notified RCM category.

Paying RCM tax without a self-invoice under RCM leaves a business exposed during audits and assessments.

A proper self-invoice should record supplier and recipient details, invoice number, description, taxable value, and applicable GST. Consistent self-invoicing under RCM strengthens both compliance and ITC defensibility.

Why Professional Guidance on Self-Invoice Under RCM Matters

According to Dr. Haresh Adwani, PhD in Commerce and a law graduate with extensive experience in taxation and compliance law, “Businesses often treat RCM as a payment obligation alone. In reality, the self-invoice under RCM is what converts a tax payment into a defensible compliance record. Without it, even correctly paid tax can become a point of dispute during scrutiny.”

This is precisely the gap that Adwani & Co. helps businesses close. At Adwani & Co., every GST obligation from computing the correct RCM liability to issuing and maintaining the self-invoice under RCM is handled as part of a single, accurate compliance process, rather than as disconnected tasks split between payment and paperwork.

Dr. Haresh Adwani’s combined background in commerce and law is particularly relevant here, since disputes around RCM documentation often sit at the intersection of accounting practice and statutory interpretation exactly where a purely accounting-led approach can fall short.

Read our detailed guide on Complete GST Compliance Checklist for Small Businesses in Pune (FY 2026–27)

How GST Authorities Cross-Verify RCM Compliance

GST administration has moved well beyond manual return scrutiny. Authorities increasingly cross-reference GSTR-3B tax payments, e-way bill data, and Input Tax Credit claims to identify transactions where documentation appears inconsistent or incomplete. A self-invoice under RCM that is missing, backdated, or inconsistent with actual payment records is exactly the kind of gap that automated compliance checks are designed to flag.

Businesses should also ensure their RCM documentation remains consistent with figures reported to the Ministry of Corporate Affairs and reflected in their broader financial statements, since mismatches across regulatory filings tend to invite deeper scrutiny rather than isolated queries.

How Adwani & Co. Supports Businesses on Self-Invoice Under RCM Compliance

Adwani & Co. is a Pune-based Chartered Accountancy firm that works with businesses to ensure GST compliance is complete not just the tax payment, but the documentation that supports it. This includes identifying which transactions require a self-invoice under RCM, setting up systematic invoicing processes, and preparing businesses to respond confidently if a GST audit or assessment arises.

Rather than treating self-invoicing as a once-a-year clean-up exercise, Adwani & Co. helps businesses build it into routine monthly compliance, so that every RCM transaction is backed by a proper self-invoice under RCM from the moment it occurs.

Frequently Asked Questions on Self-Invoice Under RCM

1. Who is required to issue a self-invoice under RCM?

The recipient of goods or services is required to issue a self-invoice under RCM when procuring from an unregistered supplier or in other notified RCM-applicable transactions.

2. Is a self-invoice under RCM mandatory even if GST has already been paid?

Yes. Paying GST under RCM in your returns does not remove the requirement to issue a self-invoice under RCM as supporting documentation for that payment.

3. What happens if a business doesn’t maintain a self-invoice under RCM?

Missing self-invoices under RCM can weaken your position during a GST audit, raise questions on ITC eligibility, and increase the risk of a show cause notice.

4. Can Input Tax Credit be claimed on RCM transactions without a self-invoice?

ITC claims on RCM transactions are far more defensible when supported by a proper self-invoice under RCM; without it, credit claims may face challenge during assessment.

5. Does the self-invoice under RCM need to follow a specific format?

It should include the core details of a standard tax invoice supplier and recipient information, invoice number, description, taxable value, and applicable GST adapted since the recipient is issuing it.

6. How often should businesses review their RCM self-invoicing process?

Ideally every month, alongside GSTR-3B filing, rather than as an annual reconciliation exercise this keeps documentation current and audit-ready at all times.

Conclusion: Don’t Let a Missing Self-Invoice Undo Correct Tax Compliance

Paying GST under RCM is only half the compliance obligation. The self-invoice under RCM is what proves that payment was correctly calculated, properly documented, and tied to a genuine transaction. Businesses that treat this as a minor formality often discover its importance only when a GST audit forces the question. Building the self-invoice under RCM into your routine monthly compliance process is a small step that prevents a much larger problem later.

If you want expert guidance on RCM compliance, self-invoicing, or any aspect of your GST documentation, connect with Adwani and Company today.

About the Author

Nidhi Adwani is the Human Resources Manager at Adwani & Co. She is a Law Graduate and holds an MBA in Human Resources. She manages recruitment, employee engagement, team development, workplace culture, and the firm’s social media and content activities. Passionate about people and organizational growth, she also contributes articles for ITRAdvisor and Adwani & Co. Her writing focuses on HR practices, leadership, workplace engagement, and professional development, offering practical insights for professionals and businesses.

Legal Disclaimer: This article is published for informational and educational purposes only. Nothing contained herein constitutes legal, financial, or tax advice, nor should it be treated as a substitute for professional consultation tailored to your specific circumstances. Tax laws, rates, and provisions are subject to change; readers are strongly advised to consult a qualified Chartered Accountant or tax advisor before acting on any information in this article.

All content is original. References to government portals and statutory provisions are paraphrased for educational purposes in compliance with fair use principles. No content has been reproduced from third-party sources