Dr. Haresh Adwani

ITR Filing Mistakes

Filing an income tax return can take fifteen minutes. Fixing one of the common ITR filing mistakes hidden inside that return can take fifteen months. That gap between how quickly a return gets filed and how long a single error can take to resolve is where most taxpayers get caught off guard. A return that is “filed successfully” is not the same as a return that is filed correctly, and the difference between the two often shows up only after a notice lands in your inbox.

Why ITR Filing Mistakes Are More Common Than You Think

Most people assume that once the income tax portal accepts a return and generates an acknowledgement, the job is done. In reality, acceptance only confirms that the form was submitted in the correct format not that every figure in it is accurate or complete. This is exactly where ITR filing mistakes slip through unnoticed, sometimes for months.

A return can sail through the initial filing stage and still carry an error serious enough to trigger scrutiny later. The income tax system today is far more interconnected than it used to be, cross-checking your return against your Annual Information Statement (AIS), Form 26AS, bank reporting, and data from other government sources. A mismatch that may have gone unnoticed a few years ago is now far more likely to be flagged.

A Real Case: How One ITR Filing Mistake Spiraled Into Months of Follow-Up

Consider a case our team reviewed recently. A taxpayer believed everything was in order the return had been filed, the acknowledgement was generated, and there was no reason to expect a problem. The issue was simple on the surface: income from one source had not been reported correctly.

The return was accepted initially. But weeks later, a notice was issued. Interest on the unpaid liability kept accumulating. The expected refund was withheld. What should have taken a few minutes to correct at the filing stage instead turned into months of back-and-forth, with the taxpayer submitting multiple explanations and clarifications before the matter could be closed.

This is not an isolated story. It is one of the most common patterns we see, and it illustrates why ITR filing mistakes deserve far more attention than they typically receive before the “Submit” button is clicked.

The Most Common ITR Filing Mistakes Taxpayers Make

Understanding where errors typically occur is the first step toward avoiding them. Based on patterns observed across hundreds of filings, these are the ITR filing mistakes that appear most frequently:

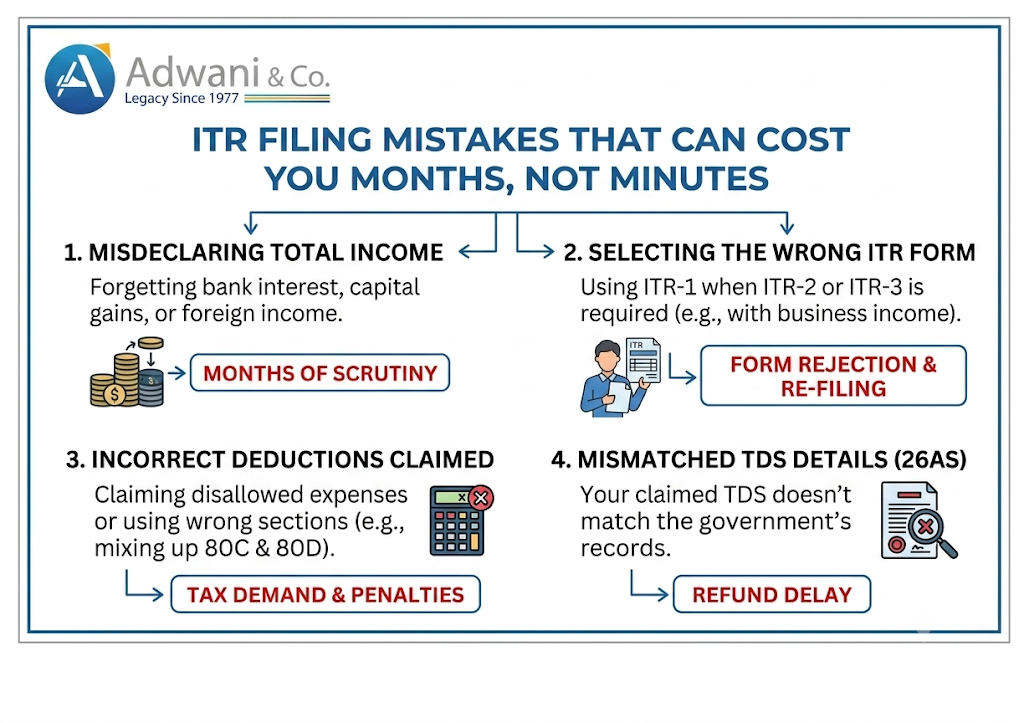

1. Underreported or Unreported Income

Interest from savings accounts, fixed deposits, freelance income, or income from a secondary employer is often left out — not deliberately, but simply because it was overlooked. Since this income is usually already visible in your AIS or Form 26AS, omitting it is one of the fastest ways to attract a notice.

2. Selecting the Wrong ITR Form

Choosing between ITR-1, ITR-2, ITR-3, or ITR-4 depends on your sources of income, residential status, and whether you hold capital assets or foreign income. Filing under the wrong form is a structural ITR filing mistake that can render the return defective.

3. Mismatch Between Return and AIS/Form 26AS

The income tax department’s systems automatically compare what you declare against what is reported by banks, employers, and other deductors. Even a small discrepancy between your return and your AIS can be enough to trigger a system-generated query.

4. Unsupported or Incorrect Deductions

Claiming deductions under sections like 80C, 80D, or 80G without valid supporting documentation is a frequent and easily avoidable error. If a deduction cannot be substantiated later, it can result in disallowance along with interest.

5. Missing Capital Gains or Foreign Asset Disclosures

Sale of mutual funds, shares, or property must be reported with proper computation, even if the resulting tax is minimal. Similarly, foreign bank accounts, foreign income, or overseas assets carry mandatory disclosure requirements that are frequently missed, particularly by first-time filers.

Submit

A few extra minutes of review before filing can prevent most ITR filing mistakes from happening in the first place. Before you submit your return, check the following:

- Is all your income reported including interest, freelance earnings, and any secondary income?

- Have you selected the correct ITR form based on your income sources and residential status?

- Are your deductions backed by valid documents you can produce if asked?

- Does your return match the figures in your AIS and Form 26AS?

- Have you disclosed capital gains, foreign assets, or other reportable income, if applicable?

Filing an Income Tax Return is not just about submitting a form. It is about submitting the right information, in the right form, supported by the right documentation.

Why ITR Filing Mistakes Lead to Notices, Interest, and Penalties

The income tax authorities increasingly rely on automated data matching to identify inconsistencies between filed returns and information already available to them. Updates and compliance guidance published through the official Income Tax Department portal make clear that the AIS and Form 26AS are central to this verification process, which means even small ITR filing mistakes are increasingly likely to be detected rather than overlooked.

Once a mismatch is flagged, the consequences typically unfold in stages: a system-generated notice is issued, interest begins accruing on any shortfall in tax paid, and in cases involving high-value discrepancies, the matter can escalate toward a formal tax demand. For taxpayers with significant income or transactions, the financial exposure from unresolved ITR filing mistakes can run into substantial amounts depending on the nature and scale of the discrepancy.

This is precisely why proactive review rather than reactive correction is the more sustainable approach to tax compliance.

As Dr. Haresh Adwani often points out to clients, the cost of a thirty-minute review before filing is almost always lower than the cost of resolving a notice after the fact.

How Adwani and Company Helps You Avoid ITR Filing Mistakes

Avoiding ITR filing mistakes consistently requires more than just software that auto-fills a form. It requires a professional review that understands how income, deductions, capital gains, and disclosures interact within the law. At Adwani and Company, returns are reviewed against your AIS, Form 26AS, and supporting documents before filing, not after a notice arrives.

Dr. Haresh Adwani, who holds a Ph.D. in Commerce and is also a law graduate, leads this approach by combining technical taxation knowledge with legal interpretation a combination that matters when a return involves nuanced questions around capital gains classification, clubbing provisions, or disclosure requirements. This dual expertise is particularly valuable when an ITR filing mistake has already triggered departmental correspondence and requires a legally sound, well-documented response.

For salaried individuals, freelancers, and business owners alike, the firm’s review process is built around the same five checks outlined above, applied systematically rather than left to last-minute judgment. Learn more about our ITR Filing Services

If a notice has already been received, read our detailed guide on responding to income tax notices for a structured approach to drafting an accurate, well-supported reply.

Under Ministry of Corporate Affairs and GST Portal frameworks, regulatory data increasingly flows between systems, reinforcing why consistency across all your filings not just your income tax return matters more than ever for taxpayers and business owners.

Read our detailed guide on ITR Filing 2025-26: Which ITR Form Is Right for You?

Dr. Haresh Adwani’s guidance has helped many clients catch ITR filing mistakes before submission rather than after a notice, which remains the most cost-effective way to stay compliant.

Frequently Asked Questions

What are the most common ITR filing mistakes that lead to a notice?

The most frequent causes are unreported interest income, mismatches between your return and your AIS or Form 26AS, incorrect ITR form selection, unsupported deductions, and missing capital gains or foreign asset disclosures.

Can a small ITR filing mistake really result in a tax notice?

Yes. Since income tax systems cross-verify returns against AIS, Form 26AS, and third-party reporting, even a small unreported amount can trigger an automated mismatch notice.

How do I check if my ITR matches my AIS and Form 26AS?

You can download your AIS and Form 26AS from the income tax e-filing portal and compare each entry against the income and TDS figures reported in your return before submission.

What happens if I already filed my return with a mistake?

Depending on the stage of filing, you may be able to file a revised return before the applicable deadline. If a notice has already been issued, a documented and professionally drafted response is typically required.

Which ITR form should I use to avoid filing mistakes?

The correct form depends on your income sources, residential status, and whether you have capital gains, business income, or foreign assets. Using the wrong form is itself considered a filing defect.

Can Adwani and Company help if I have already received an income tax notice?

Yes. The firm reviews the notice, reconciles it against your AIS, Form 26AS, and supporting documents, and helps prepare a structured response within the applicable deadline.

Conclusion: Don’t Let a Small Mistake Become a Long Problem

Filing your return quickly feels efficient — right up until an ITR filing mistake turns into a notice, a withheld refund, or months of correspondence over an amount that could have been reported correctly the first time. The taxpayers who avoid this outcome are not necessarily the ones with the simplest returns; they are the ones who review before they submit.

A few extra minutes spent checking your income, your form selection, your deductions, and your AIS reconciliation today can save months, or even years, of unnecessary stress tomorrow.

| Get Your ITR Reviewed Before You File If you are unsure whether your return has been reported correctly, a quick professional review today can help avoid a much bigger problem later. Connect with Adwani and Company for a thorough pre-filing review, or reach out if you have already received a notice and need expert guidance on how to respond. |

About the Author

Dr. Haresh Adwani

Ph.D. in Commerce | Law Graduate | Managing Partner, Adwani & Co LLP Dr. Haresh Adwani holds a Ph.D. in Commerce and is a qualified Law graduate with over two decades of hands-on experience in GST advisory, direct taxation, and statutory compliance for businesses across Pune and Maharashtra. As Managing Partner of Adwani & Co LLP a firm established in 1977 by Advocate N. T. Adwani Dr. Adwani has guided hundreds of

SMEs, startups, and corporates through India’s evolving tax landscape. He is a recognised advisor on GST compliance, company formation, and Virtual CFO services, and regularly

contributes to professional seminars and industry forums in Pune.

Disclaimer

This article is intended for general informational purposes only and does not constitute professional tax, financial, or legal advice. While every effort has been made to ensure accuracy as of the date of publication, tax laws, forms, and procedures are subject to change. Readers should consult a qualified chartered accountant or tax professional before making decisions based on this content. Adwani and Company accepts no liability for actions taken solely on the basis of this article.

© 2026 Adwani and Company. All rights reserved.

Content published via ITRAdvisor.in, a tax education and compliance initiative of Adwani and Company.