By Dr. Haresh Adwani, PhD (Commerce), Law Graduate, Adwani and Company

Received a GST notice under Section 73? Don’t panic. Section 73 of the CGST Act, 2017 deals with cases where tax has not been paid, short paid, or input tax credit (ITC) has been wrongly

availed but without any intention of fraud or wilful misstatement. These are routine tax demand notices and can be resolved smoothly with the right response. This complete 2026 guide walks you through everything: what the notice means, when it is issued, the time limits, a step-by-step reply process, required documents, penalties for ignoring it, and answers to the most common questions taxpayers ask.

What’s in This Guide

- What is a Section 73 GST Notice?

- When is it Issued? (With scenario table)

- Time Limits to Reply — Key Deadlines

- Step-by-Step Reply Process (7 Steps)

- Documents Required

- What is a Section 73 GST Notice?

- Penalties if You Ignore the Notice

- 7 FAQs Answered by CA Experts

- Case Study: How Adwani & Co Saved a Client

What is a GST Notice Under Section 73?

Legal Definition: Section 73 of the CGST Act, 2017 empowers a proper officer to issue a show cause notice (SCN) to a registered taxpayer when tax has not been paid, has been short-paid, erroneously refunded, or when ITC has been wrongly availed or utilised without any element of fraud or intentional misstatement.

In plain terms: the GST department has identified a mismatch or gap in your returns/tax payment, and they want you to explain or pay up without accusing you of fraud (that would be Section 74).

When is a Section 73 Notice Issued?

The GST officer may issue a Section 73 notice in any of these situations:

| Scenario | Common Reason | Risk Level |

| GSTR-3B vs GSTR-2A/2B mismatch | ITC claimed but not reflected in supplier’s data | Medium |

| GSTR-1 vs GSTR-3B mismatch | Output tax declared in GSTR-1 but not paid | Medium |

| Short payment of tax | Tax due > tax deposited | Medium |

| Excess ITC claimed | ITC beyond eligible limit claimed | High |

| Erroneous refund | Refund granted but conditions not met | High |

| Non-payment by unregistered person | Tax liability exists but GST not paid | High |

| Annual return discrepancy | GSTR-9/9C data doesn’t match returns | Medium |

Time Limits — What You Must Know

Understanding time limits under Section 73 is critical. Missing a deadline converts a manageable notice into a serious penalty situation.

| Action | Time Limit | Consequence if Missed |

| Voluntary payment BEFORE SCN | Anytime before SCN is issued | No SCN issued; no penalty |

| Payment after SCN but within 30 days | Within 30 days of SCN | No penalty payable |

| Reply / Show Cause response | As stated in notice (usually 30 days) | Ex-parte order passed against you |

| Officer’s order issuance (DRC-07) | Within 3 years from the due date of annual return | N/A — legal deadline for officer |

| SCN issuance deadline | At least 3 months before order deadline SCN can be challenged as time-barred | SCN can be challenged as time-barred |

| Appeal against order | 3 months from date of order | Forfeiture of appeal right |

Important 2026 Update: The Finance Act 2024 extended the time limit for issuance of orders under Section 73 for FY 2018-19 to FY 2021-22. If you receive a notice for these years now, it is still valid. Always verify the notice date and consult a CA immediately.

Received a notice and unsure of your deadline? (Consult Adwani & Co — Get Expert Review in 24 Hours)

Also Read https://www.adwaniandco.com/blog/gst-show-cause-notices

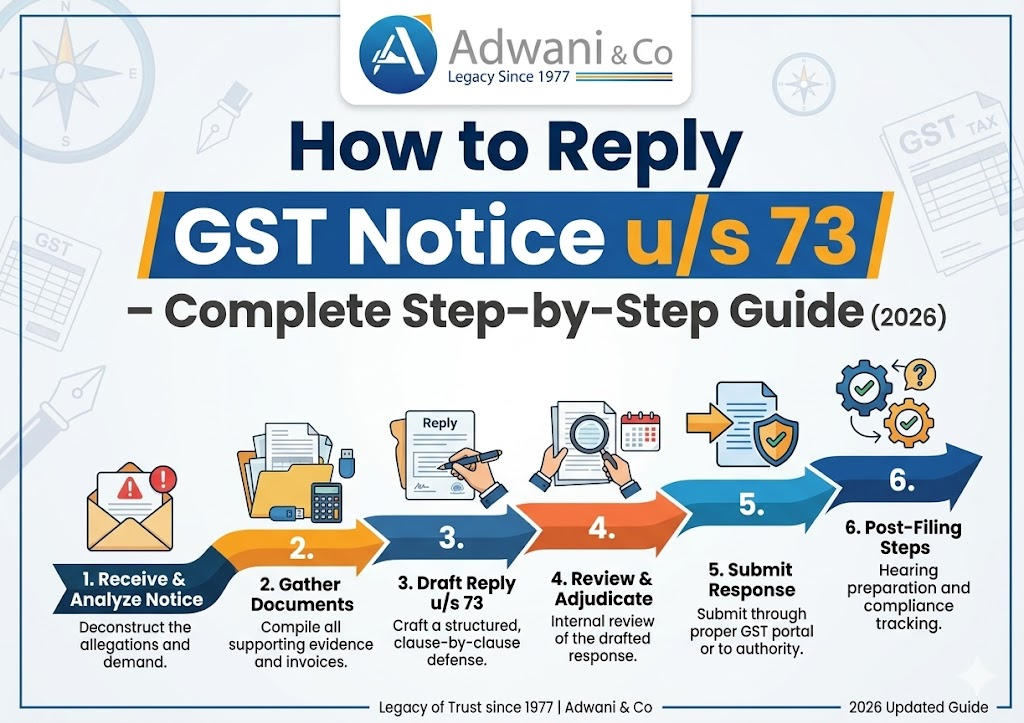

Step by Step: How to Reply to GST Notice u/s 73

Step 1: Read the Notice Carefully (DRC-01)

Identify the financial year, the tax period, the amount demanded (CGST/SGST/IGST/Cess separately), the reason for notice, and the response deadline. Check if it is a SCN (Show Cause Notice) or a pre-SCN intimation (DRC-01A).

Step 2: Analyse the Discrepancy

Download your GSTR-1, GSTR-3B, GSTR-2A/2B, and GSTR-9 for the relevant period. Cross check the department’s claim against your own records. Identify whether the demand is correct, partially correct, or incorrect.

Step 3: Decide Your Response Strategy

Three options:

(a) Accept the demand and pay — no penalty within 30 days of SCN

(b) Partially agree — pay agreed portion and contest the rest

(c) Fully contest — file a detailed reply with supporting documents

Step 4 : Prepare Your Reply (GST Notice Reply Format)

Draft a point-by-point reply addressing each allegation in the SCN. Refer to the specific paragraph numbers in the notice. Use DRC-06 form for filing the reply on the GST portal.

Attach all supporting documents and a clear reconciliation statement.

Step 5 : File the Reply on GST Portal

Log in at gstin.gov.in → Services → User Services → View Notices and Orders → Click on the relevant notice → Submit reply using DRC-06. Attach documents (PDF, max 5MB each).

Preserve the ARN (Acknowledgement Reference Number) after submission.

Step 6 : Attend Personal Hearing (If Called)

If the officer schedules a personal hearing, attend it (or send an authorised representative). Carry original documents and a point-wise argument sheet. Request adjournments in writing via the portal if needed.

Step 7 : Track the Order & Take Next Steps

After hearing, the officer issues DRC-07 (Demand Order). If the order is in your favour no further action needed. If you disagree with the order, file an appeal before the Appellate Authority (GST APL-01) within 3 months.

Documents Required to Reply to Section 73 Notice

- GSTR-1 for the relevant period

- GSTR-3B for the relevant period

- GSTR-2A / 2B reconciliation statement

- GSTR-9 (Annual Return)

- Purchase invoices (basis for ITC claimed)

- Sales invoices for the disputed period

- Bank statements

- Previous hearing orders (if any)

- Supplier correspondence (if disputing ITC)

- E-way bills (if applicable)

- Books of accounts / ledgers

- CA-certified reconciliation statement

Pro Tip: Always submit a reconciliation statement along with your reply even if the officer didn’t specifically ask for it. It demonstrates good faith and helps resolve the matter faster.

Penalties if You Ignore the GST Notice u/s 73

Do NOT ignore a Section 73 notice. Here is what happens:

| Situation | Penalty / Consequence |

| No reply filed within stipulated time | Ex-parte order passed; demand confirmed automatically |

| Demand confirmed via DRC-07 | Interest @ 18% p.a. on unpaid tax + 10% penalty |

| Ignoring confirmed demand | Recovery action: bank attachment, asset seizure |

| Non-payment after order | Certificate issued to Tax Recovery Officer; property recovery |

| Minimum penalty u/s 73 | Higher of ₹10,000 or 10% of tax dues |

Important: If you voluntarily pay the tax within 30 days of the Show Cause Notice you pay zero penalty. This is the most important window to act quickly.

Real Case Study – Adwani & Co

Textile Wholesaler Pune | GST Notice for ITC Mismatch (FY 2021-22)

A Pune-based textile wholesaler received a Section 73 SCN for ₹18.4 lakhs alleging ITC claimed on invoices not reflecting in GSTR-2B. The client had missed the response deadline and

an ex-parte order was already issued.

Demand Raised ₹18.4 Lakhs

Final Settled Amount ₹2.1 Lakhs

Demand Waived 89%

Our team filed a rectification application with full reconciliation proving 87% of the ITC was

valid with supplier invoices and payment proof. Penalty was fully waived.

Handled by Adwani & Co, 2023

Frequently Asked Questions

01.What is the GST notice reply format PDF / which form do I use?

You file your reply using Form GST DRC-06 on the GST portal. It allows you to submit a

written reply, upload supporting documents, and indicate whether you agree/disagree with the demand. There is no separate “PDF format” the reply is filed online through the portal. You

can prepare a detailed written representation offline and upload it as a PDF attachment with DRC-06.

02.How to reply to a GST notice — is it the same as an income tax notice?

No. Income tax notices are handled under the Income Tax Act 1961 via the Income Tax portal

(incometax.gov.in), while GST notices are handled under CGST Act 2017 via the GST portal (gst.gov.in). The forms, deadlines, and processes are completely different. This guide covers GST notices only.

03.What is the time limit to reply to a GST notice u/s 73?

The reply deadline is mentioned in the notice itself — typically 30 days from the date of the

notice. If you need more time, you can request an extension in writing via the portal. If you

received an intimation (DRC-01A) before the SCN, you have 30 days to pay or explain before the formal SCN is issued.

04.Can I avoid paying the penalty under Section 73?

Yes — if you pay the full tax demand within 30 days of receiving the Show Cause Notice

(SCN), no penalty is levied under Section 73(8). If you pay voluntarily even before the SCN is

issued (upon receiving DRC-01A), you pay zero penalty and no SCN is even issued.

Q5. What if I disagree with the entire demand?

You file a detailed reply via DRC-06 on the GST portal, contesting each point with evidence

invoices, ledgers, reconciliation statements, etc. The officer will schedule a personal hearing. If the order still goes against you, you can appeal before the GST Appellate Authority (GST APRIL-01) within 3 months of the order.

Q6. Is Section 73 notice serious? Will I face criminal action?

Section 73 notices are civil/tax proceedings — not criminal. Criminal prosecution under GST

applies only to Section 132 offences involving fraud, fake invoicing, or tax evasion above ₹5

crore. A Section 73 notice (no fraud element) will not result in criminal action if you respond

properly. However, ignoring it will lead to demand orders and recovery proceedings.

Q7. Can I hire a CA or tax consultant to handle the GST notice reply?

Absolutely and it is strongly recommended for demands above ₹1 lakh or complex ITC

mismatch cases. A qualified CA can review the notice, identify errors in the department’s claim,

prepare a legally sound reply, represent you in hearings, and negotiate settlements. Adwani & Co specialises in GST notice handling with a 90%+ success rate in demand reduction

About the Author

Dr. Haresh Adwani

Ph.D. in Commerce | Law Graduate | Managing Partner, Adwani & Co LLP Dr. Haresh Adwani holds a Ph.D. in Commerce and is a qualified Law graduate with over two decades of hands-on experience in GST advisory, direct taxation, and statutory compliance for businesses across Pune and Maharashtra. As Managing Partner of Adwani & Co LLP a firm established in 1977 by Advocate N. T. Adwani Dr. Adwani has guided hundreds of

SMEs, startups, and corporates through India’s evolving tax landscape. He is a recognised advisor on GST compliance, company formation, and Virtual CFO services, and regularly

contributes to professional seminars and industry forums in Pune.