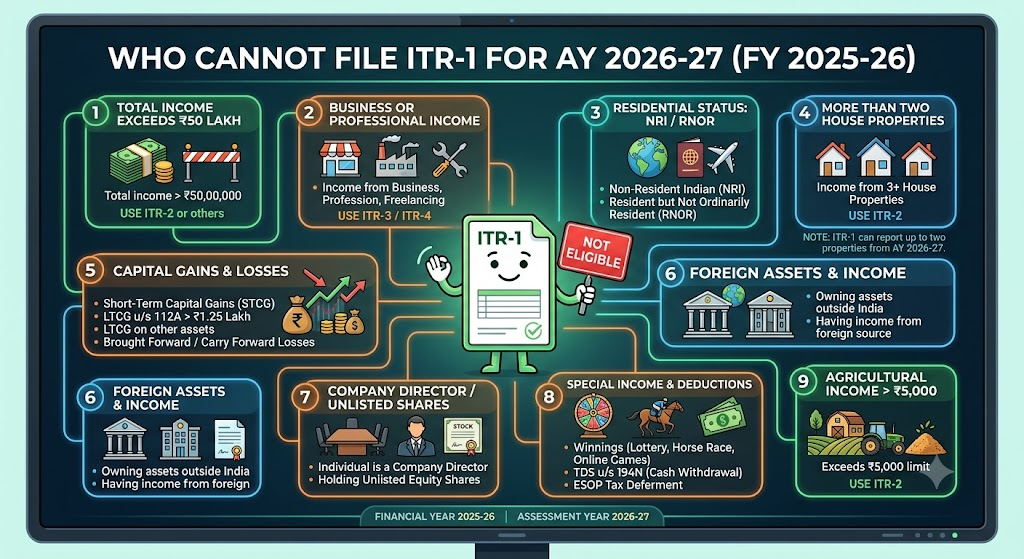

Who Cannot File ITR-1 for AY 2026-27

Every year, thousands of taxpayers in India make the same expensive mistake: they open the Income Tax e-filing portal, pick ITR-1 because it looks simple, and file only to receive a defective return notice months later. The reason? They were never eligible to use ITR-1 in the first place.

Understanding who cannot file ITR-1 for AY 2026-27 is not a technicality reserved for chartered accountants. It is essential knowledge for any individual taxpayer, because filing the wrong ITR form renders your return defective under Section 139(9) of the Income Tax Act and the department gives you just 15 days to fix it before treating your return as not filed at all.

This guide breaks down ITR-1 eligibility criteria for AY 2026-27 clearly, explains every disqualification, and tells you exactly which form you should be using instead.

What Is ITR-1 (Sahaj) and Who Is It Designed For?

ITR-1, officially called Sahaj, is designed for resident individuals with simple income profiles. The Income Tax Department introduced it specifically to make compliance easy for salaried employees, pensioners, and small interest earners who do not have complex financial transactions.

For AY 2026-27, ITR-1 is intended for individuals whose total income does not exceed ₹50 lakh from the following sources only:

- Salary or pension income

- Income from one house property (excluding cases where loss is carried forward from previous years)

- Income from other sources such as interest from savings bank accounts, fixed deposits, or family pension

- Agricultural income up to ₹5,000

If your income profile matches these criteria and only these you may be eligible to file ITR-1. But the list of people who cannot use this form is longer than most taxpayers realise.

Complete List : Who Cannot File ITR-1 for AY 2026-27

1. Taxpayers with Total Income Exceeding ₹50 Lakh

The income ceiling for ITR-1 is a hard limit. If your gross total income from all sources — including salary, interest, rental income, and any other head — exceeds ₹50 lakh in FY 2025-26, you are not eligible to file ITR-1 for AY 2026-27. You will need to file ITR-2 instead.

Practical Example: Ravi is a salaried employee earning ₹48 lakh per year. He also earned ₹4 lakh in interest income from FDs. His total income is ₹52 lakh. Despite being purely salaried, Ravi cannot file ITR-1 and must use ITR-2.

Read our detailed guide on GST Notice 2026: What Businesses Miss

2. Non-Resident Indians (NRIs) and RNORs

ITR-1 is exclusively for resident individuals. If your residential status for FY 2025-26 is Non-Resident Indian (NRI) or Resident but Not Ordinarily Resident (RNOR) as determined under Section 6 of the Income Tax Act, you cannot file ITR-1 under any circumstances.

NRIs must file ITR-2, which accommodates foreign income, foreign assets, DTAA (Double Taxation Avoidance Agreement) provisions, and NRE/NRO account disclosures. The Income Tax Department has strengthened NRI compliance tracking significantly — misclassification of residential status is one of the most common triggers for scrutiny notices.

3. Individuals with Capital Gains Income

If you earned any capital gains during FY 2025-26 whether from equity shares, mutual funds, property, gold, or any other capital asset you cannot file ITR-1. This applies to both Long-Term Capital Gains (LTCG) and Short-Term Capital Gains (STCG), including:

- LTCG from equity mutual funds exceeding ₹1.25 lakh (now taxable at 12.5% post-Budget 2024)

- STCG from shares taxed at 20% under Section 111A

- Capital gains from property sale

- Gains from debt mutual funds

Even a single mutual fund redemption or stock sale during the year makes ITR-1 inapplicable. The correct form is ITR-2.

Dr. Haresh Adwani, a PhD holder in Commerce and law graduate who leads Adwani and Company, frequently observes that taxpayers who invest in SIPs and redeem units during the year unknowingly disqualify themselves from ITR-1 — often without realising it until after filing.

4. Individuals with Income from More Than One House Property

ITR-1 allows reporting of income from only one house property. If you own two or more properties — whether self-occupied, rented, or deemed let out — you must file ITR-2.

Additionally, if you are carrying forward a loss from house property from a previous assessment year and wish to set it off in AY 2026-27, ITR-1 does not permit this. You will need ITR-2 to claim the set-off.

5. Directors of Companies

Any individual who serves as a director in a company (whether private, public, OPC, or any other structure registered with the MCA Ministry of Corporate Affairs) cannot file ITR-1. This restriction applies regardless of whether the director received any remuneration from the company during the year.

6. Individuals Who Hold Unlisted Equity Shares

If you hold shares in unlisted companies at any point during FY 2025-26, ITR-1 is not applicable for you. This includes ESOPs granted by private companies (which are typically unlisted) that have vested or been exercised during the year.

7. Individuals with Foreign Assets or Foreign Income

If you are a resident Indian who holds foreign assets — including overseas bank accounts, foreign property, foreign investments, or financial interests in any foreign entity — you must disclose them under Schedule FA in the ITR. ITR-1 does not have Schedule FA. Therefore, if you have any foreign assets or have earned income from outside India, ITR-2 is mandatory.

As Dr. Haresh Adwani points out in client advisory sessions at Adwani and Company, the CBDT has been particularly vigilant about foreign asset non-disclosure, and the penalties under the Black Money Act for wilful concealment are severe — making accurate form selection critical for this category.

H3: 8. Individuals with Business or Profession Income

If you have any income from business or profession freelancing, consulting, professional fees, sole proprietorship, or trading activity ITR-1 does not apply. This includes:

- Freelancers and independent consultants

- Professionals such as doctors, lawyers, architects, and designers earning professional fees

- Individuals running any business activity, even informally

- F&O traders (futures and options trading income is classified as business income)

For professionals with income under ₹75 lakh eligible for presumptive taxation, ITR-4 (Sugam) is the relevant form under Sections 44AD or 44ADA. For others, ITR-3 applies.

Learn more about our [ITR Filing Services for Freelancers and Professionals AY 2026-27]

9. Individuals with Agricultural Income Above ₹5,000

While agricultural income is exempt from income tax in India, it is used for rate purposes (to calculate tax on other income) when it exceeds ₹5,000. If your agricultural income exceeds this threshold, you cannot use ITR-1 and must file ITR-2.

10. Hindu Undivided Families (HUFs)

ITR-1 is available only to individuals. A Hindu Undivided Family is treated as a separate assessable entity under the Income Tax Act and must file ITR-2 (if no business income) or ITR-3 (if it has business income).

11. Individuals with Tax Deducted Under Section 194N

Section 194N applies TDS on cash withdrawals exceeding ₹1 crore (or ₹20 lakh for those who have not filed ITR for the past three years). If TDS has been deducted under this provision, you cannot use ITR-1.

Quick ITR Form Selection Reference : Who Cannot File ITR-1 and What to File Instead

| Situation | Cannot File ITR-1 | Correct Form |

| Income above ₹50 lakh | ✗ | ITR-2 |

| NRI or RNOR status | ✗ | ITR-2 |

| Any capital gains (LTCG/STCG) | ✗ | ITR-2 |

| More than one house property | ✗ | ITR-2 |

| Director of a company | ✗ | ITR-2 |

| Unlisted equity shares | ✗ | ITR-2 |

| Foreign assets or foreign income | ✗ | ITR-2 |

| Freelance or professional income | ✗ | ITR-4 or ITR-3 |

| F&O trading | ✗ | ITR-3 |

| HUF | ✗ | ITR-2 or ITR-3 |

| Agricultural income > ₹5,000 | ✗ | ITR-2 |

What Happens If You File ITR-1 When You Are Not Eligible?

Filing the wrong ITR form has real consequences:

The Income Tax Department processes returns under Section 143(1) and cross-checks the data against Form 26AS, AIS (Annual Information Statement), and SFT reports. If the filed form does not match your income profile, you will receive a defective return notice under Section 139(9).

You then have 15 days to file a revised return in the correct form. Failure to respond treats your return as not filed — exposing you to late filing fees under Section 234F (up to ₹5,000), interest under Sections 234A/B/C, and in some cases, scrutiny assessment.

According to advisories available on the Income Tax Department’s portal at incometax.gov.in, taxpayers are advised to carefully verify their eligibility before form selection each assessment year, as eligibility criteria and form instructions are updated annually. Dr. Haresh Adwani emphasises at Adwani and Company that the cost of correcting a wrong form selection in terms of time, penalties, and stress is almost always greater than the cost of getting it right the first time with professional assistance.

ITR-1 Eligibility Checklist for AY 2026-27

Before filing ITR-1, verify all of the following:

✅ You are a resident individual (not NRI or RNOR)

✅ Total income does not exceed ₹50 lakh

✅ Income is only from salary/pension, one house property, and other sources

✅ No capital gains of any kind during FY 2025-26

✅ You are not a director in any company

✅ You do not hold unlisted equity shares

✅ No foreign assets, foreign accounts, or foreign income

✅ No business or professional income

✅ Agricultural income is ₹5,000 or below

✅ No TDS under Section 194N

If even one box does not apply, you need a different form.

Read our detailed guide on ITR Filing 2026: Deadlines, Penalties & Smart Tax Saving Guide

Q1. Can I file ITR-1 if I sold mutual funds during FY 2025-26?

No. Any capital gains including redemption of mutual fund units disqualifies you from ITR-1 for AY 2026-27. You must file ITR-2.

Q2. I am salaried but also have a small freelance income. Which ITR form should I use?

You cannot use ITR-1. Since you have professional/freelance income, you need to file ITR-3 or ITR-4 (if eligible for presumptive taxation under Section 44ADA with income below ₹75 lakh).

Q3. Can a director of a private limited company file ITR-1?

No. Any individual serving as a director regardless of whether salary was received is disqualified from ITR-1 and must file ITR-2.

Q4. My salary is ₹48 lakh and FD interest is ₹3 lakh. Can I file ITR-1?

No. Your total income is ₹51 lakh, which exceeds the ₹50 lakh ceiling for ITR-1. You must file ITR-2.

Q5. Can NRIs use ITR-1 if their income is only from Indian salary?

No. ITR-1 is restricted to resident individuals. NRIs must file ITR-2 regardless of income source.

Q6. I have two flats one self-occupied and one rented out. Can I still use ITR-1?

No. ITR-1 permits only one house property. With two properties, you must file ITR-2.

Q7. What is the ITR filing last date for AY 2026-27?

The due date for filing ITR for most individual taxpayers for AY 2026-27 is July 31, 2026. Filing after this date attracts a late fee under Section 234F.

Conclusion: Get Your ITR Form Right Before You File

Choosing the right ITR form is the foundation of accurate tax filing for AY 2026-27. ITR-1 is simple and convenient but it is designed for a narrow income profile. If you have capital gains, directorship, foreign assets, more than one property, business income, or total income above ₹50 lakh, filing ITR-1 is not just incorrect it is a compliance risk.

The Income Tax Department’s systems are more sophisticated than ever before, with AIS cross-verification and AI-based scrutiny flagging form mismatches automatically. This is not the year to guess.

Adwani and Company, led by Dr. Haresh Adwani a PhD holder in Commerce and law graduate with deep expertise in income tax and compliance provides precise, personalised guidance on ITR form selection, deduction planning, and complete filing for individuals, professionals, and businesses across India.

About the Author

Dr. Haresh Adwani

Ph.D. in Commerce | Law Graduate | Managing Partner, Adwani & Co LLP Dr. Haresh Adwani holds a Ph.D. in Commerce and is a qualified Law graduate with over two decades of hands-on experience in GST advisory, direct taxation, and statutory compliance for businesses across Pune and Maharashtra has guided hundreds of SMEs, startups, and corporates through India’s evolving tax landscape. He is a recognised advisor on GST compliance, company formation, and Virtual CFO services, and regularly contributes to professional seminars and industry forums in Pune.

Don’t risk a defective return notice. Connect with Adwani and Company today for expert ITR filing guidance tailored to your income profile for AY 2026-27.

Disclaimer: This article is published for informational and educational purposes only. It does not constitute legal, financial, or professional tax advice. Tax laws are subject to change; readers are advised to consult a qualified Chartered Accountant or tax professional for advice specific to their circumstances. Content has been prepared with reference to provisions of the Income Tax Act, 1961 and publicly available CBDT guidelines.

© 2026 Adwani and Company. All rights reserved. Unauthorised reproduction or distribution of this content is prohibited.