GST Classification of Water

Same water. Same bottle. Completely different GST rate.

If that sentence surprises you, you are not alone. Across India, thousands of businesses in the food and beverage sector from distributors and traders to hotels and e-commerce sellers are applying incorrect GST classifications to water and water-based beverages. The result? Short payment of tax, mismatched GSTR-3B filings, wrong input tax credit eligibility, and in some cases, a GST notice landing at their door before they even realise the error.

The GST classification of water is one of the most instructive examples of how GST rates in India work and why getting HSN codes right is not a formality but a core compliance obligation. The product may look identical on the shelf, but factors such as packaging, processing, added ingredients, and the manner of supply change the tax rate from Nil to 5% to 28% plus cess, depending entirely on how the product is classified under GST.

At Adwani and Company, we regularly encounter businesses that have been applying a blanket GST rate to their water products without realising that the GST rate depends on the product’s HSN classification, not just its description. Dr. Haresh Adwani who holds a PhD in Commerce and a law degree, and brings both regulatory depth and legal precision to complex GST matters has helped numerous clients correct their classifications before a GST scrutiny notice forced them to.

This guide walks you through every category of water and water-based beverages under GST, the applicable HSN codes, the rates under GST rates India 2026, and the compliance risks that come with wrong classification.

Why GST Classification of Water Is More Complex Than It Looks

GST in India does not tax products it taxes classified goods and services as defined by the GST Council. Each product is assigned a Harmonised System of Nomenclature (HSN) code, and the tax rate follows the HSN code, not the product name.

Water, in its many commercial forms, falls across multiple HSN chapters. This is what makes GST classification of water particularly prone to errors:

- Chapter 22 of the GST tariff covers waters, including mineral, aerated, and other non-alcoholic beverages

- Chapter 2201 covers water without added sugar or flavouring including plain, mineral, and aerated water

- Chapter 2202 covers waters with added sugar, sweeteners, or flavourings including soft drinks, carbonated beverages, and energy drinks

The critical distinction is not the physical state of water, but what has been added to it, how it has been processed, and how it is packaged and supplied. This is where most classification errors occur.

| Key Insight on GST Compliance The GST Council’s rate schedule is based on HSN codes not product names. A business that classifies ‘water’ without checking the correct HSN code and corresponding rate schedule is always at risk of a short payment or excess ITC claim. Source: GST Portal : gst.gov.in |

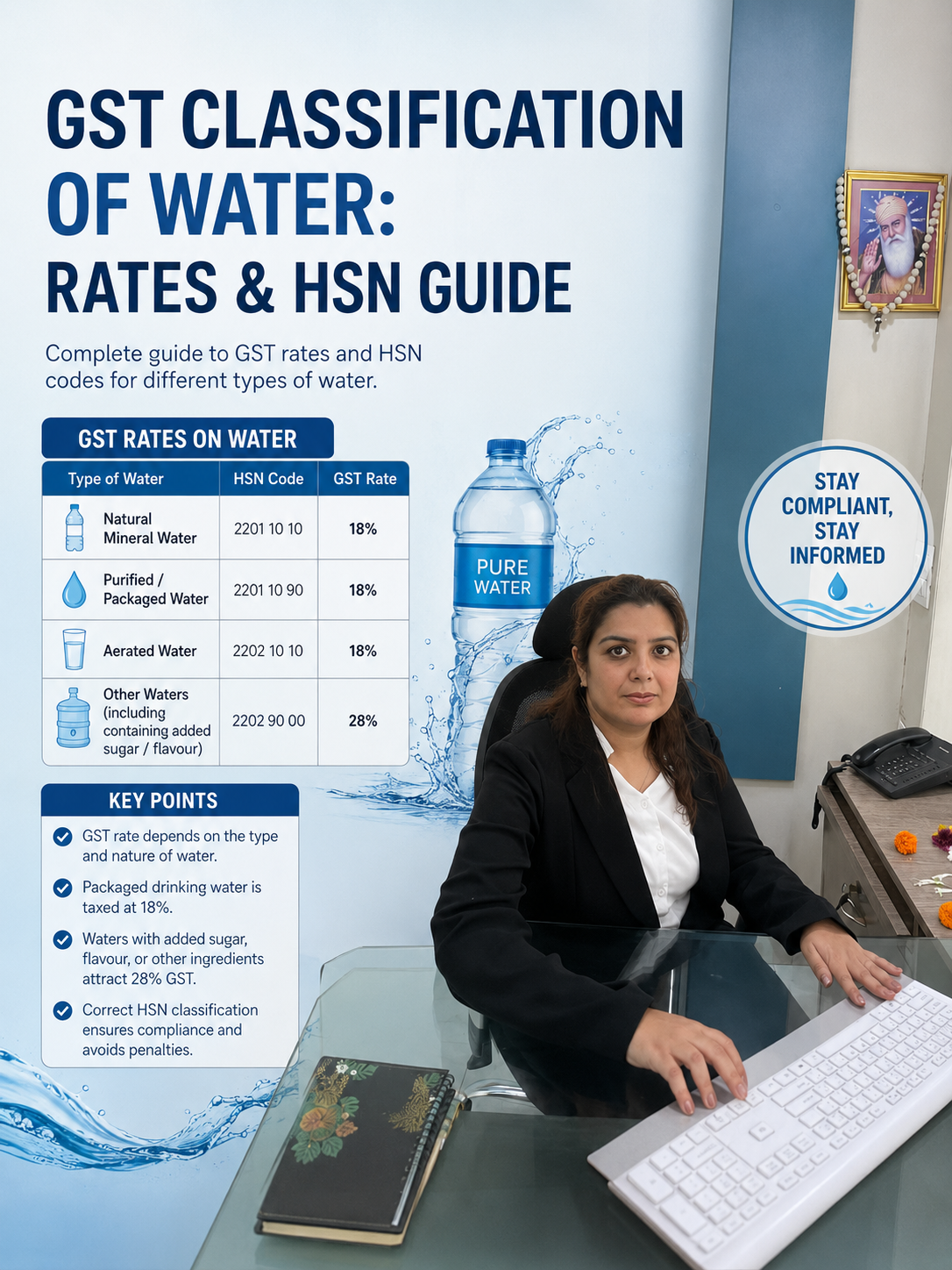

GST Classification of Water: Complete Rate Table with HSN Codes

The following table reflects the GST rates applicable to different categories of water products under GST rates India 2026. Businesses should verify current rates on the GST Portal as the GST Council periodically revises these classifications.

| Water Product / Category | HSN Code | GST Rate | Key Condition |

| Tap water (municipal supply) | 2201 | NIL | Supplied through distribution system |

| Water supplied through pipelines | 2201 | NIL | Non-commercial pipeline supply |

| Packaged drinking water (≤20 litres) | 2201 | 12% | Pre-packaged, sealed containers |

| Packaged drinking water (>20 litres) | 2201 | 5% | Large bulk packaged jars |

| Natural mineral water | 2201 | 12% | Bottled, commercially sold |

| Ice (for commercial use) | 2201 | 18% | Manufactured ice sold commercially |

| Aerated/carbonated plain water | 2201 | 18% | Carbonated, no added sweetener |

| Flavoured or sweetened water | 2202 | 28% + Cess | Added sugar, flavour, or sweetener |

| Carbonated soft drinks / cola | 2202 | 28% + Cess | Sugared, flavoured carbonated drinks |

| Soda water (plain, no flavour) | 2201 | 18% | Aerated water without additives |

Important Update for 2026

GST rates on packaged drinking water were revised by the GST Council. Packaged water sold in bottles up to 20 litres now attracts 12% GST (revised upward from 5% in an earlier Council meeting). Bulk jars above 20 litres continue at 5%. Always verify the current rate schedule before GSTR-3B filing 2026. Source: GST Council notifications gst.gov.in

Read our detailed guide on GST Notice 2026: What Businesses Misshttps://www.adwaniandco.com/blog/gst-notice-2026-what-businesses-miss

GST Classification Error: A Real-World Example and Its Cost

Consider a beverage distributor, Mehta Beverages Pvt Ltd, supplying three categories of products: natural mineral water in 1-litre bottles, 500 ml flavoured fruit water, and bulk 20-litre packaged drinking water jars.

| Product | Correct GST Rate | Rate Applied | Monthly Turnover | Monthly GST Short-paid |

| Mineral water (1L bottles) | 12% | 5% (error) | ₹8,00,000 | ₹56,000 |

| Flavoured fruit water (500ml) | 28%+cess | 12% (error) | ₹4,50,000 | ₹72,000+ |

| Bulk jars (20L) | 5% | 12% (error) | ₹3,00,000 | ₹21,000 excess |

| TOTAL MONTHLY IMPACT | — | — | ₹15,50,000 | ₹1,07,000+ net error |

In this scenario, Mehta Beverages is simultaneously underpaying GST on mineral water and flavoured water, and overpaying on bulk jars. The net monthly tax error exceeds ₹1 lakh. Over a financial year, this compounds to over ₹12 lakh in potential tax liability, interest under Section 50 of the CGST Act, and possible penalties all originating from a classification assumption rather than a deliberate evasion.

Dr. Haresh Adwani, drawing on both his commerce expertise and legal training, emphasises that classification errors of this nature are treated by GST authorities as compliance failures and depending on whether the assessing officer concludes they are due to negligence or fraud, the penal consequences can vary significantly under Sections 122 to 125 of the CGST Act.

→ Learn more about our GST Advisory and Compliance Services

Why Businesses Apply Wrong GST Classification for Water Products

In our experience at Adwani and Company, wrong GST classification of water and beverage products typically arises from three sources:

1. Relying on Product Descriptions Instead of HSN Codes

Businesses often instruct their billing teams to apply a GST rate based on what the product is called — ‘water’, ‘flavoured water’, ‘mineral water’ — without mapping it to the HSN code. Since water falls across HSN 2201 and 2202 with very different rates, this approach consistently produces errors.

2. Outdated Rate Masters

GST rates have been revised by the GST Council on multiple occasions since 2017. Businesses that set up their accounting software once and never updated the rate master are likely operating with incorrect classifications, particularly after the 2022 and 2024 rate revisions on packaged goods.

3. Treating Carbonated and Non-Carbonated Products the Same

One of the most common mistakes is applying the same GST rate to plain soda water and flavoured carbonated drinks. While both are ‘fizzy’, plain soda water without any added sugar or flavouring falls under HSN 2201 (18%), while a sweetened carbonated beverage falls under HSN 2202 at 28% plus compensation cess. The composition of the product not its fizzy character determines the classification.

GST Classification Errors: Compliance Consequences You Cannot Ignore

Wrong GST classification is not a technicality that authorities overlook. The GST Portal, now integrated with e-invoice data, e-way bill records, and GSTR-2B reconciliation, makes it increasingly straightforward for the department to identify businesses applying inconsistent rates.

The consequences of wrong GST classification of water and other products include:

- Short payment of GST: liability to pay the differential tax amount

- Interest at 18% per annum under Section 50 of the CGST Act from the due date of payment

- GST return late fee penalty if the classification error was detected only after a delayed return

- ITC reversal if input tax credit was claimed on purchases at a rate inconsistent with the correct classification

- Issuance of a show cause notice under Section 73 or Section 74 of the CGST Act

- Potential scrutiny of GSTR-3B filing 2026 records going back up to five years in cases of fraud

According to advisories available through the GST Portal, the department’s automated compliance mechanism cross-verifies HSN-wise turnover reported in GSTR-1 against GSTR-3B filed tax amounts. Discrepancies at the HSN level trigger further review making accurate GST classification of water and all other products a non-negotiable compliance requirement.

GST Classification Extended: Beverages Beyond Water

The water classification exercise extends directly to other beverages that businesses commonly sell or distribute. Understanding where each product sits in the GST rate schedule helps prevent misclassification across an entire product portfolio.

| Beverage Product | HSN | GST Rate | Notes |

| Coconut water (natural) | 2009 | NIL | Unprocessed, no packaging |

| Coconut water (packaged) | 2202 | 12% | Packaged, commercially sold |

| Fruit juice (100%, packaged) | 2009 | 12% | No added sugar |

| Fruit drinks (<100% juice) | 2202 | 28% | With added sweeteners |

| Energy drinks | 2202 | 28% + Cess | Caffeinated, sweetened |

| Syrups / sharbat concentrate | 2106 | 18% | Concentrated form for dilution |

| Tea / coffee (non-alcoholic) | 0902 / 0901 | 5% | Unprocessed or basic processing |

This expanded view matters enormously for businesses in the FMCG distribution, hotel industry, and e-commerce categories, where multi-product invoicing requires accurate HSN codes and corresponding GST rates on every line item. A single wrong rate on a high-volume SKU can create a substantial GST compliance gap that surfaces months later during a GSTR-2B reconciliation review or a GST registration 2026 renewal verification.

GST Classification for Businesses: Why Professional Advisory Matters

The GST framework is not static. The GST Council meets periodically sometimes several times a year and revises rates, exemptions, and classification guidance. Businesses that rely solely on their accounting software or historical practice risk operating on outdated assumptions.

At Adwani and Company, we conduct periodic GST classification reviews for clients in the FMCG, hospitality, manufacturing, and e-commerce sectors. The review maps each product in the client’s portfolio against the current HSN rate schedule, identifies classification mismatches, quantifies the tax exposure, and recommends corrective action either through a voluntary rectification in a subsequent return or, where warranted, through a formal amended return under the CGST Act.

Dr. Haresh Adwani notes that classification disputes are among the most contested areas of GST litigation. The combination of his doctoral background in commerce which includes detailed study of indirect taxation frameworks and his legal training allows him to assess classification questions not only from a tax rate perspective, but also from the angle of how an Appellate Authority or the GST Tribunal would evaluate the same question.

For businesses with complex product lines, we recommend an annual GST health check that includes HSN classification validation, GSTR-2B reconciliation, input tax credit eligibility 2026 review, and alignment of GSTR-1 outward supplies with GSTR-3B tax liability filings.

Key Takeaways: GST Classification of Water at a Glance

| Water / Beverage Type | GST Rate | Critical Risk if Misclassified |

| Tap water / pipeline supply | NIL | Incorrectly charging GST = excess collection liability |

| Packaged drinking water (≤20L) | 12% | Charging 5% = short payment + interest |

| Packaged drinking water (>20L) | 5% | Charging 12% = excess deposit + ITC mismatch |

| Mineral water (bottled) | 12% | Charging 5% = short payment; 28% = overcharge |

| Flavoured / sweetened water | 28% + Cess | Charging 12–18% = significant short payment |

| Carbonated soft drinks | 28% + Cess | Among highest-risk misclassification items |

| Plain soda / aerated water | 18% | Must confirm no added sugar/flavour |

1. What is the GST rate on packaged drinking water in India 2026?

Packaged drinking water sold in bottles or pouches up to 20 litres attracts 12% GST under HSN 2201 as of 2026. Bulk packaged water in jars above 20 litres continues to be taxed at 5%. These rates were revised by the GST Council and differ from earlier years. Always check the current GST Portal rate schedule before GSTR-3B filing 2026.

2. What is the HSN code for mineral water and what is its GST rate?

Natural mineral water falls under HSN 2201. The applicable GST rate is 12% for commercially bottled and packaged mineral water. Tap water and water supplied through municipal pipelines remains at NIL. The distinction lies in the commercial packaging and processing two factors that directly determine GST classification under Indian GST law.

3. Why is flavoured water taxed at 28% GST while plain water is taxed at 5–12%?

The GST classification of water changes fundamentally when sugar, flavouring agents, or sweeteners are added. Plain water even when packaged falls under Chapter 2201 of the GST tariff. Water with any added flavour, sugar, or sweetener moves to Chapter 2202, which attracts 28% GST plus compensation cess. This classification is based on the Harmonised System of Nomenclature codes adopted under India’s GST regime.

4. What happens if a business applies the wrong GST rate on water products?

Wrong GST classification triggers short payment of tax, interest at 18% per annum under Section 50 of the CGST Act, and possible penalties under Sections 122 to 125. Additionally, input tax credit claimed by buyers on incorrectly classified invoices may be disallowed during a GSTR-2B reconciliation review. Where the department determines that the misclassification was not bona fide, the GST return late fee penalty provisions may also apply. Businesses should consult a CA firm like Adwani and Company to verify their classification and correct any errors proactively.

5. Is ice taxed under GST? What is the GST rate on ice in India?

Ice manufactured and sold commercially falls under HSN 2201 and attracts 18% GST. This is distinct from ice cream, which falls under a different chapter. Ice used in food processing can also have different implications depending on how it is supplied and whether it forms part of a composite supply. Businesses in the hospitality and cold chain sectors should map their ice-related purchases and sales carefully.

Conclusion: In GST, the Right Question Is Always ‘How Is It Classified?’

Water, in its many commercial forms, is a perfect illustration of why GST compliance is fundamentally about classification accuracy and not just tax payment. The same substance water attracts NIL GST when flowing through a tap, 5% when packaged in a bulk jar, 12% when bottled as mineral water, and 28% plus cess when sweetened or flavoured.

Wrong GST classification of water products is not a rare edge case. It is one of the most common compliance errors in the food and beverage trade in India today. And with the GST Portal’s data analytics now cross-referencing GSTR-1, GSTR-3B, e-invoices, and e-way bills in near real time, the window for undetected classification errors is narrowing every month.

As Dr. Haresh Adwani consistently advises clients: before asking ‘What is the GST rate?’, always ask ‘How is my product classified under GST?’ Because in Indian taxation, the classification determines everything the rate, the input tax credit eligibility, and ultimately, whether your GSTR-3B filings hold up to scrutiny.

A small classification check today can prevent a major tax dispute tomorrow. And the right time to conduct that check is now not after a notice arrives.

About the Author – Nidhi Adwani

Nidhi Adwani is the Human Resources Manager at Adwani & Co. She is a Law Graduate and holds an MBA in Human Resources. She manages recruitment, employee engagement, team development, workplace culture, and the firm’s social media and content activities. Passionate about people and organizational growth, she also contributes articles for ITRAdvisor and Adwani & Co. Her writing focuses on HR practices, leadership, workplace engagement, and professional development, offering practical insights for professionals and businesses.