Notice Under Section 153C: What to Do if Your Name is in Someone Else’s Papers. Protect your rights and challenge wrongful tax demands with Adwani & Co.

When tax authorities find your name in a third party’s documents during a search, the law draws a sharp line between what is permissible and what is not. Most taxpayers and even some officers get this wrong.

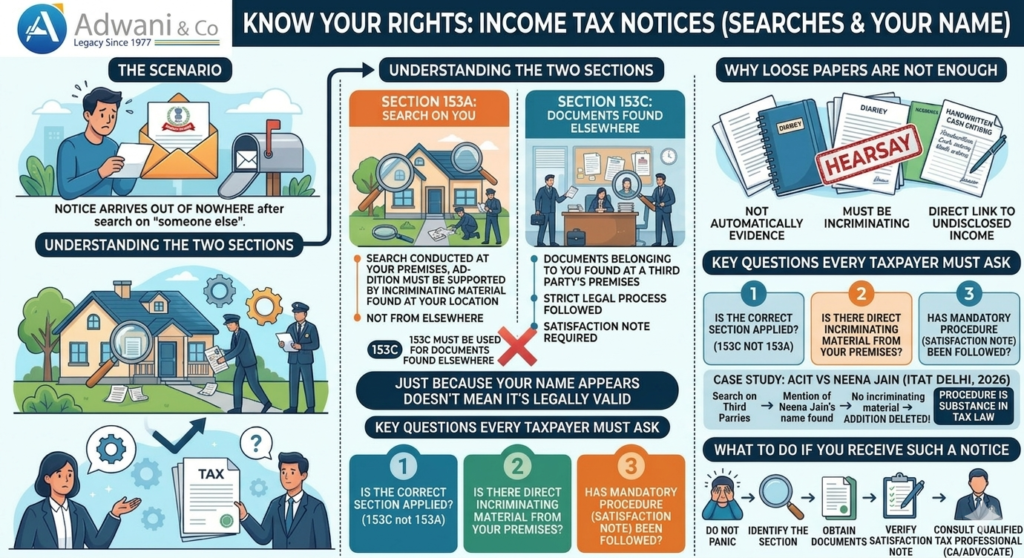

The Notice That Arrives Out of Nowhere

Imagine opening your mailbox one ordinary morning to find an income tax notice. The search was not on you. No officer visited your home. No documents were seized from your premises. Yet there it is a notice proposing a significant addition to your income, based on papers found at someone else’s address.

This is not a rare scenario. It happens frequently across India, and it leaves taxpayers confused, anxious, and often vulnerable to wrongful demands. The good news? The law is clear if you know where to look.

Key insight: Just because your name appears in a document does not mean an income tax addition against you is legally valid. The section under which proceedings are initiated matters enormously.

Also Read

https://www.adwaniandco.com/blog/income-tax-reopening-notice-invalid-india

Understanding Section 153C vs 153A

The Income Tax Act, 1961 lays down two distinct legal pathways when a search or seizure operation takes place. Confusing one for the other is not merely a paperwork error it can invalidate the entire proceeding.

Section 153A

Search on YOU

Applies when income tax authorities conduct a search directly on your premises. Any addition made must be supported by incriminating material found at your location. Not from elsewhere from your address.

Section 153C

Documents found elsewhere

Applies when documents or assets belonging to you, or referring to you, are found during a search at a third party’s premises. A strict legal process, including a satisfaction note, must be followed before you can be assessed.

The distinction is not technical hair-splitting. It is the foundation of a fair assessment. When the wrong section is applied, the entire addition is built on a procedurally defective foundation and courts have consistently held that such additions cannot stand.

Don’t panic over a Section 153C notice. Follow these 5 critical steps to protect your rights and challenge wrongful tax additions with expert advice.

5 Critical Steps to Take Immediately

- Identify the Section: Verify if the notice is under Section 153A or 153C. If no search occurred at your premises, 153A is likely invalid.

- Verify the Satisfaction Note: Ensure the Assessing Officer recorded a formal “satisfaction note” before proceeding.

- Inspect the Evidence: Demand to see the “incriminating material.” Remember, casual mentions in loose papers are often not enough.

- Check for Procedural Errors: In tax law, procedure is substance. A wrong section means the entire addition could be deleted.

- Consult a Professional: Engage a qualified tax advocate or CA at Adwani & Co to draft a technically sound response.

What Went Wrong in ACIT vs Neena Jain (ITAT Delhi, 2026)

This recently decided case before the Income Tax Appellate Tribunal, Delhi, is a textbook example of procedural overreach and how the law protects taxpayers when authorities step outside their legal bounds.

Case Study

ACIT vs Neena Jain ITAT Delhi, 2026

A search and seizure operation was conducted but on third parties, not on the assessee.

During that search, loose papers and handwritten cash entries were discovered that allegedly mentioned Neena Jain’s name.

The department initiated proceedings against her under Section 153A the section that applies only when a search is conducted on the taxpayer herself.

No incriminating material was found from the assessee’s own premises. The entire case rested on third party documents.

The mandatory procedure under Section 153C including a formal satisfaction note from the Assessing Officer was not followed.

The ITAT held that the addition was entirely unsustainable. The wrong section had been invoked, there was no incriminating material against the assessee, and the entire addition was deleted.

Why Loose Papers Are Not Enough

Tax law does not operate on suspicion or inference alone. Loose papers found at a third party’s premises a diary, a note, a printed ledger entry are not automatically evidence against the person named in them. The courts have repeatedly emphasised that the word “incriminating” is key.

Incriminating material means evidence that directly implicates the assessee not hearsay, not casual mentions, not unverified entries in someone else’s records. For an addition to survive legal scrutiny, there must be a direct and demonstrable link between the document and the assessee’s undisclosed income.

What counts as incriminating material? Documents, assets, or entries that directly and specifically indicate the taxpayer’s undisclosed income or unexplained investment and which were found during a valid search of their own premises.

The Three Questions Every Taxpayer Must Ask

Before filing a reply to any income tax notice arising from a search whether on you or on someone else take a step back and ask these three questions systematically. The answers could determine whether any addition against you survives at all.

Is the correct section being applied?

If the search was not on your premises, the department must proceed under Section 153C, not 153A. Any notice issued under the wrong section is procedurally invalid from the outset.

Is there direct incriminating material against you?

The tax department must point to specific documents or assets found from your premises that establish undisclosed income. A mere mention of your name elsewhere is not sufficient.

Has the mandatory procedure been followed?

Under Section 153C, the Assessing Officer of the searched person must record a satisfaction note establishing that the documents belong to or pertain to you. Without this, the proceeding has no legal basis.

The Broader Lesson Procedure Is Substance in Tax Law

In many areas of life, procedure is secondary to outcome. In Indian income tax law, it is the opposite. A procedural error by the department invoking the wrong section, failing to record a satisfaction note, relying on documents not found from the correct premises is not a minor lapse that can be cured later. It is a fundamental defect that vitiates the entire assessment.

This is why experienced tax practitioners scrutinise the procedural foundation of every assessment order, not just the quantum of the addition. An addition of any amount, no matter how large, can be deleted if the legal basis for initiating proceedings was flawed.

The Neena Jain case reinforces a principle that courts have upheld consistently: an assessee cannot be penalised simply because their name surfaced in someone else’s records. The law demands more and it is right to do so.

Remember: Tax cases are not decided solely on what documents exist. They are decided on how those documents were obtained, whose premises they came from, and whether the correct legal process was followed at every step.

Notice Under Section 153C:What to Do If You Receive Such a Notice

Receiving a notice is not a verdict. It is the beginning of a legal process one in which you have rights, safeguards, and remedies. Here is a practical approach:

First, do not respond in panic. Read the notice carefully, identify the section under which it is issued, and note the assessment year and the search date. Second, obtain the documents on which the department is relying. You have a right to inspect the material used against you. Third, verify whether a satisfaction note exists under Section 153C. If it does not, that is a strong procedural ground in your favour.

Most importantly, consult a qualified tax advocate or chartered accountant with experience in search assessments. The nuances of Sections 153A and 153C are well-litigated but fact-specific. Professional guidance tailored to your situation is essential.

Disclaimer: This article is intended for general informational and educational purposes only. It does not constitute legal or tax advice. The facts and outcome of the ACIT vs Neena Jain case are discussed for illustrative purposes. For advice specific to your situation, please consult a qualified tax professional or legal counsel.

Frequently asked questions

1.I received a tax notice after a search on someone else.What shouls I do first?

Do not panic and do not respond immediately without analysing the notice carefully. Here are the first three steps you should take:

1. Identify the section: Check whether the notice is issued under Section 153A or Section 153C. If the search was not on your premises, Section 153A cannot validly apply.

2. Verify the satisfaction note: Ask your tax advisor to confirm whether the Assessing Officer recorded a valid satisfaction note as required under Section 153C.

3. Check the evidence: Find out exactly which documents the department is relying on and whether they constitute genuine incriminating material found from your premises.

2.How many years can the income tax department reopen under Section 153A

Under Section 153A, the income tax department can reopen assessments for six assessment years immediately preceding the year of search. In cases where the undisclosed income exceeds Rs. 50 lakhs, the department can go back up to ten assessment years.

However, this power applies only when a valid search has been conducted on the assessee’s own premises, and only when incriminating material is found for the relevant years. For years where no incriminating material is found, additions to completed assessments are not permissible — as confirmed by the Supreme Court.