By Dr. Haresh Adwani, PhD (Commerce), Law Graduate & Senior Partner — Adwani and Company

Published · May 2026

“A search and seizure operation does not destroy a business. The panic that follows does.”

Picture this: It is 6 a.m. on an ordinary Tuesday. Before your first cup of chai, there is a knock at the door a team of Income Tax officers with official authorisation to conduct a search and seizure under Section 132 of the Income Tax Act, 1961. Your heart races. Your mind goes blank. And in the silence of that moment, a single question forms: What do I do now?

If you run a business in India whether a proprietorship, a partnership, a private limited company, or an LLP — an income tax search and seizure is one of the most stressful regulatory events you will ever face. Yet the businesses that come through it with the least damage are not the luckiest. They are the most prepared.

In this comprehensive guide, Dr. Haresh Adwani of Adwani and Company breaks down exactly what happens during an IT raid, what your rights are, what mistakes destroy businesses, and most critically what you must do in the 48 hours after a search and seizure operation.

What Is an Income Tax Search and Seizure?

Under Section 132 of the Income Tax Act, 1961, the Director General of Income Tax or the Commissioner of Income Tax is empowered to authorise a search and seizure when there is credible information suggesting that a person is in possession of undisclosed income, unexplained assets, or unaccounted cash and documents. According to the official guidelines issued by the Income Tax Department of India, search operations are conducted covertly and without prior notice. They can cover business premises, residential properties, bank lockers, and even vehicles, computers, and digital storage devices.

This is not a routine inspection or assessment. An income tax search and seizure carries serious evidentiary and legal consequences, and how you respond in the first hours — and in the 48 hours that follow — can significantly determine the outcome of any subsequent proceedings.

Section 132 vs Section 133A: Knowing the Difference

Many business owners confuse a search and seizure under Section 132 with a survey under Section 133A. The distinction is critical. A survey is conducted during business hours and is limited to business premises. Officers cannot seize books or documents in a survey — they can only make copies.

A Section 132 search, on the other hand, can take place at any hour, covers all premises simultaneously, and gives officers the power to seize books, documents, cash, jewellery, and digital assets. Understanding this difference is the first step to responding correctly.

→ Learn more about our Tax Compliance Serviceshttps://www.adwaniandco.com/services/taxation-compliance

What Happens During an Income Tax Search and Seizure?

Across businesses sectors, the sequence of events in an IT search and seizure typically unfolds as follows:

- Officers arrive, typically at dawn, with a valid search warrant issued under Section 132.

- They produce their identity cards and the authorisation order. You have a right to examine both.

- All persons present at the premises may be required to stay until the search concludes.

- Officers inspect books of accounts, ledgers, computers, mobile phones, documents, and safes.

- Cash, jewellery, and documents found during the search may be seized or placed under restraint.

- A Panchnama (an official record) is prepared, listing everything searched and seized.

- You (or your authorised representative) must sign this Panchnama.

- A statement may be recorded under oath (Section 132(4)).

The search can continue for multiple days. Officers are permitted to seal premises or break open any locked space if they have reason to believe it coYour Legal Rights During an Income Tax Search and Seizurenceals undisclosed assets.

Your Legal Rights During an Income Tax Search and Seizure

Cooperation does not mean surrender. Every business owner has legal rights during an income tax search and seizure, and understanding them is not obstructing justice it is exercising the protections that Indian law guarantees.

- You have the right to verify the identity of officers and examine the search warrant.

- You may have two respectable witnesses present during the search (Panchas).

- You are entitled to a copy of the Panchnama at the end of the search.

- You can refuse to make voluntary statements without the presence of your legal or tax advisor.

- You have the right to be informed of the grounds of search on request.

- Any item seized must be listed, and you are entitled to an acknowledgement receipt.

- You can request that the search be conducted in the presence of a medical officer if someone present requires medical attention.

Dr. Haresh Adwani consistently advises his clients: “Know your rights before you need them. The moment of a search is not the time to be reading the rulebook.”

https://www.adwaniandco.com/services/taxation-compliance→ Learn more about our Business Legal Advisory Serviceshttps://www.adwaniandco.com/services/taxation-compliance

The Biggest Mistakes Businesses Make During a Search and Seizure

In over two decades of tax advisory work, Adwani and Company has seen businesses suffer far greater damage from their own reactions than from the search itself. These are the most costly mistakes:

1. Panic-driven statements

The moment officers arrive, the instinct is to explain, justify, or apologise. Any statement made under pressure — even an innocent explanation — can be treated as an admission in subsequent proceedings. Never make voluntary statements without your tax advisor present.

2. Handing over documents without a record

Every document removed from your premises must be listed in the Panchnama. Handing over files without insisting on this record can create disputes later about what was taken and in what condition.

3. Failing to contact a professional immediately

The single most effective action you can take during the search is to call your Chartered Accountant and legal advisor immediately. Your advisor can guide you on what to say, what not to say, and how to ensure the process is conducted lawfully.

4. Making undocumented admissions in Section 132(4) statements

Officers may record your statement under oath during the search. Anything you say here has legal weight. Statements that are later contradicted by your accounts or books can be used against you. Always insist on reviewing what has been recorded before signing.

Practical Example

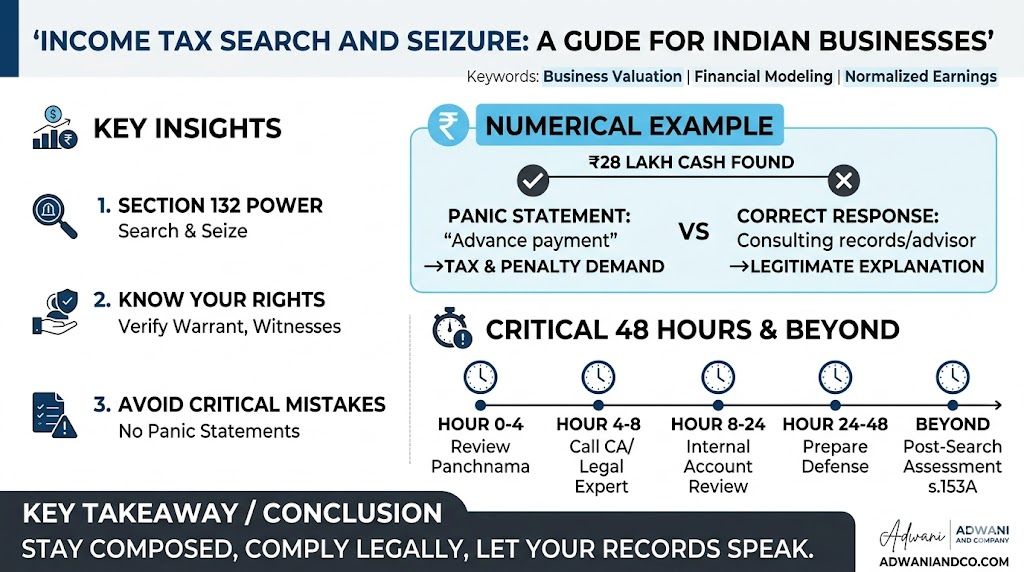

Scenario: A manufacturing firm in Pune undergoes an income tax search and seizure. Officers find ₹28 lakh in cash on the premises. The proprietor, panicking, immediately explains the cash as “advance payment from a customer.” This oral statement is recorded in the Section 132(4) statement.

However, the firm’s actual books show the ₹28 lakh as an opening balance a completely legitimate entry. Because the oral statement did not match the books, the department treated the discrepancy as an unexplained liability, leading to tax demand, interest, and penalties exceeding ₹11 lakh.

Lesson: Had the proprietor simply said “I will provide a written explanation after consulting my advisor,” the cash would have been explained through the books alone — with no inconsistency and no additional liability.

The Critical 48 Hours After an Income Tax Search and Seizure

The search ends. The officers leave. And now you face the 48 hours that will define what comes next. This is not the time to be passive. Based on the advisory approach of Adwani and Company, here is what must happen immediately:

- Hour 0–4: Review and retain a copy of the Panchnama. Document everything that was seized, including descriptions, quantities, and condition.

- Hour 4–8: Brief your Chartered Accountant fully — share all correspondence, the Panchnama, and any statements recorded.

- Hour 8–16: Conduct an internal review of your accounts. Identify every item mentioned or seized and ensure you can explain it with supporting documentation.

- Hour 16–24: Prepare a chronological record of events from the moment of search — witnesses present, officers’ names, time, and sequence of actions.

- Hour 24–48: File any retraction or clarification to a Section 132(4) statement (if made under duress) through your legal advisor, if required.

- Hour 48: Engage legal counsel for the post-search assessment proceedings under Section 153A (which replaces the regular assessment for the six preceding years

The Ministry of Finance has consistently clarified that post-search assessments under Section 153A require the Assessing Officer to issue notices for the six assessment years immediately preceding the search. Being prepared with clean, explainable accounts for those six years is your strongest defence.

→ Read our detailed guide on Poshttps://www.adwaniandco.com/blog/section-153c-tax-notice-guidet-Search Assessment under Section 153A

How Adwani and Company Protects Your Business During a Search and Seizure

Adwani and Company provides end-to-end advisory support for businesses facing income tax search and seizure proceedings. From the moment the search begins to the final resolution of post-search assessments, the firm offers:

- Immediate on-call advisory during and after the search

- Review and verification of the Panchnama and seized documents

- Preparation and filing of statements under Section 132(4)

- Representation before the Income Tax Department during post-search assessments

- Assistance with appeals before the Commissioner (Appeals) and the Income Tax Appellate Tribunal (ITAT)

- Guidance on penalty mitigation and settlement proceedings

As Dr. Haresh Adwani puts it: “The goal is not just to survive a search. The goal is to come out on the other side with your business, your reputation, and your future intact.”

Preventive Measures: How to Search-Proof Your Business

While no business can predict a search and seizure, every business can reduce the risk and the damage. Adwani and Company recommends the following proactive steps:

- Maintain meticulous books of accounts reconciled monthly, audited annually as required under the Income Tax Act.

- Ensure all cash transactions above ₹2 lakh are properly documented (as mandated under Section 269ST).

- File GST returns accurately and on time through the GST Portal.

- Keep all MCA filings current particularly for companies and LLPs regulated by the Ministry of Corporate Affairs.

- Maintain a “search readiness” file: updated balance sheet, cash book, investment records, and explanation for any large or unusual transactions.

- Conduct an internal “mock audit” annually with your CA to identify and resolve discrepancies before they become issues.

→ Learn more about our Annual Compliance and Services https://www.adwaniandco.com/services/taxation-compliance

Conclusion: A Search Is Not the End : How You Respond Decides What Comes Next

An income tax search and seizure is undeniably one of the most disruptive events in a business owner’s life. But it is not, by itself, a verdict. The Income Tax Department initiates thousands of search operations every year and many of them conclude without any adverse outcome for the searched party, because those businesses maintained clean records, exercised their rights, and responded with the guidance of qualified professionals.

What makes the difference is not luck. It is preparation. It is calm. It is the right advisor at the right moment.

The businesses that come through a search and seizure intact are the ones that call their Chartered Accountant first, stay composed second, and let the documentation speak for itself third.

If your business has faced an income tax search and seizure — or if you want to be prepared for one — the expert team at Adwani and Company, led by Dr. Haresh Adwani, is ready to guide you through every step with precision, confidentiality, and decades of hard-won expertise.

Frequently Asked Questions

1. Can the Income Tax Department conduct a search and seizure without a warrant?

No. A search under Section 132 requires written authorisation from a high-ranking officer typically the Director General or Commissioner of Income Tax. You have the right to examine this authorisation before permitting entry.

2. How long can an income tax search and seizure last?

There is no statutory time limit. In practice, searches involving complex cases and multiple premises can last several days. However, the search must be conducted within the scope of the authorisation order.

3. Can I refuse to answer questions during a search and seizure?

You are required to cooperate, but you are not required to make voluntary statements without your advisor. You may request that any statement under Section 132(4) be deferred until your tax advisor is present though officers may not always agree to this. Be careful and measured with every word.

4. What happens to the cash and jewellery seized during an IT raid?

Seized assets are held by the department and can be retained for up to 60 days (extendable with approval). If the seized assets are satisfactorily explained and declared income, they are returned. If not, they can be applied against tax demands arising from the assessment.

5. What is a Section 153A assessment and how does it differ from a regular assessment?

After a search and seizure, the Income Tax Department issues notices under Section 153A for the six assessment years preceding the search year. These assessments replace the regular ones and allow the department to reassess income for those years based on seized material and any other evidence found during the search.

6. Can I be penalised even if I cooperate fully during a search?

Cooperation reduces risk but does not automatically eliminate penalties. Penalties under Section 271AAB apply specifically to undisclosed income found during a search. However, making a voluntary declaration of undisclosed income during the search (with your advisor’s guidance) can attract a lower penalty rate of 30% compared to 60% if it is detected without disclosure.

7. How can Adwani and Company help if my business has already undergone a search and seizure?

Adwani and Company provides comprehensive post-search advisory — from reviewing the Panchnama and preparing your Section 153A assessment response to representing you in appeals before the ITAT. Contact us today for an immediate consultation.

Dr Haresh Adwani holds a PhD in Commerce and brings over 20 years of expertise in GST compliance, income tax advisory, FEMA, and corporate law. Services include GST audit, ITR filing, GST appeal representation, notice response, NRI taxation, and FEMA compliance.