Dr. Haresh Adwani, May 2026, 9 min read

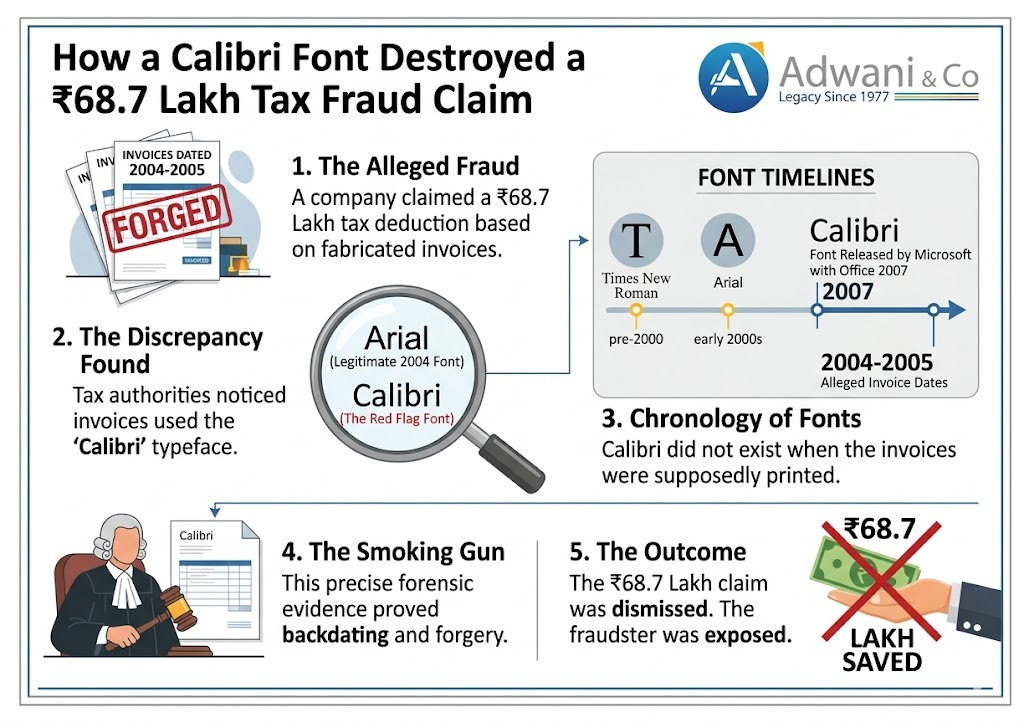

A taxpayer walked into the Income Tax Department in Hyderabad believing their paperwork was airtight. They had ₹68.7 lakh in claimed deductions, a pile of improvement bills spanning six years, and a taxable gain reduced to an almost negligible ₹24,774. Everything looked fine until an officer noticed one small, damning detail: the font.

In what has become a landmark example of how tax fraud detection in India is growing increasingly sophisticated, the Calibri font tax fraud case from Hyderabad is a stark reminder that document authenticity matters more than ever. Whether you are a business owner, a salaried professional, or an NRI dealing with property transactions, this case has lessons that could protect you or expose you.

At Adwani and Company, led by Dr. Haresh Adwani a PhD holder in Commerce and a law graduate with deep expertise in direct taxation we have seen firsthand how easily avoidable mistakes can trigger scrutiny. Let us walk you through exactly what happened, why it matters, and what you must do to stay compliant.

The Calibri Font Tax Fraud Case: What Actually Happened

The case centers on a property transaction in Hyderabad. A taxpayer sold a residential property for ₹1.4 crore. Under the provisions of the Income Tax Act, 1961, Long-Term Capital Gains (LTCG) on the sale of property held for more than two years are taxable. However, the law also permits deductions for cost of improvement genuine expenditures made to enhance the value of the property.

The taxpayer submitted a set of improvement bills dated between 2002 and 2008, collectively totaling ₹68.7 lakh. After applying these as deductions against the sale proceeds, the taxable long-term capital gain was reduced to a mere ₹24,774. On paper, this was a legitimate, well-structured claim. In practice, it was a fabrication and an expensive one.

The Income Tax Department’s scrutiny officer flagged this anachronism. Faced with an undeniable factual inconsistency, the taxpayer withdrew the fraudulent claim and paid the correct tax amount. There was no lengthy litigation the font spoke for itself.

Understanding Long-Term Capital Gains and Calibri Font Tax Fraud Risks

To understand the full implications of this Calibri font tax fraud, you need to understand how LTCG deductions work under Indian tax law. According to the Income Tax Department of India, the taxable capital gain on the sale of a long-held asset is calculated as:

Taxable LTCG = Sale Price (Indexed Cost of Acquisition + Indexed Cost of Improvement)

The cost of improvement covers genuine renovation, reconstruction, or structural enhancement expenditures that increase the asset’s value. These must be supported by original bills, receipts, and in many cases corroborating evidence such as contractor agreements or building permits.

As Dr. Haresh Adwani frequently advises clients at Adwani and Company: “The law does not punish genuine claims. It punishes fabricated ones. The problem is that many taxpayers do not preserve original records and then attempt to reconstruct them at the time of sale often with modern tools that inadvertently leave digital fingerprints.”

→ Learn more about our Ultimate Financial Modeling to Normalize Business Valuation in India

Real Numerical Example: How the ₹68.7 Lakh Calibri Fraud Unravelled

Practical Illustration

Property Sale Tax Calculation — Fraudulent vs. Legitimate

| Item | Fraudulent Claim | Actual (After Withdrawal) |

|---|---|---|

| Sale Price of Property | ₹1,40,00,000 | ₹1,40,00,000 |

| Indexed Cost of Acquisition | ₹71,25,226 | ₹71,25,226 |

| Claimed Improvement Costs | ₹68,70,000 (fake) | ₹0 |

| Taxable Long-Term Capital Gain | ₹24,774 | ₹68,74,774 |

| Tax Liability @ 20% (approx.) | ≈ ₹4,955 | ≈ ₹13,74,955 |

Note: Indexation applies per the Cost Inflation Index notified by the Income Tax Department each financial year. Consult a CA for your exact computation.

The difference in tax liability was staggering nearly ₹13.7 lakh in tax that would have gone unpaid, not counting any penalties or interest under Sections 270A and 234B of the Income Tax Act. This is precisely why the Income Tax Department scrutinizes improvement cost claims so rigorously.

Why Document Forensics in Tax Fraud Detection Is Growing in India

The Calibri font tax fraud case is not an isolated incident. It is a window into a much broader trend. India’s tax administration has been investing significantly in advanced analytics, Artificial Intelligence tools, and document forensics as part of the broader digital transformation of the Income Tax Department.

The department’s data analytics wing powered by integrated systems that link PAN, GST, MCA filings, and bank records can now triangulate inconsistencies that would have gone undetected a decade ago. Metadata embedded in digital documents, font version histories, and even printer calibration patterns have all been used internationally to expose forged records.

In India, the GST Portal and the Ministry of Corporate Affairs (MCA) maintain interconnected registries. A claimed business expenditure that does not appear in a supplier’s GST return will immediately raise a red flag. Similarly, improvement bills from contractors who were never registered, never filed returns, or ceased to exist years ago are vulnerable to challenge.

What Forensic Auditors Look for in Suspicious Documents

- Font anachronisms : as in the Calibri font tax fraud case, fonts postdating the document’s claimed date

- Metadata mismatches : PDF creation dates that contradict stated document dates

- Printer and scanner artifacts : inkjet patterns inconsistent with era-appropriate technology

- Paper quality and ageing : physical documents that show signs of artificial ageing

- Signature inconsistencies : graphological analysis of handwriting

- Cross-referencing with GST/TDS records : verifying whether the contractor claimed income from the project

Expert Insight from Adwani and CompanyAccording toDr. Haresh Adwani, “The single most effective protection against scrutiny is maintaining contemporaneous, original records. Store bills the day you receive them. Photograph physical receipts. Cross-verify with your contractor’s GST returns. An authentic paper trail is your strongest defence.”

Calibri Font Tax Fraud Lessons for NRIs, Business Owners, and Professionals

The Calibri font tax fraud case resonates especially loudly for three groups: Non-Resident Indians managing property in India, business owners reconstructing historical expenditure records, and professionals advising clients on capital gains transactions.

For NRIs: Extra Scrutiny on Property Sales

NRIs selling property in India are subject to TDS deductions on the buyer’s side, and their capital gains are audited more frequently than resident taxpayers. Fabricating improvement bills is especially risky when the underlying property was acquired decades ago and supporting contractors may no longer be traceable. → Read our detailed guide on NRI Tax Rules: 10 Critical Questions Before Returning to India

For Business Owners: GST Linked Verification

Business improvement or renovation costs claimed for commercial properties must now be reconciled against the GST invoices filed by the vendor. If a contractor was unregistered or did not file returns, any bills issued by them become suspect. The Income Tax Department can and does cross-verify these records with the GST portal.

For CA Firms and Tax Professionals

At Adwani and Company, our document review process includes timeline verification, metadata checks, and cross-referencing with publicly available GST and MCA records before any improvement cost deduction is claimed on behalf of clients. This is not excessive caution it is professional due diligence.

How to Legitimately Reduce Long-Term Capital Gains Tax in India

The good news is that the Income Tax Act provides several legitimate avenues to reduce your LTCG liability — none of which require fabricated bills or font gambles.

- Section 54 Exemption: Reinvest the capital gains in a new residential property within two years of sale (or construct within three years). This is one of the most widely used, fully legitimate exemptions available.

- Section 54EC Bonds: Invest up to ₹50 lakh in specified bonds (REC, NHAI) within six months of the sale. The invested amount is exempt from LTCG taxation.

- Indexation Benefit: Use the government’s published Cost Inflation Index (CII) to inflate your acquisition cost, significantly reducing the computed gain.

- Genuine Improvement Costs: Claim genuine, well-documented renovation and improvement expenditures. Original bills, bank payment records, and contractor GST invoices form the backbone of a defensible claim.

- Capital Gains Account Scheme: If you cannot immediately reinvest, deposit the gains in a Capital Gains Account with a scheduled bank before the ITR filing deadline.

✅ Key TakeawayEvery rupee of tax you save through legitimate means is a rupee the law intended you to keep. Every rupee saved through falsification is a liability that compounds — with interest, penalties, and potential prosecution under Section 276C of the Income Tax Act.

Calibri Font Tax Fraud and the Broader Message: Records Are Your Shield

The deeper message of the Calibri font tax fraud case is not about technology. It is about culture. Indian taxpayers and businesses have historically underinvested in record-keeping infrastructure. Physical receipts are lost; digital documents are not backed up; contractor relationships are informal and undocumented.

As India’s tax administration increasingly converges GST, income tax, TDS, and MCA data into unified analytical systems, the tolerance for informal or reconstructed records is approaching zero. The Income Tax Department has explicitly stated in recent departmental communications that unexplained discrepancies between filed returns and third-party data will trigger automated scrutiny.

Dr. Haresh Adwani summarizes it plainly: “In 2002, a typing error might have gone unnoticed. In 2026, the tax system has a longer memory than you do and it does not forget fonts.”

Frequently Asked Questions

01. What is Calibri font tax fraud case in India?

The Calibri font tax fraud case refers to a recent incident in Hyderabad where a taxpayer submitted fake property improvement bills dated 2002–2008 to claim ₹68.7 lakh in LTCG deductions. One bill was typed in Calibri (Body) font, which was not publicly available until around 2006, exposing the document as fraudulent.

02. Can I claim improvement costs to reduce Long Term Capital Gains tax?

Yes, genuine improvement costs are deductible under the Income Tax Act, 1961. However, you must have original, authentic supporting documents bills, receipts, bank payment records, and GST invoices from the contractor. Fabricated or reconstructed bills are a criminal offence.

03.How does Income Tax department detect fake bill?

The department uses multiple methods: document forensics (including font timeline analysis), metadata extraction from digital files, cross-referencing with GST returns, TDS records, MCA filings, and bank transaction data. Advanced analytics tools flag anomalies automatically.

04. What are the penalties for submitting fake bills to Income Tax Department?

Penalties can include 200% of the tax evaded under Section 270A (misreporting), interest under Sections 234A/B/C, and criminal prosecution under Section 276C for willful evasion, which can result in imprisonment of up to seven years along with a fine.

05. How can NRI’s legally save tax on property sales in India

NRIs can use Section 54 (reinvestment in residential property), Section 54EC (capital gains bonds up to ₹50 lakh), indexation benefits, and genuine documented improvement costs. Consulting a specialist CA firm like Adwani and Company is strongly recommended before filing.

06.What records should i maintain for property improvement cost?

Maintain original paper receipts and bills, digital scans with unaltered metadata, bank payment statements or cheque records, contractor agreements, GST invoices from registered vendors, and any municipal permits related to renovation work. Keep these for at least six years from the date of filing the relevant ITR.

Conclusion

The Calibri font tax fraud case is a watershed moment in Indian tax enforcement. What began as a seemingly mundane property transaction unravelled because of a microscopic detail a typeface that didn’t exist when a document claimed to have been created. The taxpayer lost ₹68.7 lakh in deductions, faced potential penalties, and perhaps most damagingly lost the benefit of the doubt.

The lesson is not that the Income Tax Department is infallible or omniscient. The lesson is that authenticity is non-negotiable. Genuine records, maintained at the time of the transaction, remain your most powerful legal protection in any tax dispute.

India’s tax system is moving toward full digital integration GST, Income Tax, MCA, TDS, and bank data are increasingly speaking to each other in real time. In this environment, a shortcut taken in 2002 can cost you in 2026. A font can sink a ₹68.7 lakh claim.

About the Author

Dr. Haresh Adwani

Ph.D. in Commerce | Law Graduate | Managing Partner, Adwani & Co LLP Dr. Haresh Adwani holds a Ph.D. in Commerce and is a qualified Law graduate with over two decades of hands-on experience in GST advisory, direct taxation, and statutory compliance for businesses across