A client called me last year with a familiar problem. His business had made professional payments across two financial years without deducting TDS. Nobody had caught it at the time. The issue only surfaced during his tax audit and by then, interest had already been building for months.

His first question was simple: “Can Form 26A fix this?”

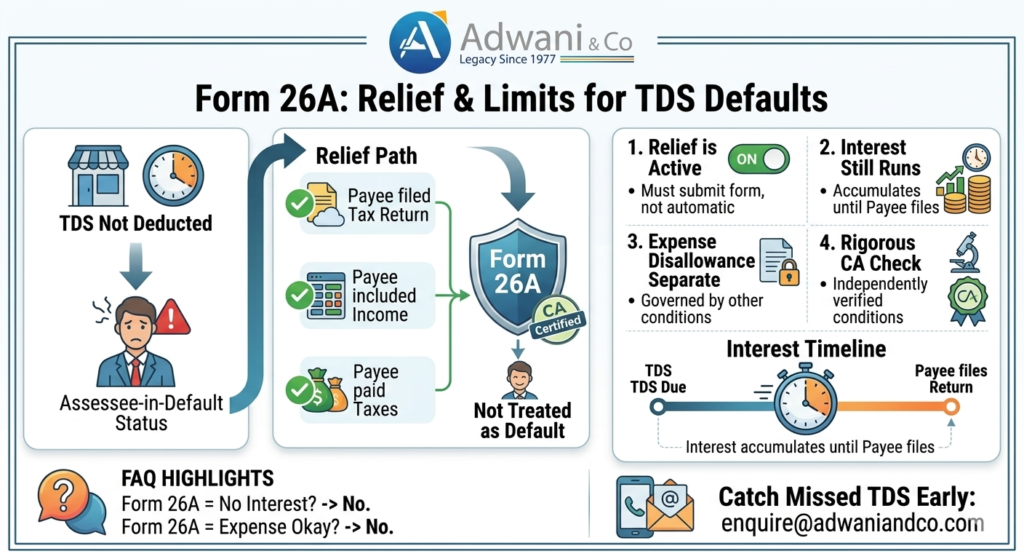

The honest answer is: partly. Form 26A is a genuine and meaningful relief mechanism. But it does not resolve everything, and businesses that assume it does often find themselves with an unexpected interest burden.

Form 26A helps a payer avoid being treated as an assesse in default under Section 201 if the payee has filed their return, included the income, and paid taxes. However, it does not eliminate interest under Section 201(1A) or guarantee expense allowability under Section 40(a)(ia).

Here is what Form 26A actually does and where it stops.

What Is Form 26A and What Does It Do in a TDS Default Situation?

When a payer fails to deduct TDS on a payment, the Income Tax Department typically treats that payer as an assessee-in-default under Section 201(1). This is not a minor label. It carries real consequences: disallowance of the expense under Section 40(a)(ia), interest liability under Section 201(1A), and a formal default on your record.

The proviso to Section 201(1) offers a conditional path out. A payer will not be treated as an assessee-in-default despite failing to deduct TDS if all three of the following conditions are met on the payee’s side:

- The payee (a resident) has filed their return of income under Section 139.

- The payee has included this specific income in that return.

- The payee has paid the tax due on this income.

If all three are satisfied, a Chartered Accountant certifies these facts in Form 26A. Once submitted, the payer escapes the assessee-in-default classification under Section 201(1).

That is meaningful relief. But many businesses stop reading here and that is precisely where the problem starts.

In a typical Form 26A TDS default case, understanding these limitations is critical to avoid further tax exposure.

Also read:

https://www.adwaniandco.com/blog/paid-your-taxes-honestly-still-got-an-income-tax-notice-2026-guide

Limitations of Form 26A in TDS Default Cases

Understanding the limits of Form 26A is just as important as knowing what it provides. Here are the four key boundaries businesses and their advisors must be aware of.

Limit 1 Relief Is Not Automatic

Form 26A must be formally obtained and submitted. Simply knowing you may be eligible does not protect you. The default remains on record until the form is actually furnished through the proper procedure. Acting on it early matters.

Limit 2 Interest Under Section 201(1A) Still Applies

New subsection to be inserted within the existing “Interest Liability Under Section 201(1A)” section.

What the Interest Actually Costs

Understanding that interest applies is one thing. Knowing the rate is what makes the risk real.

Section 201(1A) prescribes two distinct rates depending on the nature of the default:

- Failure to deduct TDS at all: Interest at 1% per month (or part of a month) on the amount of tax that should have been deducted, running from the date TDS was required to be deducted to the date the payee files their return of income.

- TDS deducted but not remitted to the government: Interest at 1.5% per month (or part of a month) on the amount deducted, running from the date of deduction to the date of actual payment.

Both rates may appear modest in isolation, but they compound against time and against the full tax amount not just the delayed portion. In a case where TDS was required in, say, April of a financial year and the payee only files their return fourteen months later in June of the following year, the interest calculation covers that entire period. At 1% per month, that is already a 14% charge on the TDS amount, before any penalties are considered.

The interest under Section 201(1A) is treated by law as a compensatory charge not a penalty for the period during which the government was denied timely access to the tax. This characterisation was affirmed by the Supreme Court in Hindustan Coca-Cola Beverages Pvt. Ltd. v. CIT (2007) 293 ITR 226 (SC), where the Court made clear that even where the payee has paid the underlying tax and the payer is not treated as an assessee-in-default, the compensatory interest still runs its course. It does not disappear simply because the substantive default has been regularised through Form 26A.

For businesses reviewing their books after a TDS audit finding, this calculation is usually the first number their CA should work out because it tells you exactly what is at stake before you even begin the Form 26A process.

Limit 3 Disallowance Under Section 40(a)(ia) Is a Separate Question

Limit 3 Disallowance Under Section 40(a)(ia) Is a Separate Question

Form 26A only addresses Section 201(1). Whether your expense is actually allowed as a deduction is governed by Section 40(a)(ia), which has its own conditions and its own logic.

Here is how Section 40(a)(ia) operates. When a payer fails to deduct TDS on payments such as professional fees, contract payments, rent, commission, interest, or royalties made to a resident, the law restricts the deduction of that expense in the year of default. The current restriction reduced from 100% to 30% by the Finance Act 2014, effective from Assessment Year 2015-16 means that 30% of the gross payment can be disallowed and added back to taxable income. For a business making substantial payments without TDS, this can translate into a meaningful increase in tax liability, not just a compliance note.

The critical link between Form 26A and Section 40(a)(ia) lies in the second proviso to that section, read with the first proviso to Section 201(1). If Form 26A conditions are satisfied payee has filed a return, included the income, and paid taxes then the payer is deemed to have deducted and paid the TDS on the date the payee filed their return of income. As a result, the disallowance under Section 40(a)(ia) does not apply for that year.

But this only works if Form 26A is filed. If the form is not furnished even where the payee has genuinely paid taxes the payer cannot claim this relief automatically. The deemed-payment fiction under the second proviso is triggered only by the act of furnishing the form through the prescribed process.

Two situations where the expense remains at risk despite a payee having paid taxes:

- Form 26A is not filed before the assessment is concluded. Courts and the CBDT have consistently taken the position that Form 26A must be furnished before the assessment proceedings are finalised. Filing it after an assessment order is passed may not provide retrospective protection.

- The payee is a non-resident. Section 40(a)(ia) covers payments to residents. For payments to non-residents, the relevant provision is Section 40(a)(i), and neither Form 26A nor the proviso to Section 201(1) applies in the same way. (This is addressed separately below under the non-resident limitation.)

The practical takeaway: Form 26A and expense allowability under Section 40(a)(ia) are related but distinct outcomes. Getting the form in place, accurately and on time, is what connects the payee’s compliance to the payer’s tax relief. Without it, the payee having paid taxes is a fact but one that the payer cannot use in their own assessment.

Limit 4 The CA Certification Must Be Rigorous

The Chartered Accountant issuing Form 26A must independently verify all three payee conditions: that the return was filed, that this income was included, and that tax was paid. If this verification is done carelessly or without proper documentary checks, the certification itself can be challenged creating fresh risk rather than resolving the existing one.

Limit 5 Form 26A Does Not Apply to Non-Resident Payees

The proviso to Section 201(1) which enables Form 26A relief applies only where the payee is a resident of India. The statute is explicit on this point. If a business makes a payment to a non-resident — whether a foreign company, NRI, or overseas service provider — without deducting TDS under the applicable section (most commonly Section 195), Form 26A cannot be used to seek relief.

For non-resident payments, the TDS obligation has a different character altogether. The government’s collection mechanism for non-resident income depends substantially on withholding at source because once funds leave India, enforcement becomes significantly more complex. Courts have reinforced this view. In matters involving payments to non-residents without deduction under Section 195, tribunals have consistently declined to extend the Form 26A protection, even where the non-resident has filed a return and paid taxes in India.

Businesses operating in cross-border vendor relationships, making royalty or technical service payments overseas, or buying immovable property from NRIs need to be aware that this relief simply does not extend to their situation. The exposure under Section 201(1) in a non-resident default remains unresolved by Form 26A, and the path to remediation if one exists lies in different provisions, including DTAA applicability, lower deduction certificates under Section 197, or representations to the Assessing Officer under Section 195(2) and (3).

If your business makes both resident and non-resident payments, a compliance review should treat these as two distinct categories with different risk profiles and different available remedies.

Interest Liability Under Section 201(1A) in TDS Default Cases

Many businesses assume that once Form 26A is obtained, the TDS default is fully resolved. That assumption is incorrect, and the consequences of getting this wrong can be significant.

Interest under Section 201(1A) is not a penalty. It is treated by law as a compensatory charge for the period during which the government was deprived of timely tax collection. The interest runs from the date on which TDS was required to be deducted to the date on which the payee actually files their return of income. This is the case even if the payee has correctly disclosed the income and paid all taxes.

In practice, there is almost always a time gap. A payment may be made during the financial year, but the payee’s return is typically filed months later sometimes beyond the due date. During this entire period, interest accrues without interruption.

The real problem arises because TDS defaults are rarely identified immediately. In most cases including my client’s situation the issue surfaces during a statutory audit, tax audit, or income tax scrutiny. By that point, a substantial period has already passed. What started as a minor compliance lapse has become meaningful financial exposure, purely because of time.

The practical advice here is straightforward: act early. If you suspect a TDS default may exist in your books, get a structured compliance review done before it surfaces in a scrutiny notice. The earlier the detection, the lower the interest exposure.

Judicial and CBDT Context: Why the Law Landed Here:

The Form 26A mechanism did not emerge from a vacuum. It was the legislature’s codification of a principle that courts had already been applying — that once the government has received its tax from the payee, the payer should not be subjected to double jeopardy merely for the failure to withhold it.

The Supreme Court in Hindustan Coca-Cola Beverages Pvt. Ltd. v. CIT (2007) 293 ITR 226 (SC) laid the conceptual groundwork. The Court held that if the payee has paid tax on the income received, treating the payer as an assessee-in-default for failure to deduct results in the government recovering the same tax twice. CBDT Circular No. 275/201/95-IT(B) dated 29th January 1997 had already taken a similar position administratively. The Finance Act 2012 formalised this logic by inserting the first proviso to Section 201(1) and, through Notification No. 37/2012, prescribing Rule 31ACB and Form 26A.

What the Supreme Court also made clear — and what CBDT Circular No. 11/2017 subsequently addressed — is that interest under Section 201(1A) occupies a different space. The Court characterised it as compensatory rather than penal: it is the price the payer pays for having denied the government access to the withheld amount during the intervening period. This distinction matters because it means the interest survives even the most complete Form 26A filing. Courts do not treat the two — assessee-in-default status and interest liability — as a single outcome that Form 26A resolves together.

CBDT Circular No. 11/2017 also introduced a narrow relief for interest waiver in specific cases of TDS default under Section 201(1A)(i) — for example, where a deductor acted on a jurisdictional High Court order that was subsequently reversed, or in cases involving non-residents where the DTAA was misapplied in good faith. These waivers require an application to the concerned CCIT or DGIT and are granted in exceptional circumstances, not as a matter of routine. Businesses in genuinely ambiguous positions may want to explore whether their facts qualify under these guidelines — but should not assume the waiver as a given.

The overall judicial trajectory is consistent: courts protect bona fide payers from double taxation but do not relieve them of the time-value cost of delayed withholding. Form 26A gives you the former. It cannot give you the latter.

How Form 26A Is Filed: The TRACES Process in Practice

The blog so far has focused on what Form 26A does and where it stops. But a business that has identified a TDS default and wants to act on it has one immediate practical question: how does this actually get done?

Form 26A is filed electronically through the TRACES portal (tdscpc.gov.in), the government’s TDS reconciliation and correction platform. The process is dual-step, involving both the deductor and the Chartered Accountant separately.

Step 1 — The Deductor Initiates the Request

The deductor logs into TRACES and raises a request for Form 26A based on the PAN of the payee for whom relief is being sought. The system auto-populates transactions from the deductor’s filed TDS returns where non-deduction or short-deduction is reflected. The deductor identifies the specific transactions, generates the annexure in the prescribed format, and submits it digitally — either using a Digital Signature Certificate (DSC) or through Electronic Verification Code (EVC). The form then moves to a status of “Sent to E-Filing.”

Step 2 — The Chartered Accountant Certifies

The assigned CA receives the request in their Income Tax e-Filing portal login under Worklist → For Your Action. Before certifying, the CA must independently verify the three conditions that the law requires: that the payee has filed their return under Section 139, that the specific income paid by the deductor is included in that return, and that the tax due on the declared income has been paid. This verification must be based on actual examination of the payee’s return, acknowledgement, Form 26AS, and tax payment records — not merely on representations made by the payee or the deductor.

The CA fills in the payee’s return filing details — date of filing, acknowledgement number, ITR form type, declared income, tax payable, and tax paid — and submits the certificate in the prescribed Annexure A format, using their own DSC.

Step 3 — The Deductor Finalises Submission

Once the CA submits, the deductor logs back into the e-Filing portal and submits Form 26A using DSC or EVC. TRACES then processes the form and recalculates the TDS default position. If accepted, the deductor’s status changes from assessee-in-default to relieved, and TRACES recomputes the interest under Section 201(1A) for the applicable period.

What the CA Must Actually Verify

Rule 31ACB of the Income Tax Rules, 1962, which prescribes Form 26A, requires that the CA examine the relevant accounts, documents, and records of the payee — not merely accept verbal confirmation. In practice, this means obtaining and retaining copies of:

- The payee’s ITR acknowledgement for the relevant assessment year

- The payee’s tax computation showing the disputed income was included

- Evidence of tax payment (Challan / Form 26AS / AIS)

- The deductor’s TDS return showing the transaction in question

A certification that is done without this documentation is not merely careless — it is professionally exposed, and could be challenged during assessment, converting a resolved matter into an active dispute.

Conclusion .

Form 26A is useful in a TDS default scenario, but it is not a complete solution.

Form 26A is a useful and legally sound mechanism. When used correctly, with proper CA verification, it provides genuine protection against the assessee-in-default label under Section 201(1).

But it is not a complete fix. Interest under Section 201(1A) still runs. Expense disallowance under Section 40(a)(ia) is a separate question. And the certification itself carries responsibility it must be done with proper documentary verification, not as a formality.

If your business has missed TDS deductions or if you are not entirely sure whether you have a structured compliance review before scrutiny is always the better path. Catching the issue early limits the damage; discovering it during a notice limits your options.

Frequently Asked Questions About Form 26A TDS Default

1. What is Form 26A in TDS?

Form 26A is a certificate issued by a Chartered Accountant confirming that the payee has included the relevant income in their return of income and paid the applicable taxes. When furnished properly, it allows the payer to claim relief from being treated as an assessee-in-default under Section 201(1) of the Income Tax Act. (Learn more about TDS defaults and compliance https://www.adwaniandco.com/services

2. Does Form 26A completely remove TDS liability?

No. Form 26A only removes the assessee-in-default classification under Section 201(1), subject to all three payee conditions being met. Interest liability under Section 201(1A) still applies, and the question of expense disallowance under Section 40(a)(ia) is an entirely separate matter.

3. Is interest payable even after filing Form 26A?

Yes. Interest under Section 201(1A) continues to apply and is calculated from the date TDS was originally required to be deducted to the date the payee files their return of income. Form 26A does not eliminate this interest.

4. When should Form 26A be filed?

Form 26A should be filed once it is confirmed that the payee has filed their return of income, included the relevant income in that return, and paid the tax due. The sooner this is done after a default is identified, the better as delay increases interest exposure.

5. What happens if Form 26A is not filed?

Without Form 26A, the payer remains classified as an assessee-in-default under Section 201(1). This can result in a tax demand, interest under Section 201(1A), and potential disallowance of the expense under Section 40(a)(ia). The default also stays on formal record, which can complicate future assessments.