A Swipe Today, a Notice Tomorrow?

Imagine this scenario. You have paid ₹12 lakh towards your credit card bills throughout the financial year. Your declared income? Just ₹6 lakh. You have never evaded tax intentionally. Your family uses your card. Friends occasionally swipe and repay. Business and personal expenses are all tangled up on a single plastic card.

Sounds familiar, doesn’t it?

Now here is the part most people miss. The Income Tax Department does not see each individual swipe. They do not know whether you bought groceries, booked a flight, or paid a hospital bill. What they see is one consolidated number: total credit card payments of ₹12,00,000. And when that number does not match your declared income, it raises a red flag that can lead to a credit card payments income tax notice.

At Adwani and Company (https://www.adwaniandco.com/), we have seen this situation unfold more times than we can count. Professionals, salaried individuals, small business owners all caught off guard by a simple mismatch between their spending and their reported income. This blog will walk you through exactly how the Income Tax Department tracks your credit card payments, what Section 69C means for you, and how you can protect yourself from unnecessary scrutiny.

As CA Dipesh Gurubakshani recently highlighted in a powerful insight: “It is not about how much you spend. It is about how well you can explain it.” This single line captures the reality that millions of credit card holders in India need to understand before it is too late.Understanding how a credit card income tax notice works is the first step toward protecting yourself from unnecessary scrutiny.

Also Read:

https://www.adwaniandco.com/blog/gst-appeal-pre-deposit-apl-01-fix-april-2026

How the Income Tax Department Tracks Your Credit Card Payments

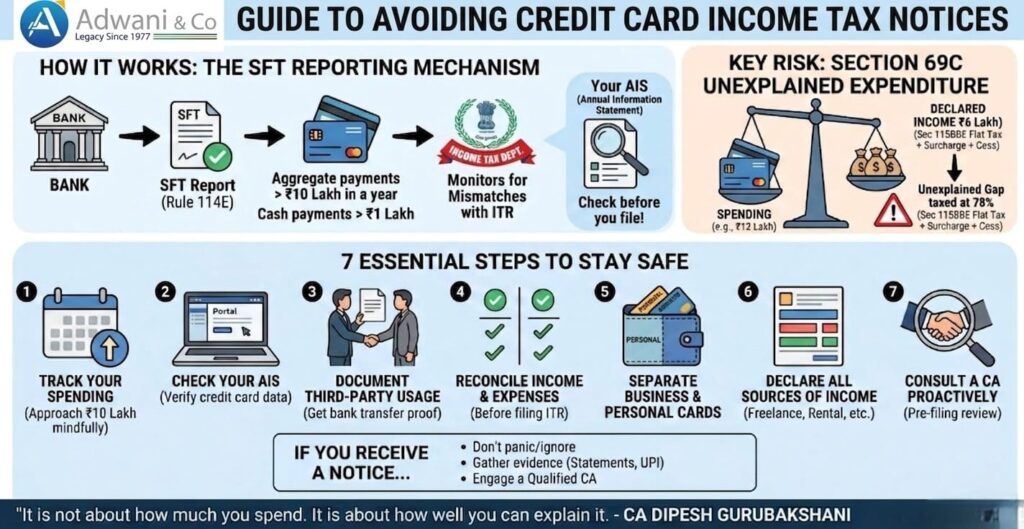

The SFT Reporting Mechanism Under Rule 114E

If you think your credit card payments are a private matter between you and your bank, think again. Under Rule 114E of the Income Tax Rules, financial institutions including banks and credit card companies are required to file a Statement of Financial Transactions (SFT) with the Income Tax Department.

Here is the critical threshold: if your total credit card payments exceed ₹10 lakh in a single financial year, your bank is legally obligated to report this to the department. This information is then reflected in your Annual Information Statement (AIS), which the Income Tax Department uses to cross-verify your filed returns.

According to the Income Tax Department of India (https://www.incometax.gov.in), the AIS is a comprehensive statement that contains details of all financial transactions carried out by a taxpayer during the year. It includes information about savings account interest, dividends, securities transactions, property purchases and yes, credit card payments.

The takeaway? Every rupee you pay towards your credit card is being watched. Not in a sinister way, but through a data-driven compliance framework designed to identify discrepancies.

What Exactly Gets Reported?

Let us be specific. The SFT report for credit card payments includes:

- Aggregate credit card bill payments made during the financial year.

- Cash payments exceeding ₹1 lakh against credit card bills.

- Any single transaction exceeding ₹10 lakh in credit card payments.

This means even if no single transaction was large, if the cumulative payments cross the threshold, it gets flagged. And this is precisely where the mismatch between income and credit card payments income tax notice issues begin.

Your Annual Information Statement Reveals Everything

Since the introduction of the Annual Information Statement (AIS), taxpayers can now see exactly what the government sees. Your AIS, accessible through the Income Tax e-filing portal, displays:

- Total credit card payments made during the year

- High-value cash deposits

- Mutual fund and stock transactions

- Property purchases

- Foreign remittances

When your credit card payments and income tax return show a glaring mismatch, the system automatically flags your profile. This is not a manual process it is algorithm-driven, and it is getting smarter every year.

Why a Credit Card Payments Income Tax Notice Gets Triggered

The Simple Math the Tax Department Uses

The logic is straightforward. If your declared income is ₹6 lakh but your credit card payments total ₹12 lakh, the department has a legitimate question: Where did the remaining ₹6 lakh come from?

You might have perfectly valid explanations:

- Your spouse or parents used your card and reimbursed you

- A friend swiped for a purchase and transferred money back

- Business expenses were routed through your personal card

- You used savings from previous years

But here is the problem valid explanations need valid documentation. Without proper records, you are left scrambling to prove the source of funds after receiving a credit card payments income tax notice.

| Situation | Tax Impact | Action |

| Payments > ₹10 lakh | Reported in AIS (SFT) | Track yearly usage |

| Spending > Income | Notice risk | Reconcile & justify source |

| Third-party usage | Treated as your expense | Keep bank proof |

| No explanation | Tax under Sec 69C (~78%) | Maintain documentation |

Here’s a real-world case of a credit card income tax notice

Let us share a practical example that we frequently encounter at Adwani and Company.

Mr. Sharma (name changed for privacy) is a mid-level IT professional in Pune.

- Annual salary income declared: ₹8,50,000

- Total credit card payments in FY: ₹14,20,000

- Cash deposits in savings account: ₹2,50,000

- Mutual fund investments: ₹1,80,000

Now look at this from the tax department’s perspective:

- Income: ₹8.5 lakh

- Total outflows (credit card + investments + deposits): ₹18.5 lakh

Where did the extra ₹10 lakh come from?

Mr. Sharma’s wife, a homemaker, frequently used his credit card for household purchases, children’s tuition fees, and online shopping. His parents, who lived with him, occasionally used the card for medical expenses. His brother had repaid ₹3 lakh for a shared vacation.

Mr. Sharma received a notice under Section 69C asking him to explain the source of funds for his credit card payments. Because he had maintained no records of reimbursements from family members and had no paper trail showing the flow of funds, what should have been a simple clarification turned into a stressful, months-long process.

At Adwani and Company, our team helped Mr. Sharma compile bank statements, family member declarations, and a detailed reconciliation of every major transaction. The case was eventually resolved but it could have been entirely avoided with proper planning.

Understanding Section 69C: Unexplained Expenditure and Your Credit Card

What Is Section 69C?

Section 69C of the Income Tax Act, 1961 deals with unexplained expenditure. If the Assessing Officer finds that a taxpayer has incurred expenditure that is not satisfactorily explained, and the source of such expenditure is not disclosed, the amount may be deemed as income and taxed accordingly.

In the context of credit card payments, this means:

- If your total credit card payments significantly exceed your declared income

- And you cannot explain the source of those funds

- the excess amount can be treated as your income and taxed at the applicable rate — 60% flat tax + 25% surcharge + 4% cess, resulting in an effective rate of 78% under Section 115BBE.

Let us put this in perspective with numbers:

If ₹5 lakh of your credit card spending is deemed unexplained under Section 69C, you could face a tax demand of approximately ₹3,90,000 (effective rate of 78%) on ₹5 lakh deemed as unexplained income — and this can go even higher if penalty under Section 271AAC is also levied) on money you may have already spent and possibly did not even owe tax on, had you documented it properly.

How Section 69C Applies to Your Credit Card Payments Income Tax Notice

The section does not require the department to prove that you earned undisclosed income. The burden of proof shifts to you, the taxpayer. You must demonstrate:

- Source of funds Where did the money come from?

- Nature of transactions What were the payments for?

- Reimbursement proof If someone else used your card, can you prove it?

This is a significant legal burden, and it is one that catches many taxpayers unprepared. This is precisely why Dr. Haresh Adwani consistently reminds clients: “Section 69C does not punish spending. It punishes the inability to explain spending. Documentation is your shield.”

For a deeper understanding of how tax provisions affect your finances, explore our tax advisory services at Adwani and Company (https://www.adwaniandco.com/).

A credit card income tax notice under Section 69C can result in your unexplained spending being taxed at 60% plus surcharge.

Common Scenarios That Lead to a Credit Card Payments Income Tax Notice

1. Family Members Using Your Credit Card

This is perhaps the most common scenario in Indian households. Your card, your liability but the spending is collective. The problem? Banks report the payment in your name, and the tax department associates it with your income.

Solution: Maintain a simple monthly log of who spent what. Ask family members to transfer their share to your account via bank transfer (not cash) so there is a clear trail.

2. Friends Swiping and Repaying Later

We have all been there a group dinner, a vacation booking, a last-minute purchase. You swipe, they repay. But if the repayment is in cash or through informal channels, there is no documentary evidence.

Solution: Always insist on bank transfers for repayments. A simple UPI transfer creates a timestamped, traceable record.

3. Mixing Business and Personal Expenses

Small business owners and freelancers are particularly vulnerable. When business expenses like client entertainment, travel, or supplies are charged to a personal credit card, the lines get blurred.

Solution: Maintain separate credit cards for business and personal use. If that is not possible, keep a detailed spreadsheet categorizing each transaction. At Adwani and Company, we recommend this as a non-negotiable best practice for all our business clients.

4. Reward-Chasing and Card Churning

Many financially savvy individuals route all payments rent, insurance premiums, mutual fund SIPs through credit cards to maximize reward points. While there is nothing illegal about this, it inflates the total payment figure reported under SFT.

Solution: Ensure your ITR accurately reflects all sources of income, including savings and investments, that justify the total outflow.

5. EMI Conversions on High-Value Purchases

High-value purchases converted to EMIs still reflect as lump-sum payments in SFT reporting. A ₹2 lakh laptop purchase on EMI appears as a ₹2 lakh credit card payment even though you are paying it in monthly installments.

Solution: Keep purchase receipts and EMI conversion confirmation emails as supporting documentation.

Each of these everyday situations can quietly build up the spending gap that eventually triggers a credit card income tax notice from the department.

How to Protect Yourself from a Credit Card Payments Income Tax Notice

Step 1: Track Your Annual Credit Card Payments

This sounds obvious, but most people do not do it. At the start of every financial year, set up a simple tracker a spreadsheet, an app, or even a diary to log your monthly credit card payments. If you are approaching ₹10 lakh, be extra mindful about documentation.

Step 2: Check Your Annual Information Statement (AIS)

The AIS is available on the Income Tax e-Filing Portal (https://www.incometax.gov.in). Review it before filing your return. If the credit card payment figure does not match your records, investigate the discrepancy before the department does.

Step 3: Maintain Documentation for Third-Party Usage

If anyone else uses your credit card, create a paper trail. Bank transfers, written acknowledgements, or even email confirmations can serve as evidence.

Step 4: Reconcile Income and Expenditure Before Filing

Before filing your ITR, do a basic reconciliation. Does your total expenditure (including credit card payments, EMIs, rent, and cash withdrawals) align with your declared income plus savings? If there is a gap, identify and document the source.

Step 5: Separate Business and Personal Cards

If you are a freelancer, consultant, or business owner, this is non-negotiable. Use a dedicated card for business expenses and another for personal spending. This clean separation makes it infinitely easier to justify your credit card payments income tax filings.

Step 6: Declare All Sources of Income

If you have income from freelancing, capital gains, rental income, or any other source declare it. An undeclared ₹2 lakh freelancing income might be exactly the gap that turns your credit card spending into “unexplained expenditure.”

Step 7: Consult a CA Before the Notice Arrives

Proactive consultation is always less expensive than reactive damage control. At Adwani and Company (https://www.adwaniandco.com/), we conduct pre-filing reviews specifically designed to identify potential red flags in your financial profile including credit card spending patterns.The best way to avoid a credit card income tax notice is to maintain proper documentation of every third-party card usage.

What to Do If You Have Already Received a Credit Card Payments Income Tax Notice

If a notice under Section 142(1), 148, or any assessment-related provision has already arrived due to your credit card spending, here is your action plan:

- Do not panic, but do not ignore it. Every notice has a response deadline. Missing it escalates the situation.

- Gather all supporting documents bank statements, credit card statements, UPI transaction records, reimbursement proofs, and employer certificates.

- Prepare a detailed reconciliation showing the source of every major payment.

- Engage a qualified Chartered Accountant who has experience handling income tax scrutiny cases. The response needs to be precise, professional, and legally sound.

Dr. Haresh Adwani and his team at Adwani and Company have successfully represented hundreds of clients in assessment proceedings. “A well-drafted response, backed by solid documentation, resolves most cases at the first stage itself,” he notes.

The Bigger Picture: India’s Expanding Financial Surveillance

The government’s ability to track financial transactions has grown exponentially in recent years. Between SFT reporting, AIS, the Faceless Assessment Scheme, Project Insight, and data analytics, the Income Tax Department now has a 360-degree view of your financial life.

Credit card payments are just one piece of the puzzle. The department cross-references your:

- Bank deposits and withdrawals

- Property registrations

- Mutual fund and equity transactions

- Foreign remittances

- GST filings (for businesses)

Conclusion: Do Not Let Your Credit Card Become a Tax Liability

Your credit card is a financial tool convenient, rewarding, and essential in today’s digital economy. But every payment you make creates a data point in the tax department’s vast surveillance network. The days of flying under the radar are long gone.

A credit card payments income tax notice is not a criminal accusation it is a request for explanation. But an unprepared response can snowball into penalties, interest, and prolonged assessments.Remember, a credit card income tax notice is not a criminal charge but an unprepared response can lead to serious financial consequences.

The solution is simple: track, document, and reconcile. And when in doubt, seek professional guidance.

If you want expert guidance on credit card tax compliance, income tax notices, or financial planning, connect with Adwani and Company today (https://www.adwaniandco.com/). With decades of experience and a team led by seasoned professionals including CA Dipesh Gurubakshani and Dr. Haresh Adwani, we ensure your finances are always compliant, transparent, and optimized.

Reach out to us today because the best time to prepare is before the notice arrives.

Now let us answer the most commonly searched questions about credit card income tax notice on Google.

1. Can I receive a credit card payments income tax notice?

Yes, absolutely. If your total credit card payments exceed ₹10 lakh in a financial year and are reported under SFT (Rule 114E), the Income Tax Department can issue a notice if there is a mismatch with your declared income.

2. What is the SFT limit for credit card payments?

Banks must report credit card payments exceeding ₹10 lakh in aggregate during a financial year. Additionally, cash payments exceeding ₹1 lakh against credit card bills are also reported.

3. What happens under Section 69C if I cannot explain my credit card spending?

Under Section 69C, unexplained expenditure can be treated as your income and taxed at 60% plus surcharge and cess under Section 115BBE. This can result in significant tax liability, interest, and penalties.

4. Does using a credit card for someone else’s purchase create tax problems?

It can, if you do not maintain proper documentation. Since the card is in your name, the payment is attributed to you. Always keep proof of reimbursement through bank transfers.

5. How can I check if my credit card payments are reported in AIS?

Log in to the Income Tax e-Filing Portal (https://www.incometax.gov.in), navigate to the AIS section, and review the SFT data. Your credit card payment details will be listed there.

6. Is it necessary to declare credit card payments in my ITR?

While you do not declare credit card payments directly in your ITR, your income declaration must be consistent with your overall spending. If total payments exceed your income, you should be prepared to explain the source.

7. How can Adwani and Company help me with a credit card income tax notice?

At Adwani and Company (https://www.adwaniandco.com/), we specialize in income tax compliance, notice responses, and tax planning. Our team can help you reconcile your credit card payments, prepare documentation, and respond effectively to any notice

Author

CA.Dipesh Gurubakshani. He is a Chartered Accountant with professional experience in audit, direct taxation, and accounting advisory services.